the Creative Commons Attribution 4.0 License.

the Creative Commons Attribution 4.0 License.

| 10 Sep 2025

| 10 Sep 2025

Individual flood risk adaptation in Germany: exploring the role of different types of flooding

Lisa Dillenardt

Annegret H. Thieken

The influence of different flood types, i.e., fluvial, flash, and urban pluvial floods, on whether and how flood-affected people prepare for flooding is unclear but might be relevant for effective risk communication. Survey data from more than 3000 households affected by different types of flooding in Germany have been investigated and revealed the influence of flood type on adaptive behavior. Descriptive statistics, Kruskal–Wallis tests, and single-factor analysis of variance (ANOVA) have been used to identify differences and similarities between respondents. Linear regressions have been used to identify factors that influence households' adaptive behavior in the context of fluvial, pluvial, and flash flooding.

Most respondents were motivated to protect themselves, but there were flood-type-specific differences in the factors influencing an adaptive response. Those affected by fluvial events had most often implemented measures before the last flooding and had experienced flooding before but frequently showed signs of maladaptive thinking. Those affected by flash flooding showed less confidence in the effectiveness of measures but were less likely to rate their costs as too high and were most likely to implement measures after the event. Regardless of the type of flooding, the perception of the effectiveness of adaptive measures and a positive perception of personal responsibility were found to be crucial for motivating those affected to protect themselves. These two key elements can be strengthened by offering financial support for adaptive measures. Communication on a municipality level enhances residents' sense of personal responsibility. Hence, communication and management strategies need to involve municipalities and should be tailored to the locally relevant flood type.

- Article

(1887 KB) - Full-text XML

- BibTeX

- EndNote

Floods were Europe's most damaging climate-related extremes between 1980 and 2022 (EEA, 2024). The European Floods Directive (2007/60/EC) was launched in 2007 in response to several damaging flood events in the European Union (EU) around the year 2000 to improve flood risk management and reduce flood impacts (EC, 2007). The directive introduced a structured and integrated flood risk management plan for all EU member states from 2010 onwards, mainly addressing coastal and fluvial floods. In particular, floods that occur due to an overloaded sewage system can be disregarded by member states when adhering to the plan. Germany used this option when adapting the Federal Water Act (Wasserhaushaltsgesetz – WHG) in 2009 to the requirements of the Floods Directive (WHG, 2009). Section 72 of the Federal Water Act defines flooding as “the temporary inundation of land not normally covered by water, particularly by surface waters or seawater entering coastal areas. This does not include flooding from sewage systems”. However, in recent years, many German cities have experienced urban pluvial flooding, e.g., the city of Münster in 2014 (Spekkers et al., 2017) and Potsdam and Berlin in both 2017 and 2019 (Caldas-Alvarez et al., 2022; Dillenardt et al., 2022). Moreover, fast-onset flash floods in the middle hills in May/June 2016 (Laudan et al., 2017; Piper et al., 2016) and July 2021 (Kreienkamp et al., 2021) had huge impacts, i.e., 11 fatalities and EUR 2.6 billion in damage in 2016 and 189 fatalities and EUR 33 billion in damage in 2021 (Thieken et al., 2023). Such impacts from these flood types were unprecedented in the recent past and again called into question current flood risk management approaches.

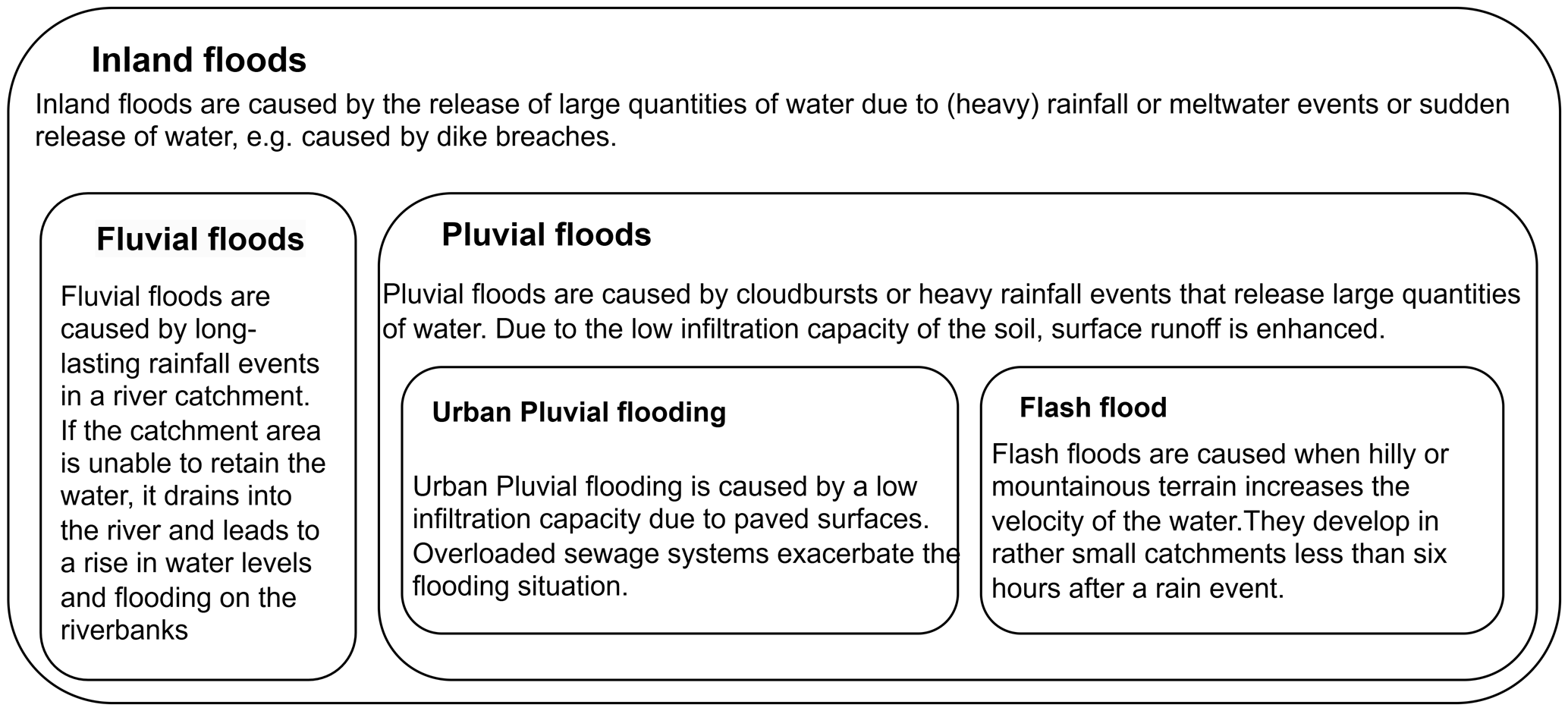

Figure 1Definitions of the flood types used in this paper based on Adams et al. (2020), Bruijn et al. (2009), Hunt (2005), Knocke and Kolivras (2007), and Sweeney (1992).

Integrated flood risk management is built on various risk-reducing measures involving all possible stakeholders, including the general public. Residents in flood-prone areas have been obliged to contribute to flood risk reduction since 2005, as stated in the WHG. Households can implement property-level flood risk adaptation measures (PLFRAMs) (Attems et al., 2020). These measures cover a broad spectrum of effectiveness and implementation costs and thus range from creating emergency plans or sealing foundations to implementing stationary barriers or relocation to a less at-risk area. PLFRAMs can reduce damage caused by floods in situ in a cost-effective manner (DEFRA, 2008; Hudson et al., 2014; Kreibich et al., 2011; Lamond et al., 2018; Poussin et al., 2015). Using the events of 2013 and 2016 as examples, however, Thieken et al. (2022) illustrated that people have to cope with very different flood pathways in terms of hydraulic characteristics. In addition, different coping and adaptive behaviors have been observed (Thieken et al., 2022). Still, explanations and conclusions for risk communication are vague. There has not yet been a study focusing on adaptive behavior and its drivers in the context of different types of flooding to identify and analyze factors influencing the motivation to adapt. Given the devastating event of July 2021, there is an urgent need to understand peoples' behavior better in different (inland) flood settings. To tackle this issue, the adaptive behavior of households in the context of three types of flooding has been investigated: fluvial, flash, and urban pluvial floods (see Fig. 1). It should be noted that the distinction between flood types is not always clearly defined, and there may be overlaps (Hunt, 2005; Kaiser, 2021; Thieken et al., 2022).

All three types of flooding are inland floods (see Fig. 1). Inland floods are usually caused by heavy-precipitation or melting events or the sudden release of water due to, e.g., dike or dam breaches (Bruijn et al., 2009; Hunt, 2005). Overflowing river courses cause fluvial floods. This can be distinguished from pluvial events, which are more directly driven by surface runoff and can, therefore, theoretically occur anywhere (Bruijn et al., 2009). Pluvial floods are triggered by heavy-rainfall events or cloudbursts, which are usually limited in time and space and difficult to predict (DWD, 2016). If pluvial events occur in urban areas with low topography, they are intensified by a high proportion of sealed surfaces and are accompanied by an overload of the sewer and/or drainage system. This study refers to this type of event as urban pluvial flooding. If pluvial events occur in hilly or mountainous terrain, i.e., in steep topography, flash floods with high flow velocities may occur (Arrow et al., 1995; Bruijn et al., 2009). They develop in relatively small catchment areas – usually less than 6 h after a rain event (Arrow et al., 1995; Knocke and Kolivras, 2007).

