the Creative Commons Attribution 4.0 License.

the Creative Commons Attribution 4.0 License.

| 05 May 2026

| 05 May 2026

Assessment of multiple predictors to the psychological effects of flooding for residential and business areas in Peninsular Malaysia

Shabir Ahmad Kabirzad

Edmund C. Penning-Rowsell

Zed Zulkafli

Badronnisa Yusuf

Bakti Hasan-Basri

Mohd E. Toriman

Floods are among the most disastrous environmental hazards, causing devastating tangible and intangible impacts. The psychological impact, which can be classified as intangible damage, is a crucial part of well-being assessment. The psychological impact of flooding has begun to receive attention in recent years; however, the complexity of measuring it makes it less attractive to be considered in damage empirical assessment and risk studies. The present study seeks to evaluate willingness to pay for the psychological impact of flooding experienced by households and business premises, and the different factors that could be determining variables of the psychological impact. A total of 217 respondents has participated in the empirical face-to-face survey conducted in different vulnerable places in Peninsular Malaysia. Through the willingness to pay (WTP) method, only 107 and 34 respondents from residential and business premises, respectively, expressed their agreement to spend on flood management efforts. The study found that flood durations and family sizes are statistically significant contributors to psychological impact for households, reflecting the intangible damages to the residential sector. The results suggest a greater investment to support affected people's welfare by improving communities' resilience and consolidated management during flood events from different authorities. These will enhance flood risk reduction efforts and reduce the psychological impacts on people at risk of flooding. The findings also revealed a key challenge of inferring intangible flood damages for business sectors through empirical evidence.

- Article

(1005 KB) - Full-text XML

- BibTeX

- EndNote

Flooding remains one of the greatest threats, with its unprecedented impact on society. A comparison of flood events across different return periods reveals that the impact of flooding on both residential properties and business premises can be extremely severe (Merz et al., 2010). A post-flood survey by the Department of Statistics Malaysia (DOSM) (2021) in 2021 shows that flood damages on residential buildings amount to USD 395 million, while business premises amount to as high as USD 123 million. Numerous studies have attempted to quantify tangible flood damages on residential and business properties (Kreibich et al., 2010; Wijayanti et al., 2017; Van Ootegem et al., 2015; Kabirzad et al., 2024), given their importance to the community's well-being and economy. Studies that attempted to establish connections between flood damages and predictors from the socio-economic and building characteristics have often applied the regression approaches given the intricate relationship between the variables (Kabirzad et al., 2024), with the aim of unravelling numerical evidence that supports analytical flood risk management, given their importance to the community's well-being and economy.

Over the past decade, analysis of flood consequences has evolved beyond conventional tangible economic damages to intangible impacts, such as psychological effects, as a critical subset of adverse flood consequences (Stanke et al., 2012; Yoda et al., 2017; Hudson et al., 2017; Patwary et al., 2024; Guntu et al., 2026). Psychological effects can be defined as the emotional and mental responses individuals experience due to disruptions in daily life, such as anxiety, depression, and stress, exacerbated by isolation and changes in routine (Veale, 1987). The psychological impact of flooding stemmed from people's experience during or after the devastating event, which may involve losing possessions, physical health, livelihoods, or even worse, the lives of loved ones (Law et al., 2025). During the disastrous flooding in 2014 and 2021 in Malaysia, severe psychological effects on individuals and the community have been reported (Ridzuan et al., 2022).

Current scholarly consensus has emphasized that the psychological effects of flooding is important to be integrated in flood management decision-making (Ti et al., 2016; Nawi et al., 2021; Sulong and Romali, 2022). Some studies have even found that intangible flood damages could be more severe than tangible losses (Nga et al., 2018; Han et al., 2023; Joseph et al., 2015). However, there are limited studies that have investigated the multivariable effect of socio-economic, building, and flood physical dimensions on psychological damages. Among the variables considered, income level and spatial characteristics (e.g., proximity to rivers, flood depth, and duration) have been reported to influence the degree of psychological effects of flooding (e.g., Fatemi et al., 2020; Lekuthai and Vongvisessomjai, 2001). By addressing the psychological impacts of flooding quantitatively, more targeted interventions can be established. The interventions can enhance emotional support systems during periods of high disaster risk and bolster community resilience, for instance, with the establishment of a more robust social network and organized shelter systems to reduce anxiety and stress during post-flooding recovery (Zahari and Hashim, 2018; Akhir et al., 2021).

One of the approaches used in the valuation of non-marketable intangible flood impacts is the willingness-to-pay (WTP) through the contingent valuation method (CVM). Since the late 20th century, studies have acknowledged CVM as one viable approach to measure non-market value. The approach takes the monetary amount for a particular good or service to alleviate flood damage that people suggest to alleviate flooding as a way to indicate the degree of “losses” of the psychological effects (e.g., Foudi and Osés-Eraso, 2022; Rodríguez Castro et al., 2025). However, its application to non-market valuation in flood damage assessment, particularly for informing decision-making agencies in damage management, is infrequently used and remains relatively new (Rogers et al., 2019). There are two mechanisms for the information of WTP to be acquired: through the stated or revealed preference approach. The first one is elicited by directly asking the respondent on the amount, whilst the second is by observing the behaviour (Foudi and Osés-Eraso, 2022; Tomoi et al., 2024; Vegh et al., 2024). WTP can also be elicited by adding a portion of expenses to bills to cover the WTP to improve the quality of life, and shows that the socio-economic factors could contribute to determining the WTP, particularly the income and education, to reduce respondents' health risk (Jianjun et al., 2016).

The present study aims to assess intangible flood damage represented by the psychological effects of flooding experienced by households and businesses in Peninsular Malaysia. Current studies in Malaysia on the two elements at risk in the context of psychological losses, alongside other flood damage factors, are absent. The ability to understand their influence on flood damages through an empirical lens and to be able to identify key drivers would provide evidence to support the refinement of flood damage modelling and flood management options. The present study elicited the monetary value of psychological impact from respondents through empirical surveys at affected locations to better understand and address future flood impacts. Based on respondents' flooding experiences and their recollection of its effects on their well-being, the study attempts to incorporate the subjective experiences of people exposed to flooding in the risk-based flood investment decision-making.

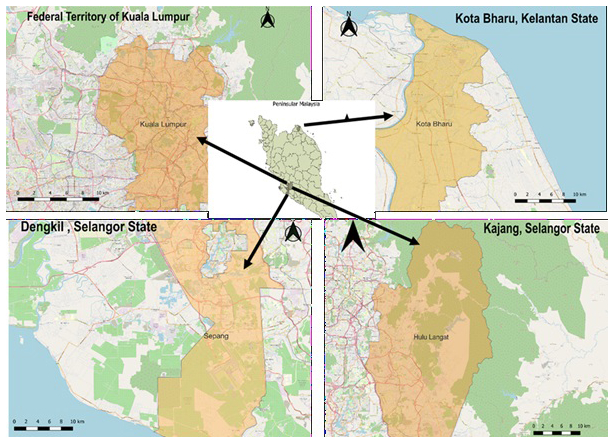

This section outlines the study areas for the evaluation of intangible flood damage through in-person interviews. The target individuals are from residential and business premises with prior flood experience and are still living in the flood-prone areas. The study areas were first identified through a desk study and a review of secondary information, focusing on two regions in Peninsular Malaysia that are often flooded: one in the northeast and another in the southwest. Within the two distinct regions, territories, and states, that are more suitable and practical for ground surveys and in-person interviews were identified, which led to Kuala Lumpur Federal Territory, Selangor state, and Kelantan state being selected for further review. Further demarcations of areas were assisted by rigorous reviews of authorized documents and reports related to floods at the territory and state levels, such as those published by the Department of Irrigation and Drainage Malaysia (2012), Kuala Lumpur City Hall (2015), and the National Statistics Department. Grey literature and open-source websites were also consulted to verify and confirm the suitability of areas. Finally, exact villages or towns affected by fluvial floods for face-to-face interviews were identified.

A description of damage generation processes for the study has led to specifying only fluvial flooding for the samples. Other flood damage generation cases, such as due to extensive extreme storms in urban areas, i.e., pluvial flood, are avoided. Moreover, flooded areas being surveyed were those that are located adjacent to rivers within a radius of 1.3 km, such that the distance from the river can be incorporated as part of the possible decisive factors to psychological intangible damage. In-person interviews were conducted between July and September 2020. Within the selected locations, each respondent was approached individually at their residential or business premises. To ensure relatively recent experiences with flood damage, only individuals who had experienced at least one flood event in the past 10 years preceding 2020 were included. Descriptions of intangible losses were provided in length to respondents during the interview before the other specific questions.

Figure 1The map was created using OpenStreetMap and the Malaysian district and territory boundaries file. Areas where surveys were conducted in Peninsular Malaysia, and the yellow area is the district or territory boundaries. Top left: Kuala Lumpur Federal Territory; top right: Kota Bharu district, Kelantan; bottom left: Dengkil, Sepang district; bottom right: Kajang, Hulu Langat.