The theoretical frameworks provided by the protection motivation theory (PMT) and the protection action decision model (PADM) are used to investigate households' adaptive behavior in a structured way. These models identify threat, coping, and responsibility appraisals as drivers of adaptive behavior (Lindell and Perry, 2012; Rogers, 1975, 1983). Various studies have demonstrated the influence of these aspects on the adaptive behavior of households in the context of flooding (Bubeck et al., 2013; Bubeck et al., 2018; Dillenardt et al., 2022; Grothmann and Reusswig, 2006). The PMT and PADM assume that an individual must first recognize a threat by assessing its severity (perceived severity) and probability of occurrence (perceived probability). In addition to the threat, the individual will assess the options for coping by estimating the costs and effort required to implement suitable measures (perceived response costs), their effectiveness in terms of risk reduction (perceived response efficacy), and their ability to implement these measures (perceived self-efficacy). The PADM adds to the basic construct of the PMT in that individuals assess the extent to which they (perceived self-responsibility) or public institutions (perceived government responsibility) are responsible for the implementation of measures and widens the understanding of framing/contextual factors (Lindell and Perry, 2012).

It is assumed that if the appraisals of threat, coping, and responsibility are sufficiently high, a motivation to protect oneself (protection motivation) is encouraged, ideally leading to a protective response within the scope of the person's possibilities. Grothmann and Reusswig (2006) also assume that an assessment of threat that is too low or too high and an assessment of coping strategies that is too low promote maladaptive thinking or emotional coping mechanisms such as fatalism, denial, procrastination, or wishful thinking, each of which is said to have a negative effect on the motivation to protect oneself. Using a hybrid PMT–PADM framework, Dillenardt et al. (2022) found that in the context of urban pluvial flooding, in addition to negative coping mechanisms, negative responsibility appraisal promotes maladaptive thinking. Another aspect of adaptive behavior is trust in public institutions. Terpstra (2011) found that although trust in public institutions is important for (potentially) affected people to believe the complex hazard assessments of scientists and other stakeholders, trust in public flood protection can also reduce their protection motivation. Currently, this aspect is not well accounted for in the theoretical frameworks. Next to threat and coping appraisals, local flood risk management and previously experienced flooding also affect adaptive behavior (Kreibich et al., 2005; Poussin et al., 2014; Thieken et al., 2006; Wind et al., 1999).

Examining the interactions described above between the individual flood types and the factors influencing adaptive behavior leads to a better understanding of flood management strategies. It opens up the possibility of tailoring risk communication to the prevailing flood situation in potentially affected areas. While past research has analyzed factors that influence adaptive behavior solely in the context of one specific type of flooding (Bubeck et al., 2020; Dillenardt et al., 2022; Grothmann and Reusswig, 2006), there is a lack of research about how those influencing factors differ among flood types. In order to close this research gap, this study analyses survey data from over 3000 households affected by fluvial, flash, or urban pluvial flooding in Germany and asks the following question: how does the type of flooding influence adaptive behavior? To answer this question, three further research questions are explored:

-

What adaptive responses were reported by individuals impacted by the three types of flooding?

-

What factors influenced adaptive behavior in those affected by the three flood types?

-

What characteristics of these three groups of respondents explain the differences reported?

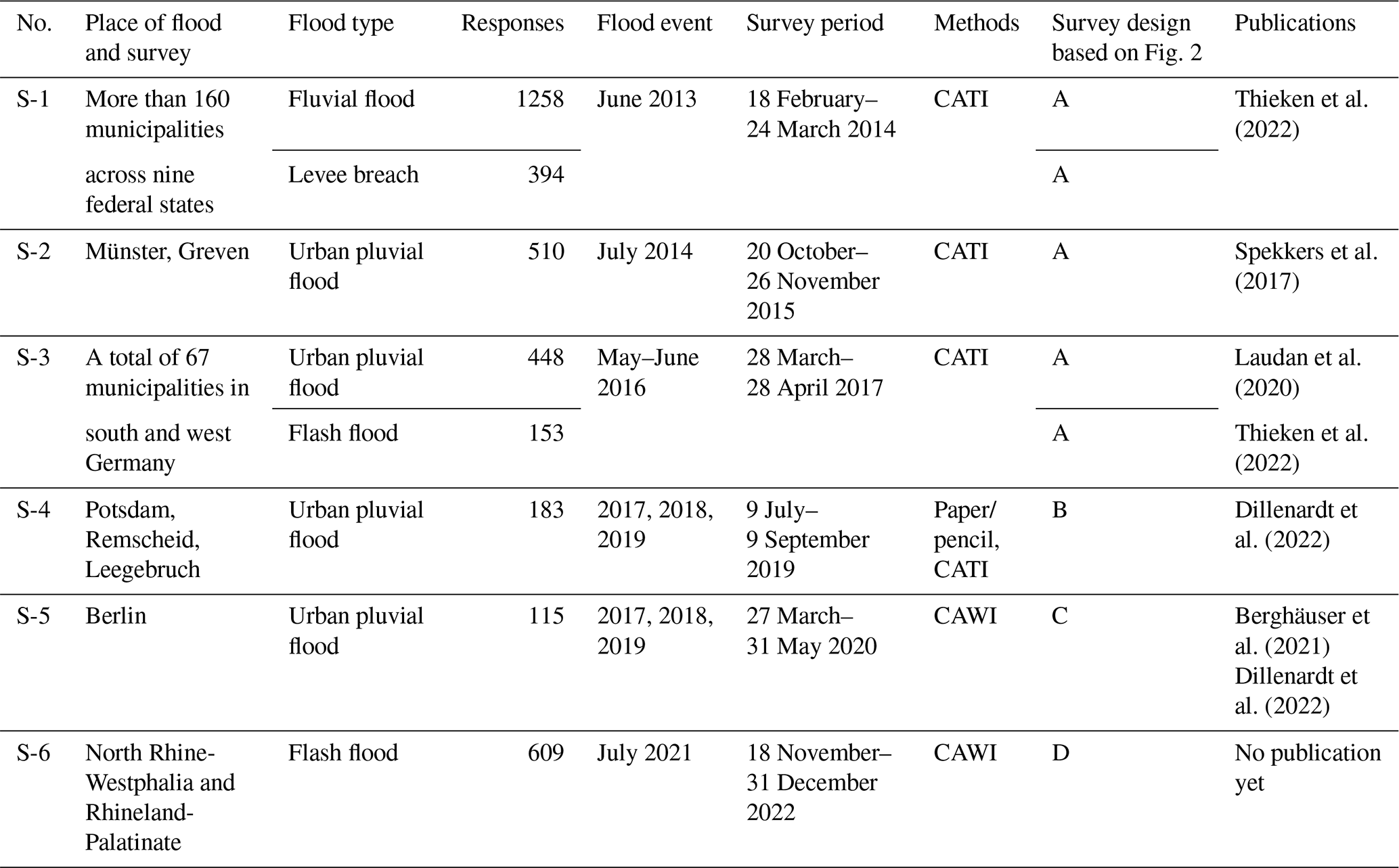

This study is based on survey data collected via four different survey designs (see Fig. 2) between 2014 and 2022 during six surveys among flood-affected households in Germany; see Table 1. While S-1, S-2, S-3, and S-4 were created by random sampling in affected areas (based on lists of flooded roads; see Thieken et al., 2017) and considered only landlines, S-6 was created in Rhineland-Palatinate with the help of the Ahrweiler district, where every third household who had applied for immediate disaster aid was invited to participate. In North Rhine-Westphalia (as well as in S-5), people from the affected areas were invited for a computer-assisted web interview (CAWI) via advertisements on Meta (Facebook and Instagram) and other media. Advertising via Meta to recruit survey participants is a method that has been used in health-related research in the last few decades (Gilligan et al., 2014; Kapp et al., 2013; Shaver et al., 2019) and has also been used by Thieken et al. (2023). A total of 3670 households were questioned about the impacts of recently experienced flood events and adaptive behavior based on the PMT and PADM. Data were collected by paper/pencil, computer-assisted web interviews (CAWIs), and/or computer-assisted telephone interviews (CATIs; see Fig. 2 and Table 1).

Figure 2Simplified illustration of survey designs A–D used to contact flood-affected households in Germany.

Table 1Information on the surveys and demographic information among surveyed households. CAWIs: computer-assisted web interviews, CATIs: computer-aided telephone interviews.