Figure 1 illustrates the study area, specifically where the interviews and ground surveys were conducted: Kota Bharu city in Kelantan, Kuala Lumpur Federal Territory, and Dengkil and Kajang districts in Selangor. Frequent flooding and large-scale evacuations have been reported in these locations. For instance, in the Kuala Lumpur Federal Territory area, as many as 2000 residents were evacuated in the 2013 flood event (Khairi et al., 2013). These reports are consistent with information obtained from interviews conducted in 2020 with the Kuala Lumpur City Hall (DBKL) officers. Kajang and Dengkil in Selangor have experienced multiple flood events, some of which resulted in large-scale evacuations. Both Kajang and Dengkil are situated within the Langat River basin. Flood reports indicate that approximately 200 people were evacuated in Kajang, and nearly 500 residents were relocated to public shelters from various inundated areas in Dengkil during the 2020 flood event. In the city of Kota Bharu, a devastating flood in 2014 led to the evacuation of 20 000 residents (Abdullah, 2014).

This section explains the data and methods applied for the analysis. Variables considered for the establishment of the decisive factors of intangible damage are explained in Sect. 3.1. Section 3.2 continues to describe the method of WTP, continued by Sect. 3.3 on data pre-processing, and lastly Sect. 3.4 on regression and model specification.

3.1 Variables for intangible flood damage analysis

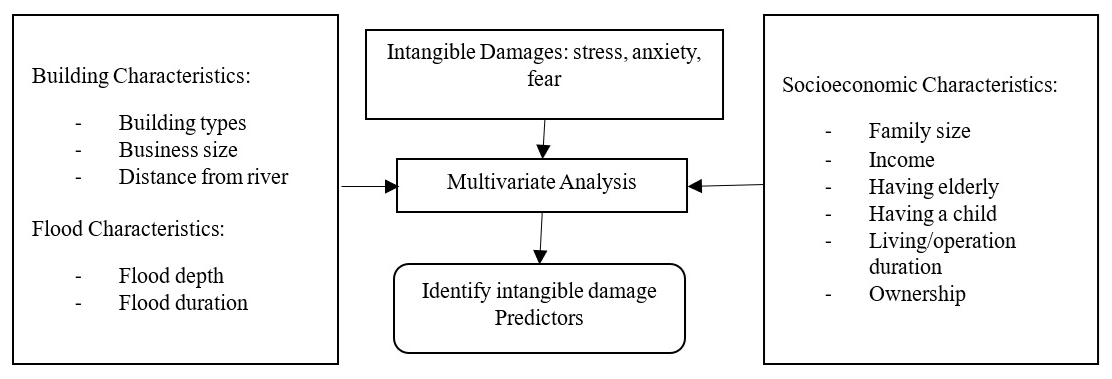

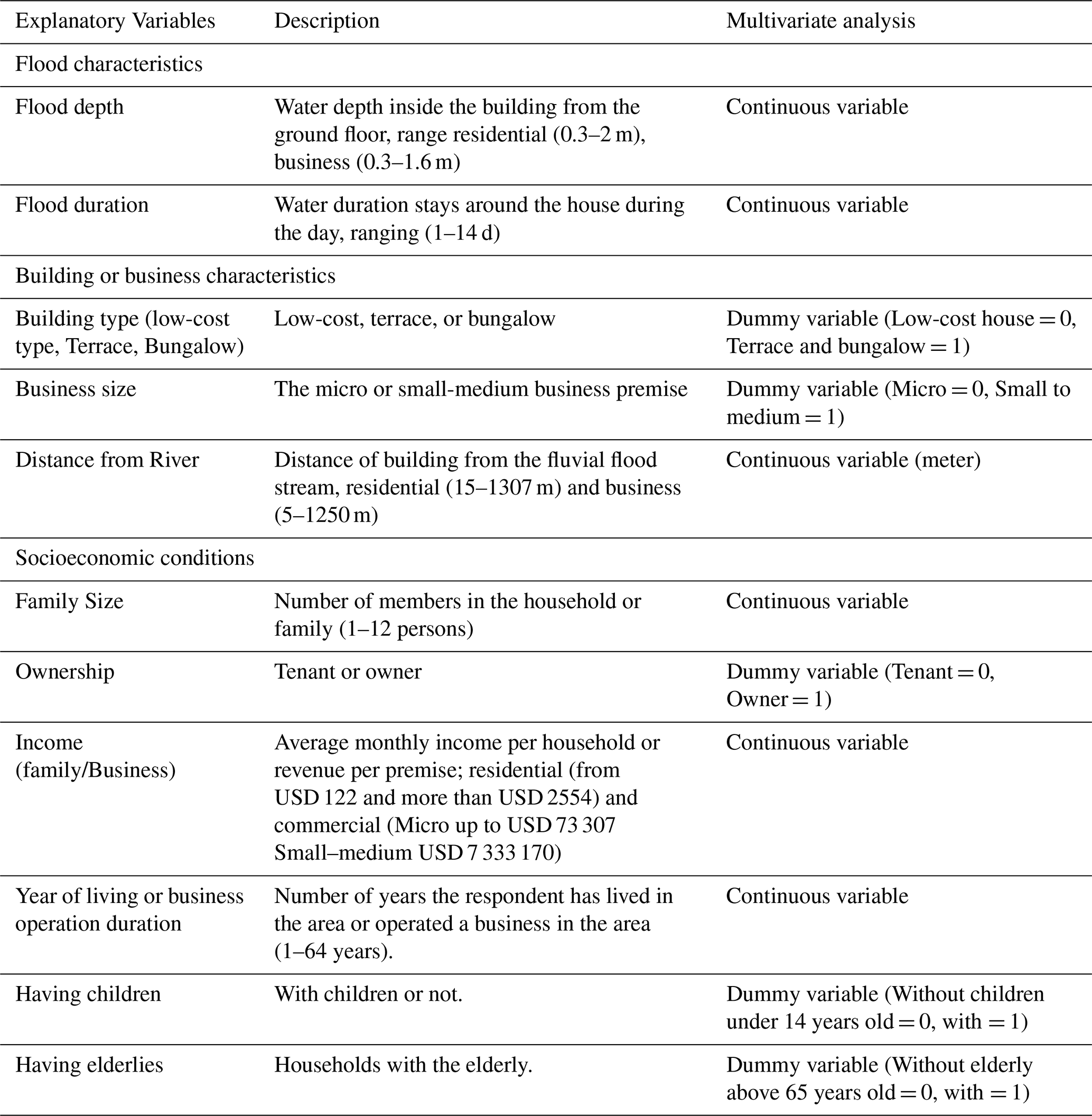

A range of variables, identified based on expert knowledge and literature review, are considered important for estimating intangible flood damage. The variables are grouped by flood characteristics, building factors, and socio-economic characteristics. Figure 2 shows the eleven independent variables: flood depth, flood duration, building type, proximity to water bodies, business type, household size, years of living (residential) or years of operation duration (business), ownership, income, the presence of elderly individuals, and the presence of children. Despite the number of possible exogenous variables that could have influenced the psychological effects of flooding, this study focuses on eleven subset variables to take advantage of the contact time with respondents and the quality of responses. All of the explanatory variables were used to assess their correlation with the intangible damage. Whilst some of the respondents shared their recovery experiences of post-flooding during the interview, the recovery rates were not being considered explicitly as one of the variables in the multivariate analysis.

Figure 2The intangible damage assessment and the independent variables used in the multivariate analysis for the damage model.

The survey questionnaire was designed to allow for separate analysis of residential and business. Residential buildings were classified as village-type, terraced, or bungalow, while businesses were categorized as micro, small-to-medium, or large businesses, similar to that proposed in KTA Tanaga Sdn Bhd (2003). These classifications represent the primary building structure types prevalent in Malaysia. The categorization of business premises type was based on the total number of workers, as specified by SME Corporation Malaysia (2022). Businesses were categorized into micro and small businesses based on the number of full-time permanent employees. Micro businesses were defined as having fewer than five employees, while small to medium businesses included those with five to thirty employees (SME Corporation Malaysia, 2022).

As for the socio-economic characteristics, three classifications were used for the demarcation of the residential sector income levels following the national standard and the parent study (i.e., Kabirzad et al., 2024) (Department of Statistics Malaysia, 2020). The classification is B40 (bottom 40 %), M40 (middle 40 %), and T20 (top 20 %). The B40 group included those earning less than USD 1130 per month, the M40 group covered incomes between USD 1130 and 2553.45 per month, and the T20 group consisted of households earning more than USD 2553.45 per month. For business, micro business income is between USD 73 367–3 668 380, and small-medium income is USD 3 668 380–7 333 170 (SME Corporation Malaysia, 2022).

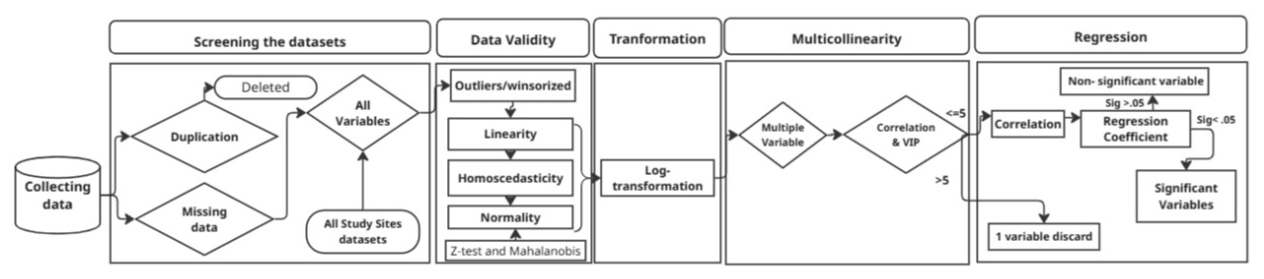

Figure 3The data process and analysis flowchart (Some of the data validity process: Winsorizing, Empirical rule, Z-test, Normality, and Mahalanobis distance).

The intangible suffering due to the psychological effects of flooding was valued using the WTP approach. The monetary values that the respondents are willing to pay to alleviate flood damages were taken as a proxy, where the absolute value of WTP originally in Malaysian Ringgit (MYR) was converted to US Dollars (USD). The study aimed to assess damage using multiple variables and understand the multiple variables' contributions. Figure 3 shows the process in which the survey was made in person and where the data screening for missing values and duplication is applied. Further explanation of the process is discussed in the next sub-sections. Ultimately, a multivariate regression analysis was undertaken to identify the contributing factors of intangible damage to residential buildings and business premises.

3.2 Intangible losses by the contingent valuation method

Intangible damages of flooding for households primarily involved diminished well-being, stress, anxiety, and sleep disturbances linked to the difficulty in managing possessions and recovering. For businesses, intangible flood damages might stem from concerns about employees' well-being and subsequent disruptions on operations and recovery (Lekuthai and Vongvisessomjai, 2001). To quantify the non-market values for alleviating psychological health resulting from flooding, the present study adopts similar work by Foudi and Osés-Eraso (2022) to estimate the WTP of people who have flood experiences and could experience flooding again,.

During the engagement sessions, conversations with household heads, business managers, or owners in flood-exposed areas were conducted in Malay, as many residents felt more comfortable speaking in their native language. The conversations were informal at first, but shifted to a more formal tone once participants were willing to engage further. The engagement was conducted cautiously to ensure interviewees received sufficient information about the study's purpose before delving deeper into the WTP questions. A sequential information-sharing process was applied before respondents were gradually brought into the topic and questions regarding WTP. Respondents can be emotionally affected by their past devastating flood experiences (Joseph et al., 2015), and this can be addressed by validating respondents' psychological experiences prior to questions being asked.

After listening to and validating their stories, they were briefed on the effects of stress and anxiety. Additionally, they were informed about the challenges of monetizing intangible flood damage, which requires the adoption of the contingent valuation method (Markantonis et al., 2012; Semrau et al., 2016; Joseph et al., 2015). To avoid confusion between intangible and tangible losses, and to focus WTP responses solely on psychological and mental health effects, the distinction between the two was explained to the interviewees. They were advised not to include financial or asset losses in their WTP values (e.g., Foudi and Osés-Eraso, 2022). Respondents were then presented with a dichotomous choice question on their willingness to pay for flood mitigation that potentially reduces the intangible damages of flooding that they experienced. Respondents who answered “yes” were then asked an open-ended question on how much they are willing to pay. Those who stated “no” were asked for their reasons. Interviews for open-ended questions were only continued for respondents who answered “yes”. From the face-to-face conversations, those who refused to pay were influenced by their strong views about the payment vehicle that should be part of the government's responsibility. Such a protest bid is common in similar social studies, and exclusions of the protest bids are necessary to reduce bias in the analysis.

Meanwhile, a number of questions were adopted to guide responses on WTP values associated with alleviating psychological burden. For instance, some of the interviewees have built concrete barriers at the opening of their house to protect from flood intrusion. Such a real case was used as a surrogate to the WTP value, but with emphasis on alleviating their psychological burden. Example questions are: (1) how much they are willing to allocate to reduce their stress and anxiety if the same flood event were to occur?, (2) if the same event as the worst that they had experience is to happen in the future and they were not at home, will the property-level protection barriers that they have constructed able to ease their psychological burden of not be able to save possessions while they are not there? If yes, then the costs for the barriers were asked, or (3) if the respondents do not yet have property-level barriers, they will be asked if they are willing to spend on one, and by how much to alleviate the same psychological burden as they have experienced during the worst flood experienced before. The price of WTP is adjusted for the inflation rate using the Malaysian Consumer Price Index calculator to maintain consistency and comparability across different periods (Department of Statistics Malaysia, 2021). Furthermore, the results were presented as an absolute value in US dollars (USD) for a flood event. Information on the selected variables for the multivariate analysis, such as building types, income level, etc., of the respondents was then collected. All information was stored using an online standard form, including the coordinates of the building's location where the interview took place.

The collected information of WTP represents the anxiety and stress at their personal level related to the businesses that they are managing, and the stress and anxiety stemming from impacts on productivity and disruption of sales, etc., manifested from the condition of flood events that they are in. Whilst the description is not exhaustive and pathways of intangible damages on individuals and businesses that they own or work in may overlap, the present study does not express a distinction. It is perceived that the intangible damages can be of any disturbance to the running of the businesses that cannot be monetised, whether it stems from a personal level of the business owner/worker related to the businesses, or from more specific losses to the business, such as loss of opportunity that they are stressed and anxious about. Moreover, the WTP does not consider economic losses that can be monetised indirectly, for example, due to business downtime. The exclusion was made clear during the interviews (e.g., Darnkachatarn and Kajitani, 2025).

3.3 Data Pre-processing

The data that has been collected was filtered to identify duplicates and missing information for all variables. The data pre-processing was conducted for both sectors in preparation for the correlation and regression analysis. Missing information was imputed with values having similar characteristics to the ones recorded (e.g., Rodríguez Castro et al., 2025). All datasets of the same type of variable from different areas were combined into a single database. Building type, business size, the presence of elderly or children, and ownership status were treated as binary variables, whilst others were treated as continuous variables. Outliers in all continuous variables were identified and treated using winsorizing, the z-test, or three standard deviation cut-offs, and the Mahalanobis distance method. After completing this process, the normality, linearity, and homoscedasticity were assessed. Subsequently, a multicollinearity assessment between the variables to identify highly correlated independent variables was undertaken. The regression analysis on intangible damage for residential types of buildings indicated multicollinearity between two independent factors, which are flood duration and distance from the river. Therefore, the distance from the river was excluded to improve the accuracy and reliability of the regression, which leaves only nine independent variables.

For the normality test, some datasets were first transformed to accommodate the variables in normality using the log or log-log transformation (Svenningsen et al., 2020). For residential buildings, the datasets were log-log transformed except for independent variables, such as building type, presence of elderly, presence of children, and ownership status. Meanwhile, for commercial buildings, the datasets remained untransformed except for income data, which was log-transformed. Linearity was checked to ensure that the dependent variable is linearly related to each independent variable. Violations can reduce model accuracy, though slight deviations may be acceptable depending on context. In this case, residual plots confirmed a generally linear relationship, but some continuous variables did not meet the assumption. Another assumption is that the residuals exhibit constant variance, ensuring the absence of heteroscedasticity (unequal variance), Heteroscedasticity can bias regression estimates and reduce predictive accuracy. Therefore, statistical transformation, such as logarithmic adjustment or other methods, is applied.

3.4 Regression Analysis and Model Specification

After the pre-processing of datasets was completed, multivariate regressions were performed to explore the relationship between intangible flood impacts in terms of victims' psychological burdens and the considered factors. These models enabled the identification of key factors contributing to damage severity related to the three groups of factors: flood characteristics, building types, and socio-economic conditions (Lee, 2020). The regression analyses for this study considered three significance thresholds, such as 10 %, 5 %, and 1 % (e.g., Lamond et al., 2015). Table 1 presents the detailed descriptions of explanatory variables considered. The goal of the analysis is to identify predictors that statistically influenced the psychological burden of respondents due to flood events. Meanwhile, standardized coefficients β were utilized to determine the relative significance of each predicting variable (x), allowing for comparison of their effects on intangible damages (Y). The final models include error terms that address unexplained variations. These models were expressed as a general Eq. (1), encompassing all essential variables to ensure reproducibility for future research investigating flood impacts in comparable settings (Svenningsen et al., 2020).

The model's performance was evaluated using the coefficient of determination (R2), which indicates the proportion of variance in the damage explained by the independent variables (e.g., Poussin et al., 2015). However, R2 is not always recommended as a sole indicator of model accuracy, as it can be artificially inflated by adding more independent variables (Jarantow et al., 2023). Furthermore, a low R2 does not necessarily indicate a weak relationship, as statistically it is heavily influenced by the variation in the independent variables (Hamilton et al., 2015). Therefore, its interpretation must always be contextualized within the specific research scope (Hair et al., 2018).

Table 1The independent variables were used in the multiple regression assessment.

The results are presented in three stages; first, Sect. 4.1 elaborates on respondents' characteristics and general feedback from the face-to-face interviews. Second, Sect. 4.2 examines variations in intangible damages across key determinant variables. Lastly, Sect. 4.3 presents a multiple regression analysis to identify decisive factors of intangible damage.