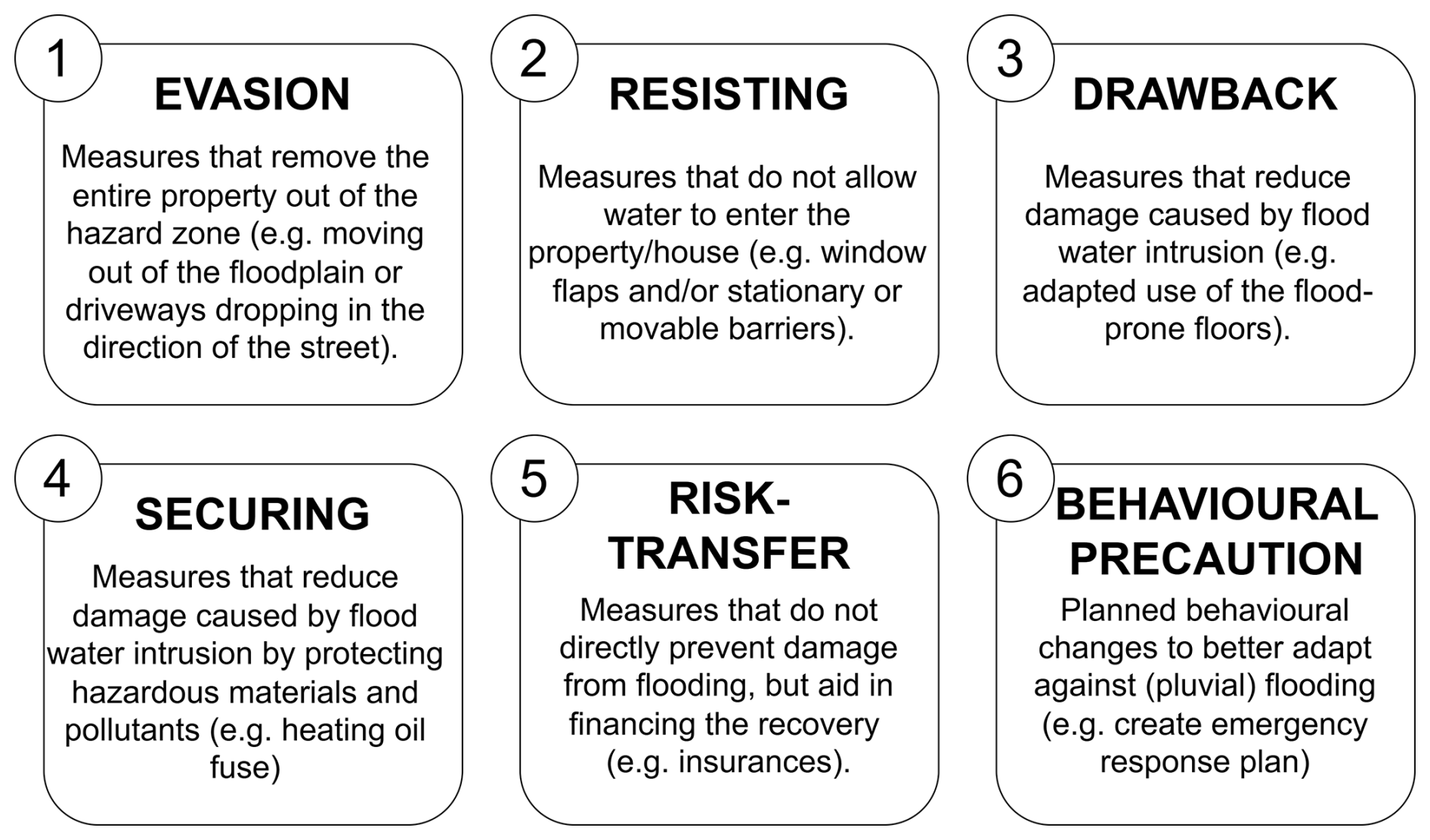

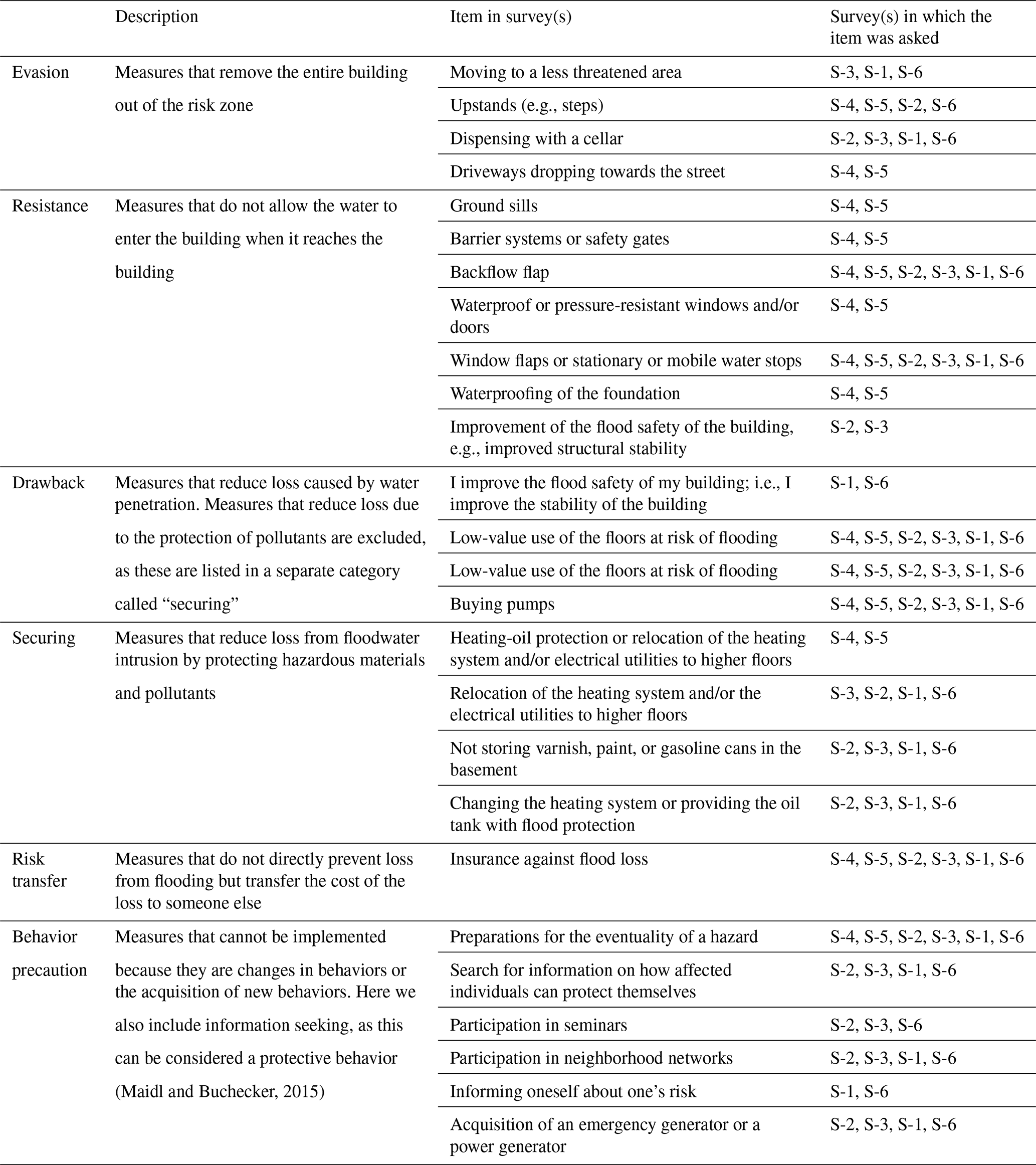

Data on what PLFRAMs were implemented before and after the damaging flood event were collected. However, the questions on PLFRAMs were not fully consistent across all surveys due to necessary adaptations to different survey and event contexts. In order to evaluate the implementation of PLFRAMs, all measures were assigned to six main groups based on their principal mode of functioning (Fig. 3), as described in current literature (DEFRA, 2008; Hudson et al., 2014; Kreibich et al., 2011; Lamond et al., 2018; Poussin et al., 2015). Table A1 (see Appendix) documents the PLFRAM queries in each survey and their assignment to these six groups. This paper does not assess the number of PLFRAMs implemented but only whether at least one PLFRAM from a respective group was implemented before or after the flood. It should be noted that this study and the available data cannot clarify if households adapted appropriately to their local flood situation. This is because the specific PLFRAM or combinations of PLFRAMs appropriate to an individual's flood risk depend on many personal and local factors for which no data were collected. On-site visits would be needed for such an evaluation.

For the analysis in this study, the respondents of the respective surveys were assigned to the urban pluvial flooding, flash flooding, and fluvial flooding flood types according to the definitions in Fig. 1 and based on pathways reported in the survey and further event contexts. Urban pluvial flooding was assigned to respondents affected by pluvial flooding in urban areas with no steep topography and possibly accompanied by overloaded sewer systems due to temporally and spatially limited heavy-rainfall events. This applies to those affected in the city of Münster and the smaller neighboring town of Greven (Spekkers et al., 2017), as well as those affected in Berlin, Potsdam, and Leegebruch (Dillenardt et al., 2022) and 448 surveyed households from S-3 (Thieken et al., 2022). The 53 households affected in the city of Remscheid are not included in the study, as Remscheid's steep topography differs too much from that of the other locations. The respondents to S-1 were assigned to the fluvial flood type, as flooding originated from the Rhine, Weser, Danube, and Elbe rivers (Thieken et al., 2022). During the flooding in June 2013, dike breaches occurred in the federal states of Bavaria and Saxony-Anhalt (Thieken et al., 2022). Respondents who experienced a dike breach were excluded from the analysis of this paper. Following the classification of Thieken et al. (2022), those from S-3 who were affected by flash floods were separated and assigned to the flash flooding flood type, while the remaining cases were considered urban pluvial flooding. All respondents from S-6 were also assigned to the flash flood type, as this was the primary flood type during the flood of July 2021.

Table 2Information on the demographic characteristics of surveyed households, with gender classified as follows: individuals who identify as female (f), individuals who identify as male (m), and individuals who identify as neither female nor male – categorized as “diverse” (d).