4.1 Respondents' characteristics and responses

A total of 380 respondents were approached, of whom 217 provided valid responses. Eliciting monetary valuations for psychological impacts proved challenging, particularly when respondents were asked about their willingness to pay (WTP) to reduce flood-related psychological distress. Despite the use of a sequential and tailored interview approach to build respondents' trust, some participants expressed disagreement when asked about their willingness to make monetary contributions to safeguard themselves from the psychological effects of flooding.

Of the valid respondents, only 141 responses (107 residential and 34 businesses) expressed willingness to pay for disaster risk reduction measures, while 76 respondents (35 %) stated zero WTP or refused to contribute. Common reasons included limited income, the belief that flood mitigation is the government's responsibility, lack of trust, and the perceptions that flood impacts were not severe or were primarily emotional. Such “protest zero” responses are common in contingent valuation studies for flood reduction measures (e.g., Hanley et al., 2009; Brouwer et al., 2009; Jones et al., 2015), and are typically excluded to reduce bias (Foudi and Osés-Eraso, 2022). In this study, zero WTP responses were excluded to focus on identifying the drivers for the non-zero range of WTP. Furthermore, WTP was used as a proxy for the intangible damage, which is unlikely to be zero in the context of damaging flood events.

Most respondents were from residential buildings, reflecting limited commercial activity in the study areas. Local information indicated that several flood-affected businesses had permanently relocated to safer locations. Time constraints and demanding schedules also limited participation among business owners, resulting in excessively long waiting times and limited interviews. Consequently, the dataset is dominated by residential respondents. Given the difficulty of collecting socio-economic and psychological data, data validity relied partly on expert judgment.

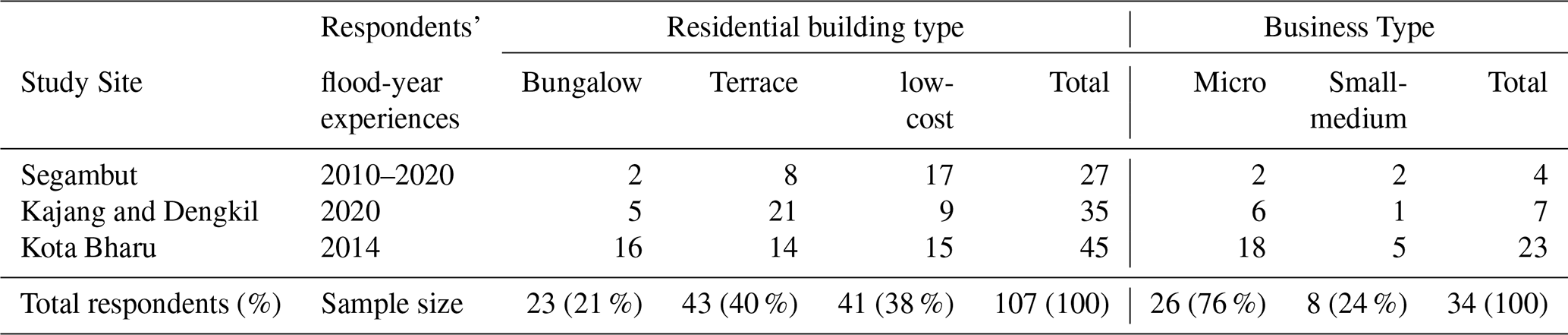

Table 2Summary of the respondents in residential and business premises categories across the study sites.

Table 2 summarises the number of residential and business respondents. Forty-four percent (44 %) of residential respondents and sixty-seven percent (67 %) of business respondents were only from the Kota Bharu (Kelantan) study area, where terrace buildings accounted for nearly 40 % of all buildings, followed by low-cost housing. Respondents from the Segambut district of Kuala Lumpur were few, and primarily resided in terrae and low-cost houses. In Kajang and Dengkil areas of Selangor, most respondents also lived in terrace houses, while Kota Bharu district respondents were more evenly distributed across building types.

Among business respondents, the predominant type of business is micro-sized enterprises (76 %), followed by small to medium businesses. The small-to-medium businesses (SMEs) represented 24 % of the study sample. Kota Bharu recorded the highest flood depths for both residential and business premises, largely attributed to the major flood event in 2014. Although the case study sites experienced flooding in different years, all locations have been severely affected by flooding over the past decade.

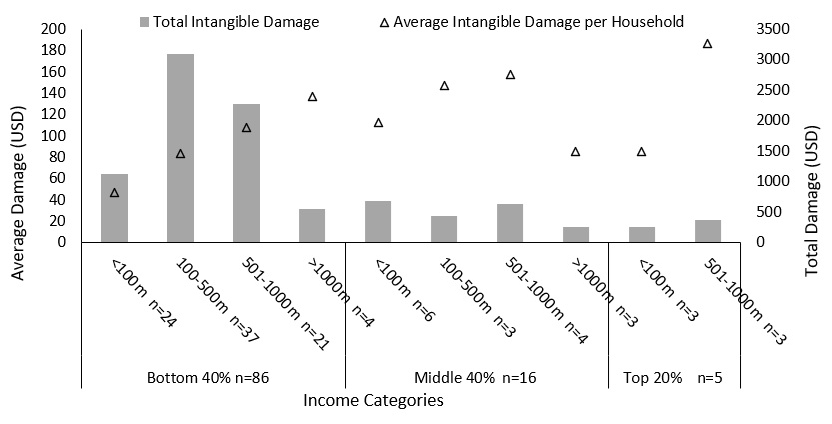

Figure 4A comparison of the total and average values of intangible damages was conducted across income groups, distance from the river categories, and the number of samples (n).

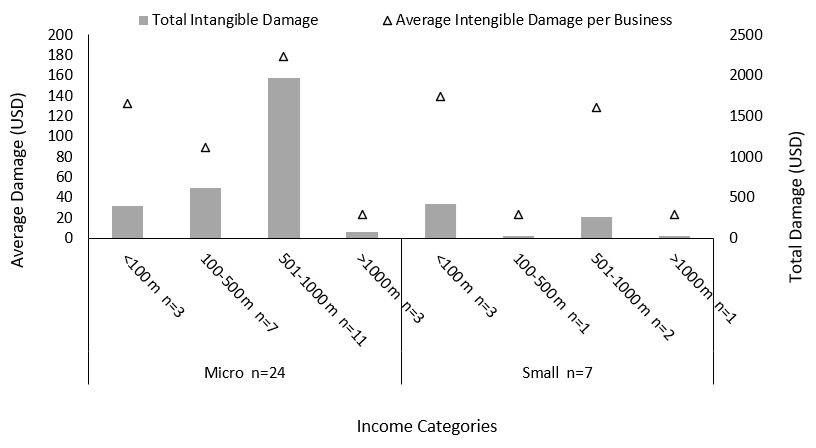

Figure 5Intangible damage assessment of business premises considering income categories, distance from the river, and the number of samples (n).

Variations in intangible damage across residential households and businesses were analysed in terms of income groups, business size, and the distance from the river using both total and average WTP values. Total values refer to the cumulative WTP within each category. Meanwhile, the average values represent the mean WTP. Comparisons across income groups are presented in Figs. 4 and 5.

4.2 Variations in Intangible Damages Across Determinant Variables

Bar charts were used to examine patterns of flood exposure and intangible damage across income groups and business sizes. The analysis focused on whether lower-income households and micro businesses experienced greater exposure and demonstrated higher WTP to reduce psychological impact. Intangible damage was assessed using both total and average WTP across income groups, business size, and buildings' distance from the river. categories.

Figure 4 presents that most residential respondents belonged to the bottom 40 % (B40) income group, followed by the middle 40 % (M40) income group, while the top 20 % (T20) group had the fewest respondents. Given that the interviewed people are randomly approached based on the criteria of their building's proximity to rivers, this distribution highlights the disproportionate exposure of lower-income households to flooding. Only 13 and 5 respondents belonged to the M40 and T20 groups, respectively, compared with 86 respondents from the B40 group. Average WTP value ranged from USD 46.6 to 186.4 across all income groups. While the B40 group recorded the highest total losses due to its larger sample size, median WTP values per household were comparable across all income groups.

Figure 5 presents results for the business premises. Micro businesses were more exposed to flooding than small to medium businesses, reflected in a larger sample size (24 versus 7). Micro businesses also showed a higher total WTP value, largely due to their greater representation. However, the median WTP value was similar across business sizes, consistent with the findings for residential households. This suggests that lower income or smaller business size does not necessarily imply significantly lower WTP.

Residential households reported higher intangible losses than businesses, reflecting their greater perceived need for interventions to reduce psychological and mental effects associated with flooding. However, comparable median WTP values across income and business size categories indicate that income alone cannot be identified as a decisive factor based on single-variable analysis. These findings may change with a larger sample size, highlighting the challenges of collecting data from flood-affected populations. While descriptive analysis provides useful insights, multivariate analysis is required to identify key determinants of intangible flood damage.

4.3 Multiple Regression Analysis of Intangible Damages

This section presents results of multivariate regression for residential and business sectors, examining building characteristics, socio-economic factors, and flood attributes influencing WTP. The objective is to identify the relative strength and significance of intangible damage drivers.

4.3.1 Residential Building Intangible Damage

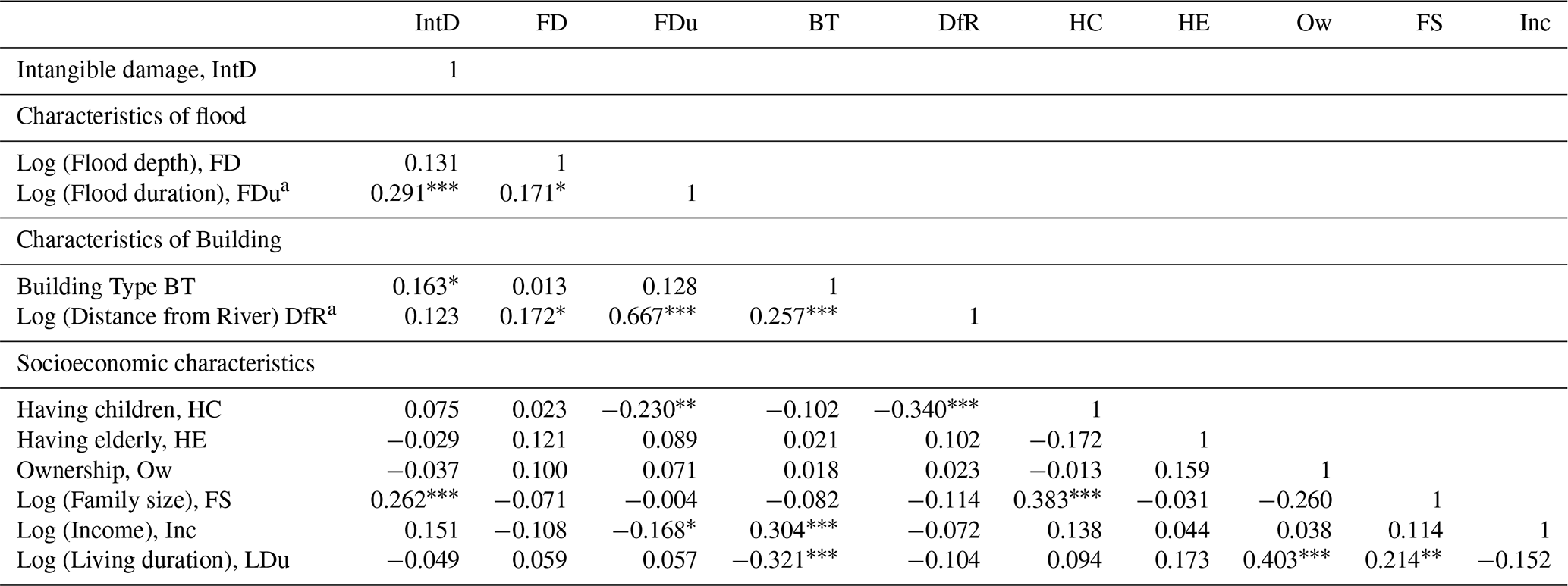

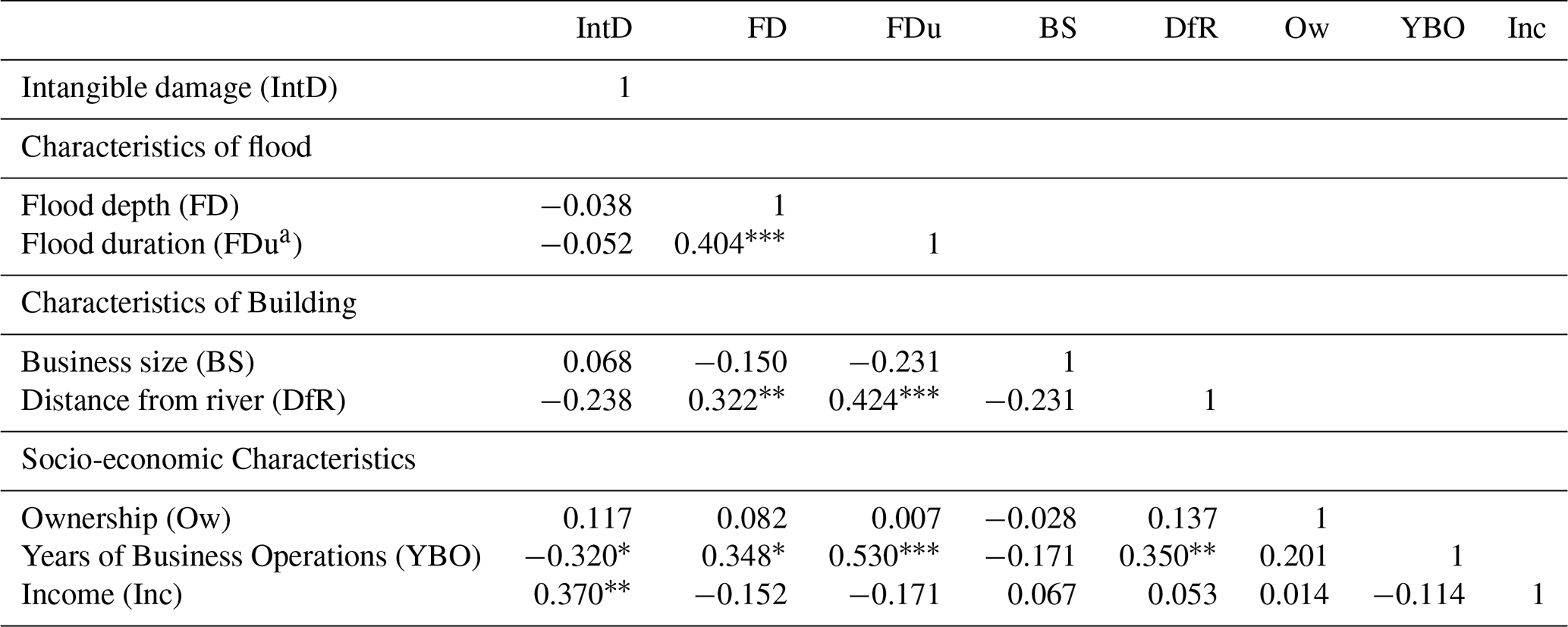

Table 3 presents the correlation matrix between intangible damage and explanatory factors. Most variables show a positive association with intangible damage at varying levels of significance. Flood durations, family sizes, and building types are positively correlated with intangible damage at a significance level at 5 % or 10 %. The relationships are intuitive; longer flood duration increases distress. A similar result was found in a previous study that flood duration has a positive contribution to flood loss (Czajkowski and Cunha, 2020). Similarly, the larger the number of family members, the greater the anxiety level and therefore the positive relationship with WTP. Large families do contribute to greater anxiety during floods, according to Babcicky et al. (2021), where there will be greater responsibilities that they have to bear.

Table 3Correlation matrix of flood intangible damages to households with damage predictors.

Note: ∗ Correlation is significant at the 0.1. Correlation is significant at the 0.05. Correlation is significant at the 0.01.

a Distance from the river and flood duration variables have multicollinearity issues.

Flood depth and proximity to rivers are not found to be statistically significant in explaining the WTP for the reduction of intangible damage. However, previous studies have found that flood depth and residence in proximity to rivers can be statistically significant explanatory variables for intangible flood damage (Lamond et al., 2015; Babcicky et al.,2021). Moreover, previous studies in Peninsular Malaysia have used flood depth as a key indicator to evaluate tangible flood damage (Rehan and Yiwen, 2023; Kabirzad et al., 2024; Fadhil et al., 2025). Another counterintuitive finding from the present study is that families are willing to pay for psychological health, but not defined by their income level. The findings of income level as an insignificant variable to explain the WTP are quite similar to some studies. For example, Ghanbarpour et al. (2014) and Yusmah et al. (2020) show that the middle-income households are more willing to contribute to flood prevention measures, whilst higher-income households are less responsive. Results from the present correlation matrix also indicate that other socio-economic characteristics are not statistically significant in explaining the WTP. This is in contrast with what has been found in Foudi and Osés-Eraso (2022), where older individuals have a lower demand for protection despite being financially vulnerable.