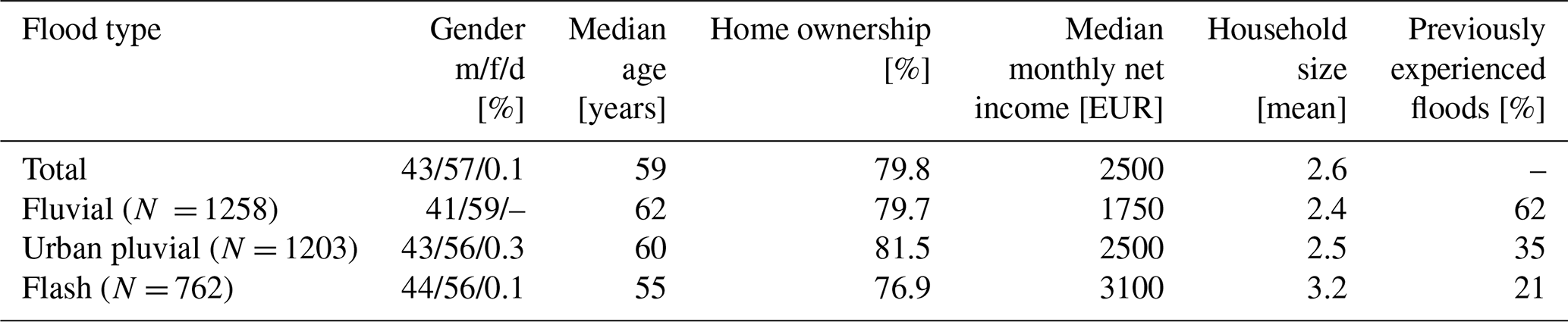

The demographics of the surveyed households are summarized in Table 2. The reported building losses were adjusted for inflation to 2022 levels based on the construction price index (DeStatis, 2023a). Losses to household contents were adjusted to 2022 levels based on the consumer price index (DeStatis, 2023b). Regardless of the flood type, more women (57 %) than men (43 %) participated in the surveys. The median age of the respondents was 59, which is approx. 8 years higher than the mean age of those over 18 years old in the German population (DeStatis, 2014). Mainly homeowners or apartment owners participated in the surveys (82 %). On average, 2.6 people lived in the households surveyed. More than half of those affected by fluvial flooding reported previous flood experience (62 %) since similar regions had already been affected in August 2002. In contrast, fewer respondents affected by urban pluvial flooding (35 %) or flash flooding (21 %) reported such experiences.

The data were analyzed using the statistical software package IBM SPSS 27. The abbreviation stands for “Statistical Package for the Social Sciences”. To identify significant differences between the three flood types, the Kruskal–Wallis test was performed. A Kruskal–Wallis test was first performed for each PMT factor for all three flood types. If the Kruskal–Wallis test showed no significant difference between the flood types, this is indicated in Table 4. If the Kruskal–Wallis test showed significant differences, single-factor analysis of variance (ANOVA) was performed to better understand the identified differences by comparing the flood types in pairs.

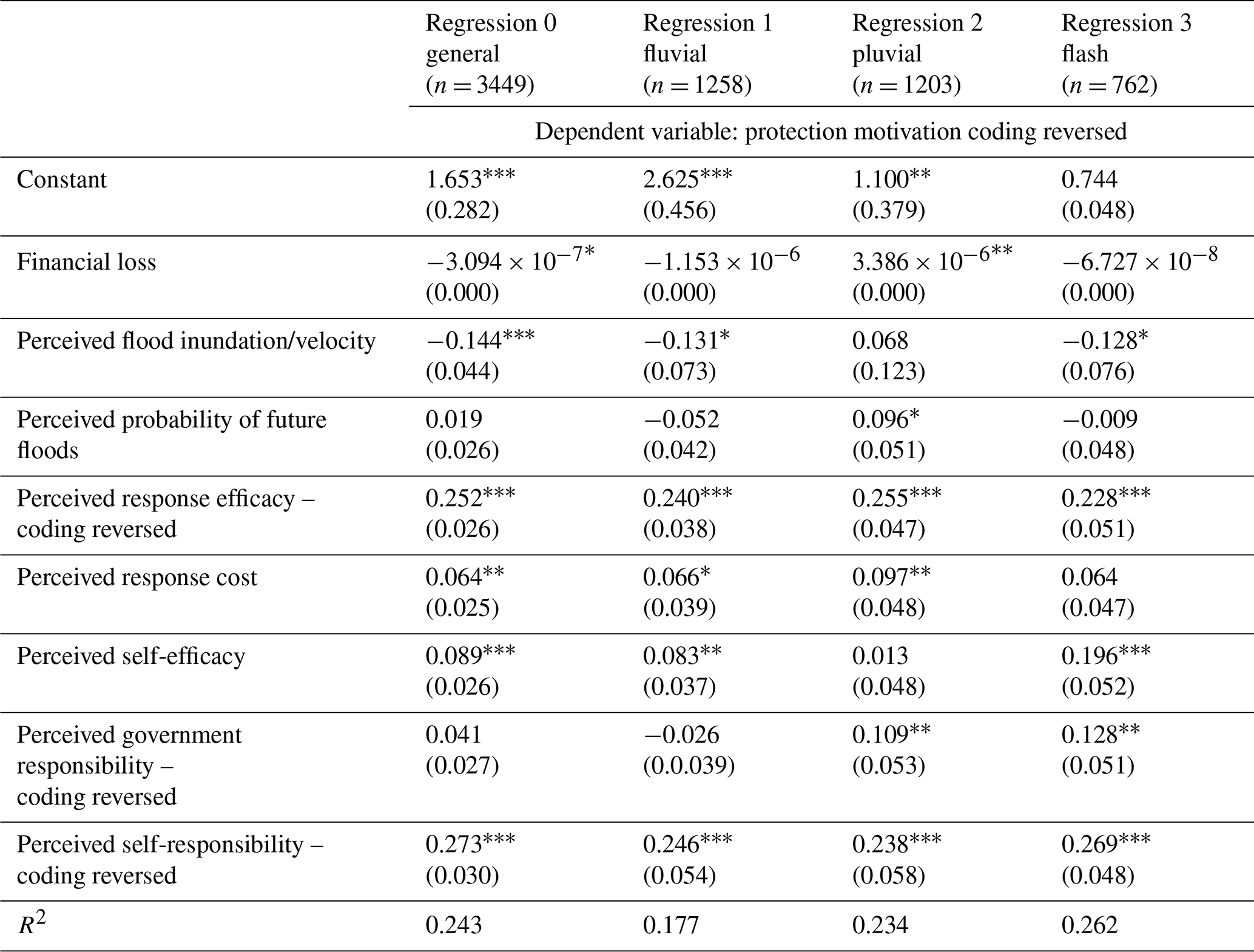

Linear regressions were carried out with IBM SPSS 27 to examine in the first step which PMT/PADM factors, i.e., threat, coping and responsibility appraisals, influenced the protection motivation of the respondents. The dependent variable for the regressions presented in Table 6 was protection motivation, derived from the “I will do everything possible to protect myself from flooding” item and the “I would recommend that others take private precautions” item (see Table A1 in the Appendix). These two items were combined so that the highest value was always taken for the combined variable. This combined variable enables us to capture protection motivation regardless of whether it relates to the respondent, as in the first item, or to others, as in the second item. In a second step, the PMT/PADM factors that significantly influenced protection motivation were examined to determine the framing factors that influenced them.

3.1 Comparing the perceived severity of the investigated flood types

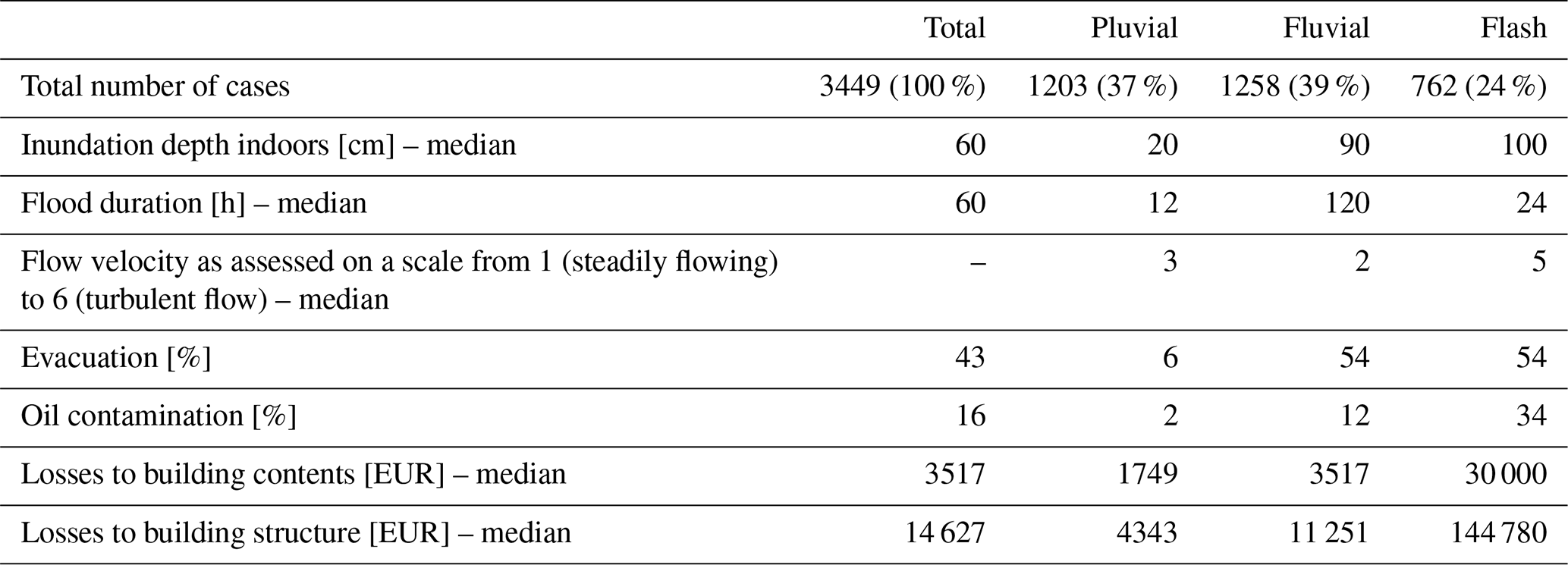

In order to characterize the different processes and impacts of the three flood types investigated, key variables are compared in Table 3. Additional data on the perceived flow velocity can be found in Table A1. Altogether, the data reveal that flash floods were particularly severe since those affected reported the most intense flow velocity, the highest losses to their buildings and building contents, and the highest water depth in their homes, and they were most likely to experience floodwater contaminated with fuel oil. About half of those affected had to be evacuated in both fluvial and flash flood events. Flood duration was particularly high in fluvial floods. Inundation indoors, duration, and contamination with fuel oil were the lowest for those affected by urban pluvial flooding. The same holds for financial losses.