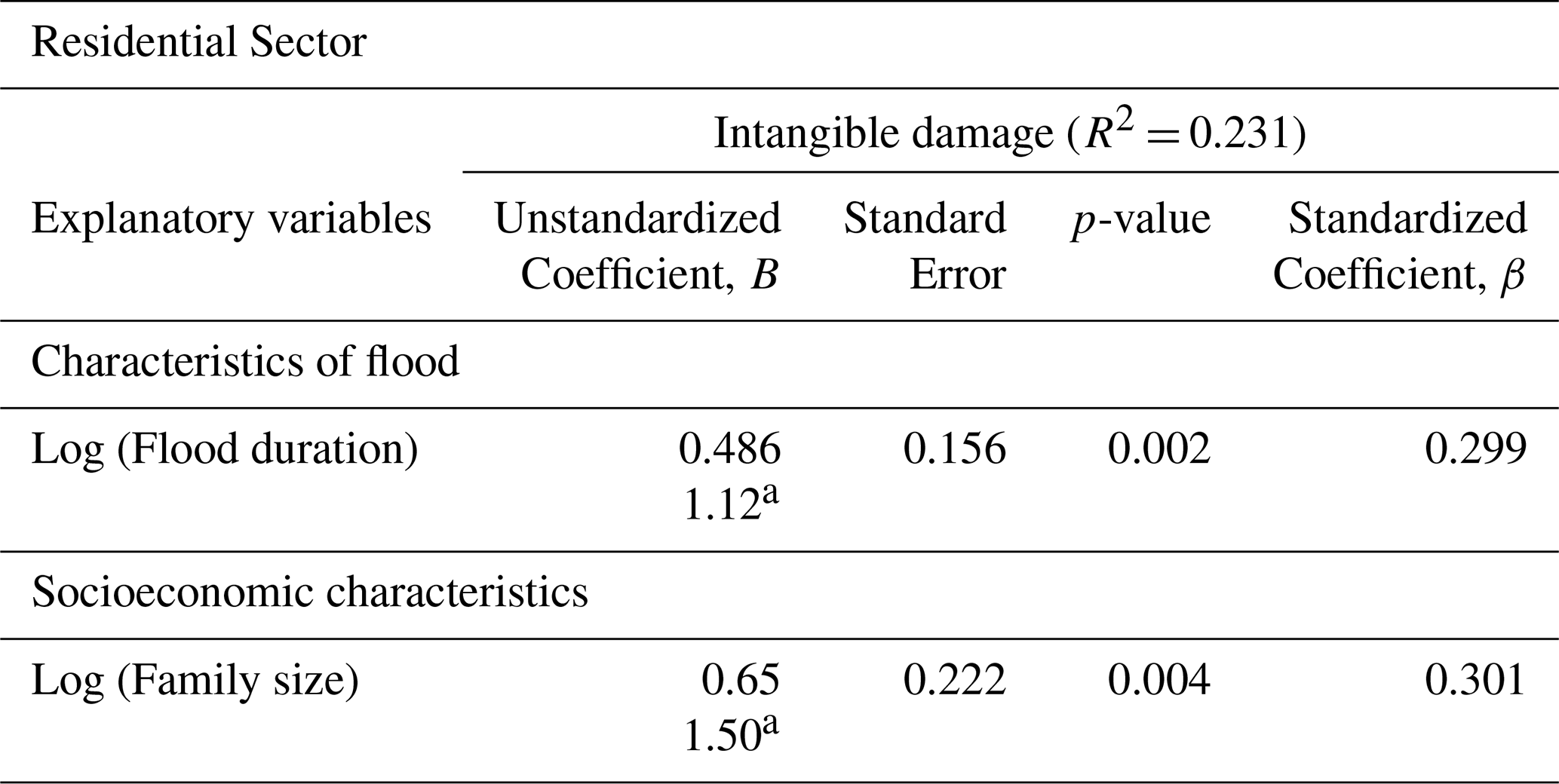

Table 4Intangible damage multiple regression results for the residential sector.

∗ The value represents the percentage increase resulting from a 1 % rise.

Table 4 presents the multivariate linear regression results after addressing multicollinearity and statistically significant considerations. Among the components examined, only two variables, flood duration and family size, are significant explanatory variables for intangible damage at 1 % significance level. The results indicate that a 1 % increase in flood duration leads to a 1.12 % increase in WTP, while a 1 % increase in family size is associated with a proportional rise of 1.5 % in intangible damage. For example, adding an individual to a household can lead to a relative increase in intangible damage of approximately 12.5 %. In other multiple regression studies, flood duration has been identified as statistically significant to intangible damage of residences (e.g., Czajkowski and Cunha, 2020). But family size is not (Joseph et al., 2015).

The regression model for intangible damage yielded a coefficient of determination (R2) of 0.23, indicating that the dependent variable (i.e., the intangible damage) is explained by other variables at 23 % of its variance. Although the value of R2 is modest, it is considered acceptable in studies of intangible flood impact (Hair et al., 2018) because R2 values in such contexts are often constrained by limited variability in explanatory variables (Hamilton et al., 2015). In some research fields, an R2 of 0.10 or lower is acceptable, as it is entirely context-dependent on the research scope (Hair et al., 2018).

4.3.2 Business Premises Intangible Damages

Table 5 presents a correlation matrix of business premises, where seven variables are considered, and the other variables, such as family size, having children, and/or elderly members, were not included as they are considered only for the residential building regression analysis. The results show that variables are correlated to intangible damage at varying significance levels. Income is positively correlated, while years of business operation are negatively correlated with the intangible damage. It is argued that experienced businesses may better cope with shocks and therefore suffer much less compared to those with less experience (Abdullah et al., 2019). Meanwhile, analysis of a multiple regression model for business premises shows that the considered variables do not adequately explain intangible damage in the business sector, with a p-value above 0.1, suggesting a failure to reject the null hypothesis. Previous studies supported that these variables are not a significant to intangible damage in business premises (Czajkowski and Cunha, 2020).

Table 5Correlation matrix of flood intangible damages to business with damage predictors.

Note: ∗ Significant at the 0.1 level. Significant at the 0.05 level. Significantly at the 0.01 level.

a Variable was removed due to multicollinearity between the independent variables.

The regression analysis for business premises did not yield statistically significant results, indicating that the proposed model could not reliably predict intangible damage in the business sector. A review of the literature reveals limited empirical evidence on intangible flood damage models for business, reflecting the complexity of capturing non-market losses in the context. Data collection proved particularly challenging, as few business owners were willing to disclose information on psychological or emotional impacts. The small sample size may introduce bias and reduce the accuracy of the damage model in the business sector. On the other hand, comparing intangible damage assessments between households and businesses is difficult, as each context presents distinct forms of evidence for evaluating impact. Intangible damages for businesses primarily relate to employee well-being, operational disruptions, asset management, revenue losses, and recovery challenges.

4.4 Effects of Sample Size

Despite the insights obtained, the analysis suggests that the current sample size may be insufficient to fully model intangible impacts across both sectors. A primary limitation is the lack of statistically significant associations in the business sector, which is largely attributable to small sample sizes. In the residential sector, while flood duration and family size were significant predictors, the distribution of the sample may result in bias and the statistical insignificance of the other variables. Specifically, smaller sample sizes for the middle income (M40) and high income (T20) than the B40 income group may limit the accuracy of the residential findings related to income level. Therefore, increased sample sizes from diverse flood-prone regions are necessary to improve model prediction and account for the heterogeneous nature of these sectors. Nonetheless, this requires laborious efforts and resources to target both the quality and quantity of sample sizes.

This study assesses the psychological health impact of flooding – conceptualised as intangible damage – on residences and businesses. By applying a non-market willingness-to-pay approach, the present study estimates the monetary value of stress, distress, and worry associated with flood events through face-to-face surveys at selected flood-prone locations. The aim is to highlight a critical need to strengthen social resilience by identifying key variables. The analysis hypothetically suggested that building characteristics, socio-economic conditions, and flood characteristics are vital contributions to intangible damage. The findings show that for the residential sector, family size contributes to shaping psychological impacts, as larger households tend to receive greater intangible losses. Moreover, flood duration emerged as a key contributor to intangible damage, suggesting the need for well-planned and effective response mechanisms in residential communities. In addition, the waiting time of victims in flooded areas and in evacuation centres should be reduced with an effective response and consolidated management from different authorities. In the business sector, while all variables considered did not yield statistically significant results, larger companies appear better able to cope with flood-related psychological impacts, suggesting that experience and adaptive capacity can reduce intangible damages.

To reduce psychological vulnerability and strengthen social resilience, policy measures such as improved early warning systems, enhanced public awareness, and better land-use planning are essential. Timely evacuation planning and targeted protection of the vulnerable are necessary to mitigate the impacts of flood duration. These findings emphasize the value of integrating social characteristics into flood resilience planning through active community engagement and the development of context-specific awareness guidelines. Strengthening resilience also requires improved flood forecasting and the integration of social characteristics into planning at multiple spatial scales.

As one of the few studies attempting to quantify intangible flood damages for both residential and business sectors, this research contributes preliminary evidence to an emerging field. However, several avenues for future research remain to advance the understanding of flood risk management. Future work could incorporate a broader range of indicators alongside physical and economic variables in multivariate analyses that would better explain variations in intangible damage. Future studies could also detail specific determinants in the business sector, such as job titles, service types, and the nature of business models, to further discern the classification and magnitude of intangible losses. However, getting participation from people through face-to-face interviews could be challenging. This emphasizes the need for coordinated efforts in managing flood damage-related data for effective proactive interventions and strategic policy decisions.

The raw data supporting the findings of this study are subject to ethical restrictions. The dataset remains the property of the university and was collected under specific approval from the Institutional Ethical Committee, which stipulates that the data be used exclusively for research purposes. Consequently, the primary source data cannot be made publicly available in order to protect participant confidentiality and adhere to institutional data governance policies.

SAK: Writing (original draft preparation, review, editing), Conceptualization, Data Curation, Formal Analysis, Investigation and Methodology, Software, Validation, Visualization. BMR: Writing (review and editing), Conceptualization, Supervision, Methodology, Funding Acquisitions, Validation, Visualization. ECP: Conceptualization, Review, Methodology, Validation. ZZ: Conceptualization, Supervision, Methodology, Validation. BY: Conceptualization, Supervision, and Methodology. BH: Conceptualization, Supervision, and Methodology. MET: Project administration, Conceptualization, and Validation.

The contact author has declared that none of the authors has any competing interests.

Publisher's note: Copernicus Publications remains neutral with regard to jurisdictional claims made in the text, published maps, institutional affiliations, or any other geographical representation in this paper. The authors bear the ultimate responsibility for providing appropriate place names. Views expressed in the text are those of the authors and do not necessarily reflect the views of the publisher.

This study received financial backing from the Ministry of Higher Education Malaysia through the grant NEWTON/1/2018/WAB05/UPM/2.

We extend our appreciation to Victoria Bell, Helen Houghton-Carr, James Miller, Paul Sayers, Rhian Chapman, Lisa Stewart, Alexandra Kaelin, and Ponnambalam Rameshwaran of the Flood Impact Across Scales Project UK team for their valuable contributions. Additionally, we acknowledge the support provided by the Drainage and Irrigation Department Malaysia, and the Kuala Lumpur City Council officers. We would also like to thanks Universiti Putra Malaysia's ethical committee for their approval to the research proposal prior to the data collection.

Prior to the site visit for the interview, Universiti Putra Malaysia's ethical committee approved the research proposal to conduct the information.

This research has been supported by the Ministry of Higher Education, Malaysia (grant no. NEWTON/1/2018/WAB05/UPM/2).

This paper was edited by Animesh Gain and reviewed by three anonymous referees.

Abdullah, F., Mohammad, S. N., Mohamad, J., and Ahmad, M.: The Economic Model for Flood Damage Cost in Retailing Business in Malaysia, in: Proceedings of the Second International Conference on the Future of ASEAN (ICoFA) 2017, Vol. 1, https://doi.org/10.1007/978-981-10-8730-1_51, 2019.

Abdullah, I.: Kelantan Flood, Straits Times, https://www.nst.com.my/news/2015/09/kelantan-flood-more-20000-evacuated (last access: 20 November 2024), 2014.

Akhir, N. M., Aun, N. S. M., Selamat, M. N., and Amin, A. S.: Exploring Factors Influencing Resilience Among Flood Victims in Malaysia, International Journal of Academic Research in Business and Social Sciences, 11, 969–981, https://doi.org/10.6007/IJARBSS/v11-i6/10227, 2021.

Babcicky, P., Seebauer, S., and Thaler, T.: Make it personal: Introducing intangible outcomes and psychological sources to flood vulnerability and policy, Int. J. Disast. Risk Re., 58, 102169, https://doi.org/10.1016/j.ijdrr.2021.102169, 2021.

Brouwer, R., Akter, S., Brander, L., and Haque, E.: Economic valuation of flood risk exposure and reduction in a severely flood-prone developing country, Environ. Dev. Econ., 14, 397–417, https://doi.org/10.1017/S1355770X08004828, 2009.

Czajkowski, J. and Cunha, L. K.: Willingness to pay for flood insurance: a case study in Phang Khon, Sakon Nakhon Province, Thailand, The 6th International Conference, IOP Conference Series: Earth and Environmental Science, https://doi.org/10.1088/1755-1315/612/1/012041, 2020.

Darnkachatarn, S. and Kajitani, Y.: Flood damage assessment model of industrial sectors in a Megacity: Derivation from business survey data in the Bangkok Metropolitan Region, Int. J. Disast. Risk Re., 118, 105221, https://doi.org/10.1016/j.ijdrr.2025.105221, 2025.

Department of Irrigation and Drainage Malaysia: Updating condition of flooding and flood damage assessment in Malaysia, Final report, Vol. 1, Executive summary, Kuala Lumpur, Malaysia, 2012.

Department of Statistics Malaysia: Household Income & Basic Amenities Survey Report 2019, Press Release, in: Chief Statistician Malaysia, 2020.

Department of Statistics Malaysia: Malaysia CPI Inflation Calculator, Department of Statistics Malaysia, https://www.dosm.gov.my/cpi_calc/ (19 January 2021), 2021.

Fadhil, M. G., Rehan, B., Kabirzad, S., Badronnisa, Y., Zulkaflia, Z., Bakti, H.-B., and Torimand, M. E.: Evaluating the Performance of Depth-Damage Curves in Flood Damage and Risk Analysis: A Case Study from Malaysia, Jurnal Kejuruteraan, 37, 2159–2172, 2025.

Fatemi, M. N., Okyere, S. A., Diko, S. K., Kita, M., Shimoda, M., and Matsubara, S.: Physical vulnerability and local responses to flood damage in peri-urban areas of Dhaka, Bangladesh, Sustainability, 12, 1–23, https://doi.org/10.3390/SU12103957, 2020.

Foudi, S. and Osés-Eraso, N.: Information, Experience, and Willingness to Mitigate Mental Health Consequences From Flooding Through Collective Defence, Water Resour. Res., 58, https://doi.org/10.1029/2021WR031357, 2022.

Ghanbarpour, M. R., Saravi, M. M., and Salimi, S.: Floodplain Inundation Analysis Combined with Contingent Valuation: Implications for Sustainable Flood Risk Management, Water Resour. Manag., 28, 2491–2505, https://doi.org/10.1007/s11269-014-0622-2,2014.

Guntu, R., Mohor, G. S., Thieken, A. H., Müller, M., and Kreibich, H.: Deciphering the drivers of direct and indirect damages to companies from an unprecedented flood event: A data-driven, multivariate probabilistic approach, Nat. Hazards Earth Syst. Sci., 26, 163–186, https://doi.org/10.5194/nhess-26-163-2026, 2026.

Hair, J. F., Black, W. C., Babin, B. J., Anderson, R. E., Black, W. C., and Anderson, R. E.: Multivariate Data Analysis, 8th edn., Annabel Ainscow, ISBN 978-1-4737-5654-0, https://doi.org/10.1002/9781119409137.ch4, 2018.

Hamilton, D. F., Ghert, M., and Simpson, A. H. R. W.: Interpreting regression models in clinical outcome studies, Bone Joint Res., 4, 152–153, https://doi.org/10.1302/2046-3758.49.2000571, 2015.

Han, D., Huang, G., Liu, L., Zhai, M., Fu, Y., Gao, S., Li, J., and Pan, X.: Factorial CGE-Based Analysis for the Indirect Benefits of the Three Gorges Project, Water Resour. Res., 59, 1–19, https://doi.org/10.1029/2022WR033360, 2023.

Hanley, N., Colombo, S., Kriström, B., and Watson, F.: Accounting for negative, zero and positive willingness to pay for landscape change in a national park, J. Agr. Econ., 60, 1–16, https://doi.org/10.1111/j.1477-9552.2008.00180.x, 2009.

Hudson, P., Botzen, W. J. W., Poussin, J., and Aerts, J. C. J. H.: Impacts of Flooding and Flood Preparedness on Subjective Well-Being: A Monetisation of the Tangible and Intangible Impacts, J. Happiness Stud., 20, 665–682, https://doi.org/10.1007/s10902-017-9916-4, 2017.

Jarantow, S. W., Pisors, E. D., and Chiu, M. L.: Introduction to the Use of Linear and Nonlinear Regression Analysis in Quantitative Biological Assays, Current Protocols, 3, 1–56, https://doi.org/10.1002/cpz1.801,2023.

Jianjun, J., Wenyu, W., Ying, F., and Xiaomin, W.:Measuring the willingness to pay for drinking water quality improvements: Results of a contingent valuation survey in Songzi, China, J. Water Health, 14, 504–512, https://doi.org/10.2166/wh.2016.247, 2016.

Jones, N., Clark, J. R. A., and Malesios, C.: Social capital and willingness-to-pay for coastal defences in south-east England, Ecol. Econ., 119, 74–82, https://doi.org/10.1016/j.ecolecon.2015.07.023, 2015.

Joseph, R., Proverbs, D., and Lamond, J.: Assessing the value of intangible benefits of property level flood risk adaptation (PLFRA) measures, Nat. Hazards, 79, 1275–1297, https://doi.org/10.1007/s11069-015-1905-5, 2015.

Kabirzad, S. A., Rehan, B. M., Zulkafli, Z., Yusuf, B., Hasan-Basri, B., and Toriman, M. E.: Examining direct and indirect flood damages in residential and business sectors through an empirical lens, Water Sci. Technol., 90, 142–155, https://doi.org/10.2166/wst.2024.202, 2024.

Khairi, R., Noriza, R., and Ariffin, R.: Community-Based Disaster Management in Kuala Lumpur, in: Procedia – Social and Behavioral Sciences, Elsevier B. V., 85, 493–501, https://doi.org/10.1016/j.sbspro.2013.08.378, 2013.

Kreibich, H., Seifert, I., Merz, B., and Thieken, A. H.: Development of FLEMOcs – a new model for the estimation of flood losses in the commercial sector, Hydrolog. Sci. J., 55, 1302–1314, https://doi.org/10.1080/02626667.2010.529815, 2010.