Table 3Factors used to approximate the severity of the different types of flooding. The reported losses to the building were adjusted for inflation to 2022 levels based on the construction price index (DeStatis, 2023a). The losses to household contents were adjusted to 2022 levels based on the consumer price index (DeStatis, 2023b).

3.2 Comparison of the measures taken by those affected before and after a perceived flood

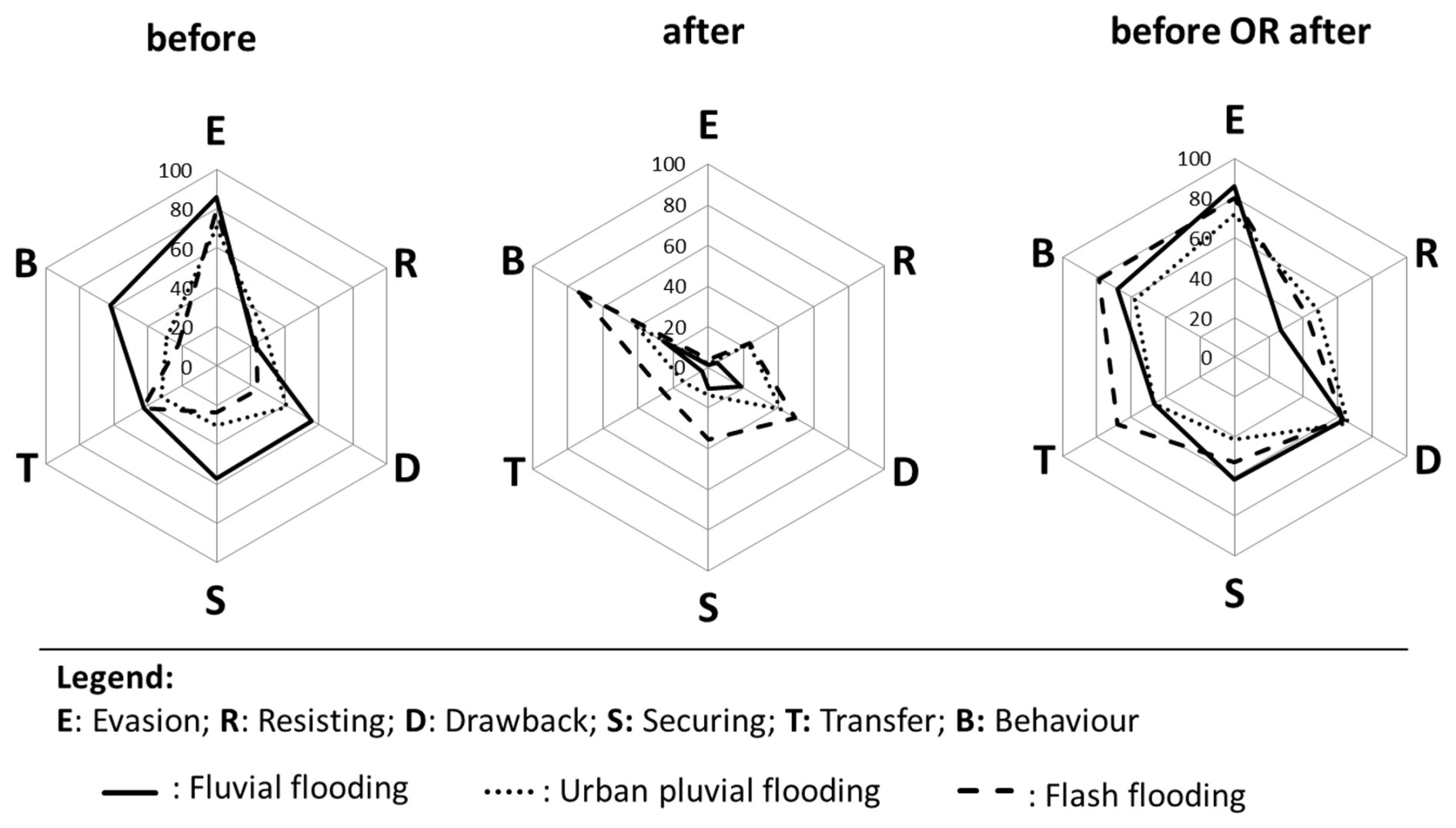

Figure 4 shows the share of surveyed households that implemented at least one PLFRAM from a given category (see Fig. 3 and A) of PLFRAMs before (Fig. 4, left) and/or after a flood (see Fig. 4, middle). The before-and-after results are summed up in Fig. 4 (right graph).

Figure 4Proportion of respondents per flood type who implemented at least one measure from a PLFRAM group before and/or after a flood.

Households affected by fluvial flooding in 2013 had implemented PLFRAMs most frequently before the event and very few measures after the event, while those affected by flash floods (in 2016 and 2021) had rarely implemented PLFRAMs before the event but frequently after the event. Those affected by fluvial or flash floods had taken out insurance before the last flood event in roughly equal numbers and more often than those affected by urban pluvial flooding. After the event, those affected by flash flooding were particularly likely to take out insurance, making them the most likely group for this kind of PLFRAM. After the event, roughly the same number of households affected by urban pluvial flooding and flash floods had implemented measures in the categories “resistance” and “drawback”. However, those affected by flash floods implemented measures in the category “securing” more frequently after they had been flooded.

Considering together the PLFRAMs implemented before and after the event, a pattern can be seen across the flood types. Preparedness measures were implemented quite frequently. Evasion measures were predominantly implemented before the most recent flood event. Drawback measures were implemented before and after with somewhat equal frequency by 60 % of respondents. In addition to the above-mentioned similarities, it is striking that those affected by fluvial flooding less frequently implemented resistance measures.