KTA Tanaga Sdn Bhd: Flood Damage Assessment of 26 April 2001 Flooding Affecting The Klang Valley And The Generalised Procedures And Guide Lines For Assessment Of Flood Damages Final: Guidelines and Procedures for the Assessment of Flood Damages in Malaysia, Vol. 2, Issue Oct., Kuala Lumpur, Malaysia, 2003.

Kuala Lumpur City Hall: Master Plan, Vol. III, Kuala Lumpur, Malaysia, 2015.

Lamond, J. E., Joseph, R. D., and Proverbs, D. G.: An exploration of factors affecting the long term psychological impact and deterioration of mental health in flooded households, Environ. Res., 140, 325–334, https://doi.org/10.1016/j.envres.2015.04.008, 2015.

Law, S., Marinova, T., Ewins, L., and Marks, E.: Understanding the psychological impact of flooding on older adults: A scoping review, Ann. NY Acad. Sci., 99–115, https://doi.org/10.1111/nyas.15356, 2025.

Lee, D. K.: Data transformation: A focus on the interpretation, Korean Journal of Anesthesiology, 73, 503–508, https://doi.org/10.4097/kja.20137, 2020.

Lekuthai, A. and Vongvisessomjai, S.: Intangible flood damage quantification, Water Resour. Manag., 15, 343–362, https://doi.org/10.1023/A:1014489329348, 2001.

Markantonis, V., Meyer, V., and Schwarze, R.: Review Article “Valuating the intangible effects of natural hazards – review and analysis of the costing methods”, Nat. Hazards Earth Syst. Sci., 12, 1633–1640, https://doi.org/10.5194/nhess-12-1633-2012, 2012.

Merz, B., Kreibich, H., Schwarze, R., and Thieken, A.: Review article “Assessment of economic flood damage”, Nat. Hazards Earth Syst. Sci., 10, 1697–1724, https://doi.org/10.5194/nhess-10-1697-2010, 2010.

Nawi, A. M., Wan Puteh, S. E., Hod, R., Idris, B. I., Ahmad, I. S., and Ghazali, M. Q.: Post-Flood Impact on the Quality of Life of Victims in East Coast Malaysia, International Journal of Public Health Research, 11, 1278–1284, https://doi.org/10.17576/ijphr.1101.2021.01, 2021.

Nga, P. H., Takara, K., and Cam Van, N.: Integrated approach to analyze the total flood risk for agriculture: The significance of intangible damages – A case study in Central Vietnam, Int. J. Disast. Risk Re., 31, 862–872, https://doi.org/10.1016/j.ijdrr.2018.08.001, 2018.

Patwary, M. M., Bardhan, M., Haque, M. A., Moniruzzaman, S., Gustavsson, J., Khan, M. M. H., Koivisto, J., Salwa, M., Mashreky, S. R., Rahman, A. K. M. F., Tasnim, A., Islam, M. R., Alam, M. A., Hasan, M., Harun, M. A. Y. Al, Nyberg, L., and Islam, M. A.:Impact of extreme weather events on mental health in South and Southeast Asia: A two decades of systematic review of observational studies, Environ. Res., 250, 118436, https://doi.org/10.1016/j.envres.2024.118436, 2024.

Poussin, J. K., Wouter, Botzen, W. J., and Aerts, J. C. J. H.: Effectiveness of flood damage mitigation measures: Empirical evidence from French flood disasters, Glob. Environ. Change, 31, 74–84, https://doi.org/10.1016/j.gloenvcha.2014.12.007, 2015.

Rehan, M. B. and Yiwen, M.: Discrepancies in estimated flood losses on paddy production: Application of damage models on historical flood records of the Northwest States of Peninsular Malaysia Discrepancies in estimated flood losses on paddy production: Application of damage model, IOP Conference Series: Earth and Environmental Science, https://doi.org/10.1088/1755-1315/1205/1/012020, 2023.

Ridzuan, M. R., Razali, J. R., Abd Rahman, N. A. S., and Ju, S. Y.: Youth Engagement in Flood Disaster Management in Malaysia, International Journal of Academic Research in Business and Social Sciences, 12, 846–857, https://doi.org/10.6007/ijarbss/v12-i5/13250, 2022.

Rodríguez Castro, D., Rafiezadeh Shahi, K., Sairam, N., Fischer, M., Samprogna Mohor, G., Thieken, A., Dewals, B., and Kreibich, H.: Key Drivers of Flash Flood Damage to Private Households, J. Flood Risk Manage., 18, 1–22, https://doi.org/10.1111/jfr3.70088, 2025.

Rogers, A. A., Dempster, F. L., Hawkins, J. I., Johnston, R. J., Boxall, P. C., Rolfe, J., Kragt, M. E., Burton, M. P., and Pannell, D. J.: Valuing non-market economic impacts from natural hazards, in: Natural Hazards, Springer Netherlands, 99, https://doi.org/10.1007/s11069-019-03761-7, 2019.

Semrau, M., Lempp, H., Keynejad, R., Evans-Lacko, S., Mugisha, J., Raja, S., Lamichhane, J., Alem, A., Thornicroft, G., and Hanlon, C.: Service user and caregiver involvement in mental health system strengthening in low- and middle-income countries: Systematic review, BMC Health Serv. Res., 16, https://doi.org/10.1186/s12913-016-1323-8, 2016.

SME Corporation Malaysia: SME Definitions, Malaysia Government, http://smecorp.gov.my/index.php/en/policies/2020-02-11-08-01-24/sme-definition (last access: 23 August 2024), 2022.

Stanke, C., Murray, V., Amlôt, R., Nurse, J., and Williams, R.: The effects of flooding on mental health: Outcomes and recommendations from a review of the literature, PLoS Currents, https://doi.org/10.1371/4f9f1fa9c3cae, 2012.

Sulong, S. and Romali, N. S.: Flood Damage Assessment: a Review of Multivariate Flood Damage Models, International Journal of GEOMATE, 22, 106–113, https://doi.org/10.21660/2022.93.gxi439, 2022.

Svenningsen, L. S., Bay, L., Doemgaard, M. L., Halsnaes, K., Kaspersen, P. S., and Larsen, M. D.: Beyond the stage-damage function: Estimating the economic damage on residential buildings from storm surges, Nat. Hazards Earth Syst. Sci. Discuss. [preprint], https://doi.org/10.5194/nhess-2020-30, 2020.

Ti, T. Z., Azaini, T. M., Shahruniza, A. S., Jamil, J., Si, Y. J., Jiun, M. T. L., Rengganathan, N. K. N., Ismail, S. B., Kadir, A. A., Razak, A. A., and Hassan, M. H. M.: Psychiatric Morbidities Among Post Flood Elderly Victims in Kelantan, Malaysia, Asean Journal of Psychiatry, 17, 209–216, 2016.

Tomoi, H., MacLeod, C., Moriyasu, T., Simiyu, S., Ross, I., Cumming, O., and Braun, L.: Determinants of Willingness to Pay for Fecal Sludge Management Services and Knowledge Gaps: A Scoping Review, Environ. Sci. Technol., 58, 1908–1920, https://doi.org/10.1021/acs.est.3c06628, 2024.

Van Ootegem, L., Verhofstadt, E., Van Herck, K., and Creten, T.: Multivariate pluvial flood damage models, Environ. Impact Assess., 54, 91–100, https://doi.org/10.1016/j.eiar.2015.05.005, 2015.

Veale, D. M. W. D. C.: Exercise and mental health, in: Acta Psychiatrica Scandinavica, 76, 113–120)-, https://doi.org/10.1111/j.1600-0447.1987.tb02872.x,1987.

Vegh, T., BenDor, T. K., and Cubbage, F. W.: Testing factors that enhance private participation in payments for ecosystem service programs targeting flood mitigation, Nature-Based Solutions, 7, 100228, https://doi.org/10.1016/j.nbsj.2025.100228, 2025.

Wijayanti, P., Zhu, X., and Hellegers, P.: Estimation of river flood damages in Jakarta, Indonesia, Nat. Hazards, 86, 1059–1079, https://doi.org/10.1007/s11069-016-2730-1, 2017.

Yoda, T., Yokoyama, K., Suzuki, H., and Hirao, T.: Relationship between Long-term Flooding and Serious Mental Illness after the 2011 Flood in Thailand, Disaster Med. Public, 11, 300–304, https://doi.org/10.1017/dmp.2016.148, 2017.

Yusmah, M. Y. S., Bracken, L. J., Sahdan, Z., Norhaslina, H., Melasutra, M. D., Ghaffarianhoseini, A., Sumiliana, S., and Farisha, A. S. S.: Understanding urban flood vulnerability and resilience: a case study of Kuantan, Pahang, Malaysia, Nat. Hazards, 101, 551–571, https://doi.org/10.1007/s11069-020-03885-1, 2020.

Zahari, N. Z. and Hashim, A. M.: Adequacy of Flood Relief Shelters: A Case Study in Perak, Malaysia, E3S Web Conf., 34, 1–8, https://doi.org/10.1051/e3sconf/20183402016, 2018.