3.3 Comparing potential drivers of adaptive behavior

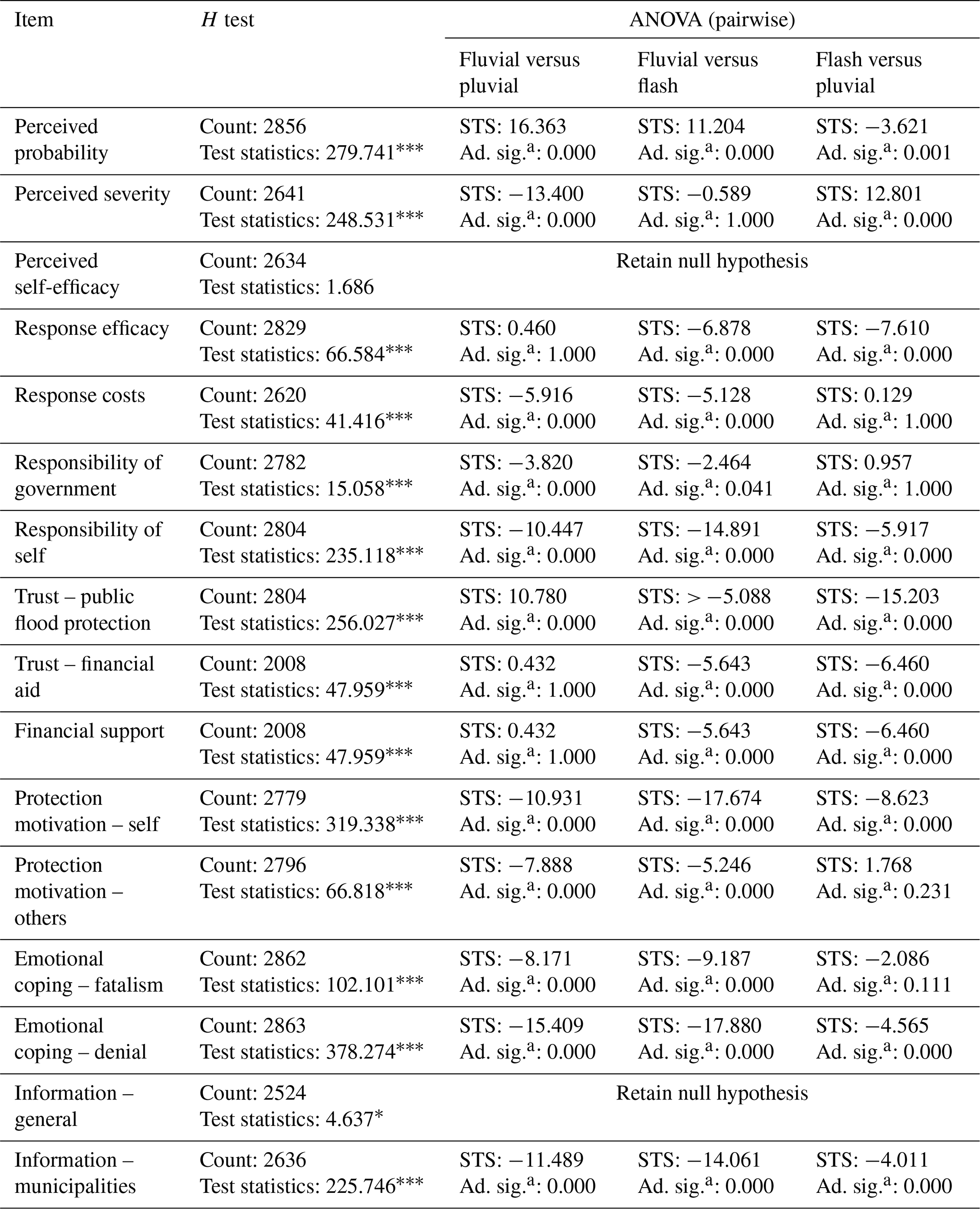

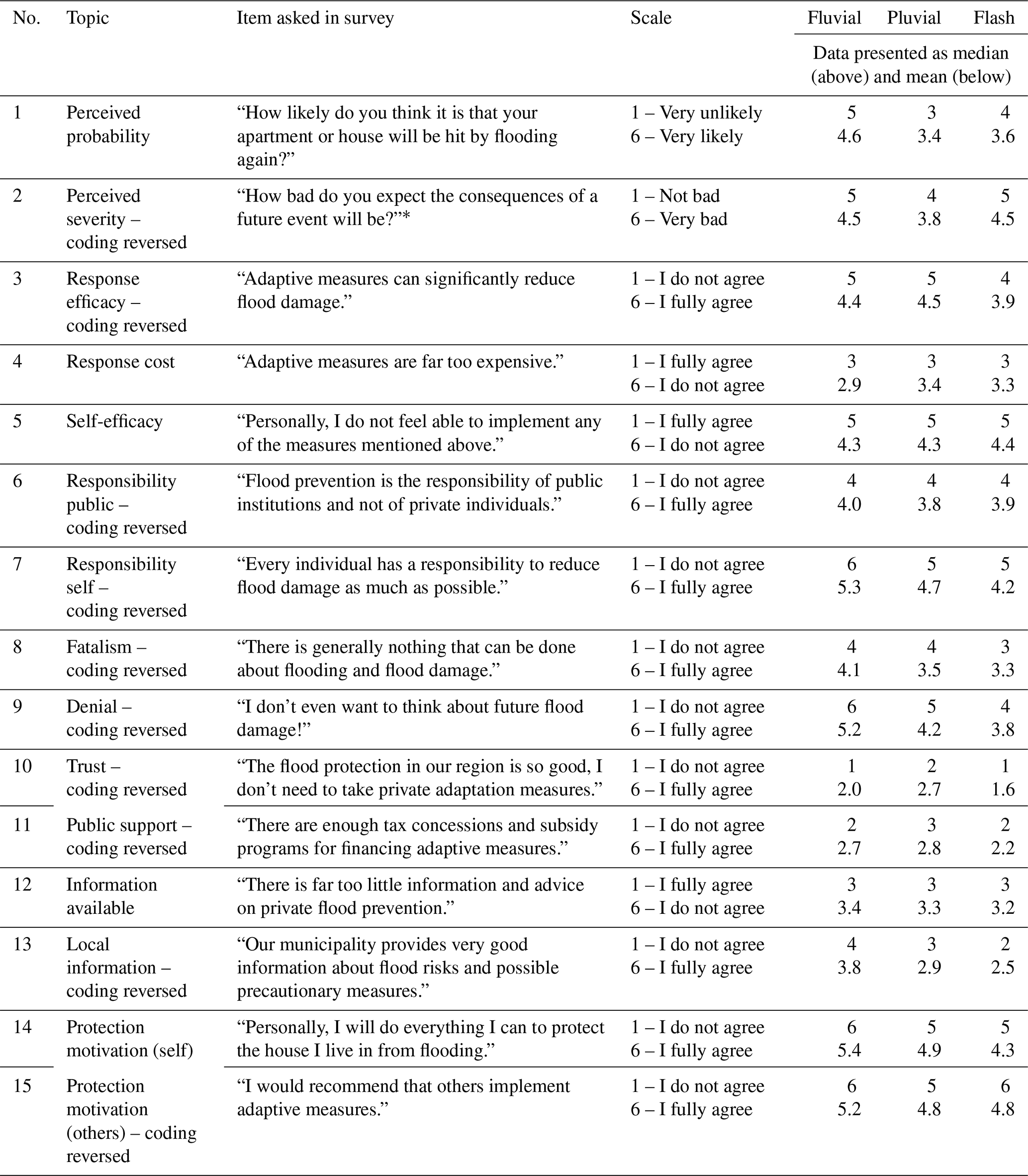

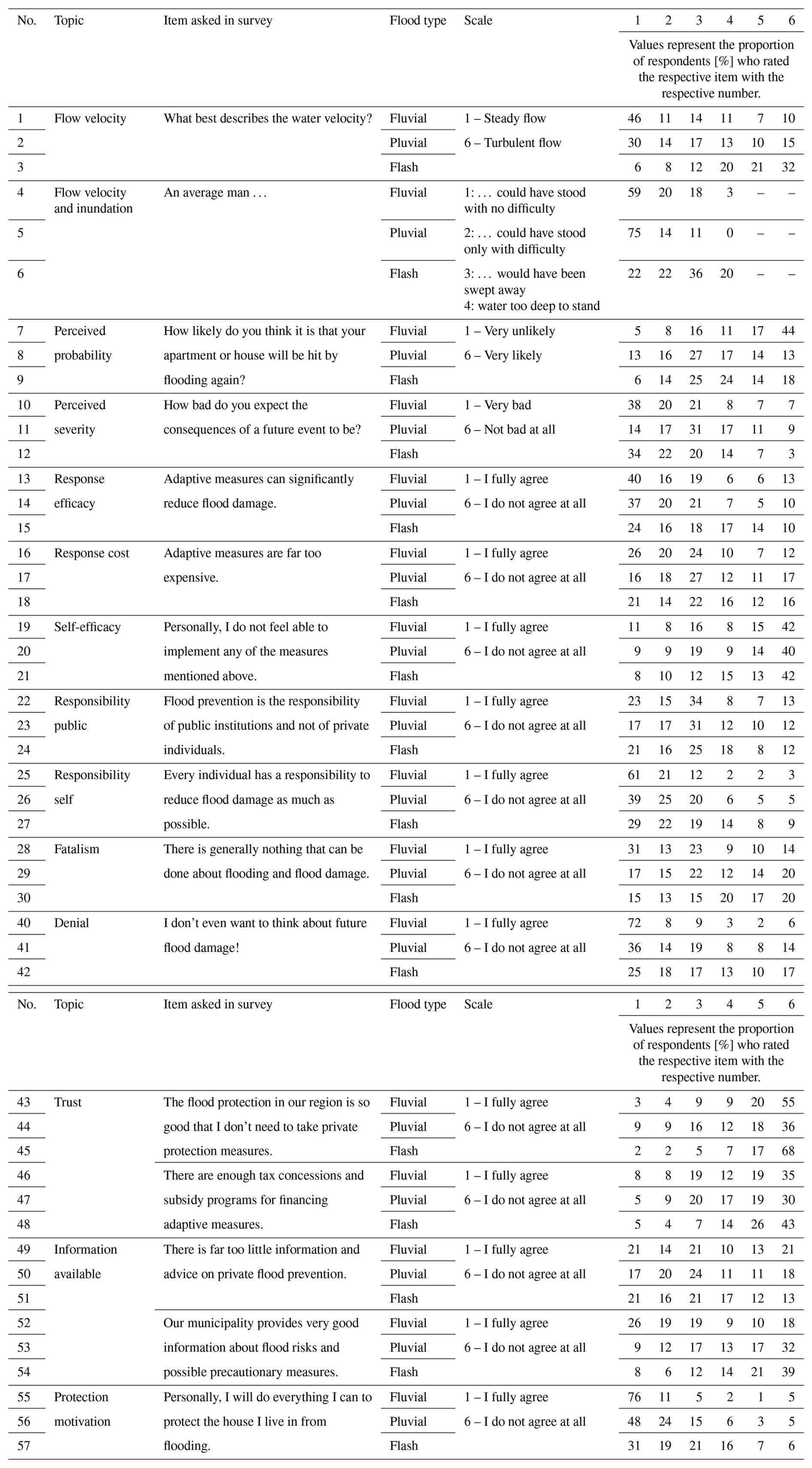

Table 4 compares the flood types in terms of respondents' attitudes towards adaptation to flood risk on the theoretical basis of the PMT and PADM, using Kruskal–Wallis tests and, if Kruskal–Wallis tests indicate differences, single-factor ANOVA. Table 5 shows the median and mean values of each item analyzed. More detailed information on the answers to the items can be found in Table A2 (see Appendix). The percentages show the proportion of respondents who selected either 1 and 2 or 5 and 6 on a scale from 1 to 6 and are derived from the data presented in Table A2.

Table 4Results of Kruskal–Wallis and ANOVA post hoc testsa: significance values are adjusted by Bonferroni correction for multiple tests. The number of cases used for this analysis is indicated by “count”; more details on the items can be found in Table A1.

∗ p < 0.1, p < 0.05, p < 0.01. STS – standardized test statistic.

Table 5Items asked in the surveys with the scales used and the answers per flood type (median and mean).

∗ As S-1 was designed as a panel survey and this item was not asked in the first wave of the survey, the results for this item are based on the results of the second wave of the panel survey, in which n = 710 households from the first wave took part.

With regard to threat appraisal, respondents rate the severity of a future flood as high (median values of 5 for fluvial, 4 for pluvial, and 5 for flash floods on a scale from 1 – not bad to 6 – very bad) but often do not believe that such a future event will affect them (median values of 5 for fluvial, 3 for pluvial, and 4 for flash floods on a scale from 1 – unlikely to 6 – likely). The group reporting high perceived severity is comparable in size to and, in some cases, larger than the group affected by fluvial or flash flooding when compared to those affected by urban pluvial floods. As for the rating of the probability of a future event, Table 5 shows a gradient from those affected by urban pluvial flooding, who rate the probability of a future event the lowest (median: 3), followed by those affected by flash flooding (median: 4) and those affected by fluvial flooding, who rate the probability of being affected again the highest (median: 5).

Coping appraisal is investigated by looking at perceived self-efficacy, perceived response efficacy, and the perceived response cost. Self-efficacy is rather high for around 60 % of respondents and comparable across all samples and flood types, indicating that self-efficacy is person-related rather than event- or flood-type-related. Most of those affected by urban pluvial and fluvial flooding tend to have a high and comparable response efficacy (median: 5), while this proportion is lower for those affected by flash floods (median: 4). About 60 % of those affected by urban pluvial floods and 56 % of those affected by flash floods perceive the response costs as (too) high and are comparable in this respect. This proportion is higher for those affected by fluvial floods (69 %).

Self-responsibility is perceived as high by all respondents. However, the level of self-responsibility is higher among those affected by fluvial flooding (median: 6) than among those affected by urban pluvial or flash flooding (median: 5). At the same time, those affected by fluvial, urban pluvial, or flash floods believe that public institutions have a responsibility to implement flood protection measures (median: 4). However, only flash and pluvial flooding are comparable here (see Table 4), and the mean values in Table 5 reveal that those affected by fluvial flooding stand out in seeing public institutions as slightly more responsible. However, most of those affected by flooding (median: 1–2) have little confidence in public flood protection measures. Moreover, most people affected by flooding lack confidence in state financial aid (median: 2–3).

In general, most respondents believe that there is enough information available about flooding and flood adaptation (median: 3). However, fewer respondents affected by urban pluvial (median: 3) and flash flooding (median: 2) believe that there is enough local information available from the municipalities. Those affected by fluvial floods stand out here, as they tend to feel better informed by their municipalities (median: 4).

Regardless of the type of flooding, over 70 % of respondents have a rather high motivation to protect themselves and/or would recommend others to do the same. A gradient can be seen in the motivation to protect oneself (fluvial – median: 5.5, pluvial – median: 4.9, and flash – median: 4.3; see Table 5). The proportion of respondents showing signs of fatalism is higher among those affected by fluvial and urban pluvial flooding (median: 4) than among those affected by flash flooding (median: 3). The proportion of respondents showing signs of denial is high among those affected by fluvial flooding (median: 6) and less high among those affected by urban pluvial and flash flooding (median: 4–3). Hence, the group affected by fluvial flooding demonstrates that high protection motivation and emotional coping are not mutually exclusive.

3.4 Results of regression analyses

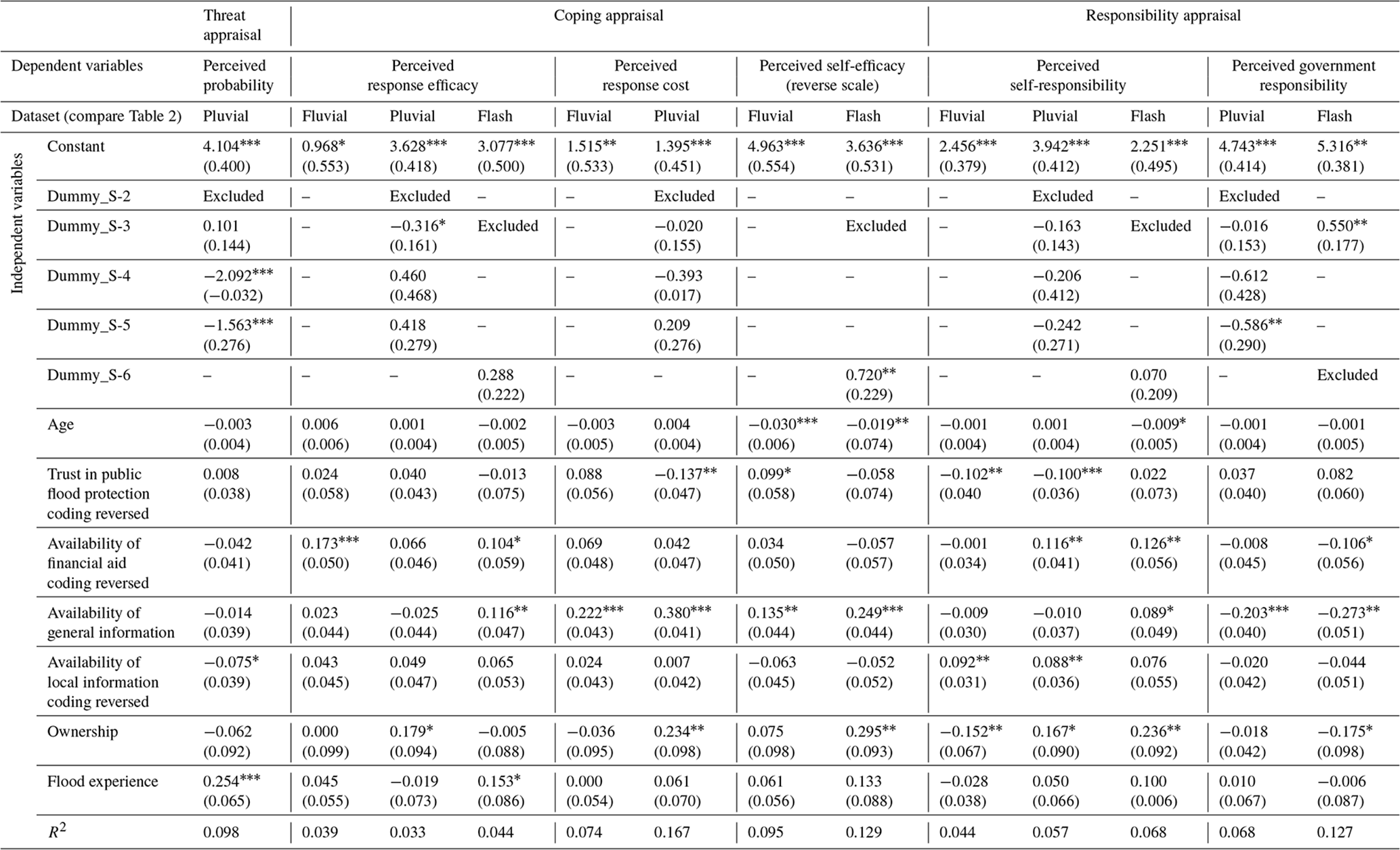

The PMT/PADM aspects analyzed in this study and how they affect protection motivation were tested in regressions 1–3 (see Table 6). After identifying the PMT/PADM aspects that showed significant influences in the respective flood type contexts, framing factors influencing them were investigated (see Table 7). This table shows the dependent variables of all linear regressions in the second row (“dependent variables”). “Perceived flood inundation/velocity” corresponds to item no. 4 in Table 1, namely “An average person could have stood with no difficulty”. The flood types were considered in all linear regressions presented here, meaning that the datasets presented in Table 2 were used. Each column in Tables 6 and 7 represents a linear regression. All PMT/PADM aspects examined show significant influences for at least one type of flooding, which indicates the suitability of the PMT/PADM-based hybrid framework for starting a discussion on the factors influencing protection motivation in the context of flooding. Only significant correlations are discussed hereafter. Correlation coefficients are shown in parentheses.

Table 6Results of regression analysis. The dependent variable for all four regressions is the protection motivation of households. Standard errors are in parentheses.

Significance is indicated as follows: ∗ p < 0.1, p < 0.05, p < 0.01.

Table 7Results of regression analysis for those affected by fluvial flooding. Dependent variables (first line) are those in Table 6 (fluvial, column 3) that are significant; standard errors are in parentheses.

Significance is indicated as follows: ∗ p < 0.1, p < 0.05, p < 0.01.

The influence of threat appraisal on protection motivation is examined through the perception of the flood inundation/velocity of the last flooding and the perceived probability of future flooding. Protection motivation is negatively linked to perceived flood inundation/velocity for those affected by fluvial flooding (−0.131) and flash flooding (−0.128). Hence, the last event's perceived severity may inhibit protection motivation. However, only for those affected by urban pluvial flooding are financial losses positively linked to protection motivation (3.386 × 10−6). This link appears minimal because this item is not on a scale from 1 to 6. Instead, this item captures the overall loss in euros. Therefore, the financial loss experienced seems to trigger protection motivation only if high losses have been experienced. The link between the perceived probability of a future event and protection motivation in the context of pluvial flooding is positive but minimal (0.096).

The influence of coping appraisal on protection motivation is analyzed through perceived response efficacy, perceived self-efficacy, and perceived response cost. Perceived response efficacy is highly significant across all types of flooding (see Table 6) and thus influences the protection motivation regardless of flood type. Perceived self-efficacy positively influences the protection motivation of those affected by fluvial (0.083) or flash (0.196) flooding, which is in line with PMT. Response costs are positively linked to protection motivation in fluvial flooding (0.066) and in the context of pluvial flooding (0.097); however, those linkages are minimal.

The influence of responsibility appraisal on protection motivation is analyzed through perceived self-responsibility and perceived government responsibility. A positive linkage between perceived self-responsibility and protection motivation is found across all types of flooding (see Table 6). Thus, the assessment of self-responsibility influences the protection motivation, regardless of the type of flooding. Protection motivation is positively linked to government responsibility for those affected by pluvial (0.109) and flash (0.128) flooding. In conjunction with the positive influence of a sense of personal responsibility, communicating responsibilities in general may positively affect the motivation to adapt.

The PMT factors identified as significant in Table 6 were then analyzed to determine the extent to which they were influenced by framing factors. However, the framing factors analyzed can only be a starting point for investigating the influences of framing factors and are limited to those included in the surveys. In order to see the extent to which event-specific and, thus, survey-specific factors could influence the PMT factors, dummy variables have been used in these analyses. A dummy variable for each survey from Table 2 was created and implemented in the linear regressions of the urban pluvial and flash flooding types. As the data on fluvial flooding originate from one survey, no dummy variables were created for this type of flooding. Only significant results are presented below. All results can be found in Table 7. The financial loss incurred and the flood inundation/velocity were not investigated. R2 is generally lower than in the regression analyses of the PMT factors. This indicates that the independent variables do not yet include all framing factors that would reveal influences in these contexts. Nevertheless, the incomplete list of framing factors is used to identify meaningful relationships between PMT/PADM aspects and framing factors.

The event-specific dummy variables improve the R2 of the regression models and capture influences that distinguish those affected by a particular event from others affected by the same type of flood. These event-specific effects can be time-, survey-, or location-specific, although it is impossible to break this down precisely based on our data. The perceived probability of a future event is lower among those who experienced urban pluvial flooding events in Berlin, Potsdam, and Leegebruch. The response efficacy was lower among those affected by urban pluvial flooding in 2016. The residents of Berlin stand out for perceiving government responsibility as lower.

Regarding flash flooding, those affected by the event in 2021 stand out with a high perceived self-efficacy, while those affected in 2016 perceived government responsibility as high. However, it must be mentioned at this point that what causes these differences on the basis of our data cannot be separated. Therefore, it remains open to interpretation and discussion as to whether these are local aspects or aspects specific to the survey. Further research is needed in this respect.

Increasing age is negatively linked to respondents' self-efficacy in the context of fluvial (−0.030) and flash (−0.019) flooding. Older people, therefore, tend to feel unable to implement PLFRAMs. Increasing age is negatively linked to perceived self-responsibility in the context of flash flooding (−0.009), which indicates that self-responsibility assessment decreases with increasing age. Confidence in public flood defenses is negatively related to the perceived response costs for pluvial flooding (−0.137), which indicates that people with a high level of confidence in public flood defenses tend to rate the costs of PLFRAMs as (too) high. When respondents have high trust in public flood defenses, they show a higher perceived self-efficacy in the context of fluvial floods (0.099) but a lower perceived self-responsibility in the context of fluvial (−0.102) and pluvial (−0.100) floods. The overall picture suggests that trust in public flood protection can be a rather hindering factor in promoting adaptive behavior.

A positive perception of the availability of financial support increases perceived response efficacy in the context of fluvial (0.173) and flash (0.104) flooding. In addition, there is a positive link between the perception of financial aid and perceived self-responsibility in the context of pluvial (0.166) and flash (0.126) flooding. Both perceived response efficacy and perceived self-responsibility were identified as the clearest triggers of protection motivation in the analysis (see Table 6). Since the perceived availability of financial aid enhances them, communicating financial aid may be crucial to support the implementation of PLFRAMs. Furthermore, the perceived availability of financial aid is negatively linked to the perceived government responsibility in the context of flash flooding.

Availability of general information has been shown to positively influence perceived response efficacy in the context of flash floods (0.116), perceived response costs in the context of fluvial (0.222) and pluvial (0.380) floods, and self-efficacy in the context of fluvial floods (0.135) and flash floods (0.249). The availability of general information has been shown to negatively influence self-responsibility for flash floods (−0.089) and government responsibility for pluvial floods (−0.203) and flash floods (−0.273). The overall picture thus shows that a positively perceived availability of general information can promote adaptive behavior, in which those affected see the government as less responsible and, at the same time, assess the costs and feasibility of measures more positively. While the availability of general information impacts the perception of the government's responsibility, it is information from the municipalities that might promote the perception of personal responsibility among the respondents, at least in the context of fluvial (0.092) and urban pluvial (0.088) flooding. However, in the context of pluvial flooding, the availability of local information links negatively with perceived probability of a future event (−0.075), which might suggest that it is challenging to communicate occurrence probabilities, as suggested in the literature (Grounds et al., 2018).

There is a positive connection between ownership and perceived response efficacy (0.179) and perceived response cost (0.234) in the context of pluvial flooding. In the context of flash flooding, ownership links positively with perceived self-efficacy (0.295) and negatively with perceived government responsibility (−0.175). Ownership further links positively with perceived self-responsibility in the context of pluvial (0.167) and flash (0.236) flooding but negatively in the context of fluvial flooding (−0.152). Hence, homeowners affected by flash flooding tend to see themselves, rather than the government, as responsible. Previously experienced floods positively affect the perceived probability of a future event occurring in the context of pluvial flooding (0.254). Flood experience positively affects the perception of response efficacy in the context of flash flooding (0.153).

4.1 Adaptive responses to the different flood types

At 95.6 %, most respondents (98.6 % of those affected by fluvial, 97.5 % of those affected by flash, and 91.5 % of those affected by urban pluvial flooding) had implemented at least one PLFRAM before or after the damaging event regardless of flood type. This reflects the generally progressed adaptation of those affected by flooding and the boost in adaptation after damaging events. Respondents were particularly likely to adapt their behavior by, e.g., seeking information, attending seminars and neighborhood assistance meetings, creating emergency plans, or implementing other preparatory measures (e.g., procuring pumps). This is consistent with the findings of Grothmann and Reusswig (2006), who found that searching for flood-related information is the most frequently performed adaptation. These positive attitudes towards preparedness measures do not directly reduce future damage but demonstrate the need for information after a flood.

Evasion measures were very rarely implemented after an event (see Fig. 4). Since measures in this group are difficult to implement retroactively, such as making driveways drop towards the road, and also require great effort, such as moving to a less flood-prone area, it is likely that these measures undergo individual cost–benefit assessments. They are much easier to be implemented when planning or constructing a home and should thus be communicated to people involved in construction projects. In contrast, the possibility of taking out insurance could be communicated before and after events. Communication on this topic is likely to have an impact. In Germany, mandatory flood insurance has been discussed since the devastating floods of 2002 (Thieken et al., 2006). Market penetration has increased from 19 % in 2002 to 49 % in 2021 (GDV, 2022) and to 52 % in 2022 (GDV, 2023).

Furthermore, our data show that the uptake of insurance policies covering flood losses before the last event was around 40 % among all households surveyed. Insurance was purchased after flooding, especially by those who were affected by flash flooding. This makes sense since the amount of flood losses by flash floods is very high (see Table 3), and people with insurance can generally rely on loss compensation based on the insurance contract.

4.2 Appraisal of threat, coping, and responsibility in the context of different flood types

The appraisal of threat is assumed to be a crucial driver in the PMT and PADM. It is formed by the perceived severity and perceived probability (of a future event) and is expected to influence protection motivation positively if the perceived threat is not too high (Grothmann and Reusswig, 2006; Lindell and Perry, 2012; Prentice-Dunn and Rogers, 1986). Fluvial floods were perceived as more devastating than urban pluvial floods but less devastating than flash floods. Hence, our analyses illustrate that the respondents perceived the flood types examined very differently. These perceptions are confirmed by research on events not analyzed in this study. Poussin et al. (2014) found for flooding in France that fluvial floods caused less damage and fewer fatalities than flash floods, and Spekkers et al. (2017) observed rather minor water depth during an urban pluvial flood in Amsterdam and did not report any fatalities. In contrast to flash flooding, urban pluvial events were perceived as the least severe in our data.

Those affected by fluvial floods report a higher perceived severity and a higher probability of future flooding, which might also be due to repeatedly experienced flooding of this type. Since this group had also implemented the most PLFRAMs before the event, our data do not allow us to observe the negative feedback loop between the implementation of PLFRAMs and the appraisal of the threat that was described by Bubeck et al. (2012) and confirmed by Poussin et al. (2014) for the context of fluvial events. Our data suggest that the implementation of PLFRAMs in the past did not lower the respondents' assessment of the threat or that the assessment of the threat, which may have decreased after the implementation of PLFRAMs, increased again after experiencing another flood. However, in this context, the fact that those who were affected by fluvial flooding retrofitted fewer PLFRAMs after the last flood event may indicate that if those affected by floods implement PLFRAMs and then experience flooding and losses again, their higher risk assessment may lead not to the implementation of more PLFRAMs but rather to higher maladaptive thinking, as maladaptive thinking was particularly pronounced in those affected by fluvial flooding.

The regression analysis of PMT/PADM aspects (see Table 6) reveals no significant link between the perceived probability of a future event and protection motivation for fluvial and flash flooding, which aligns with findings in Australia (Bird et al., 2013). For all respondents, the mean of the perception of a flood's severity is higher than its perceived probability, indicating that many of those affected are aware that flooding can cause high levels of losses but that they might not be affected by it (again), which is in line with findings of Netzel et al. (2021) in the context of urban pluvial flooding. Communicating the probability of future events occurring in a particular locality may, therefore, be a way to enhance one's local risk awareness. Return periods may not be the most suitable tool here (Grounds et al., 2018) since they suggest long time periods between flood events if not well explained. Perceived inundation/velocity showed an effect that decreased the motivation to protect oneself in the context of fluvial and flash floods, which were perceived as more severe. In the context of urban pluvial flooding, financial losses trigger protection motivation if those losses are high. Future information campaigns for urban pluvial flooding could, therefore, communicate high losses, if those are to be expected in a specific area.

In addition to assessing the threat, it is the assessment of coping options that shapes adaptive behavior and is perhaps even the stronger driving force here (Poussin et al., 2014). Therefore, it is a positive aspect that most respondents, after an event, tend to believe that PLFRAMs reduce flood damage and that they can implement these measures. They thus generally tend to perceive both a high sense of self-efficacy and a high perceived response efficacy. Perceived response efficacy has been found to positively influence protection motivation regardless of flood type. The fact that those affected by flash flooding have a lower perceived response efficacy but less often perceive the costs of measures as too high may suggest that this group of respondents experienced particularly severe flooding, undermining the effectiveness of many PLFRAMs and putting their costs into perspective. Therefore, cost–benefit analyses of PLFRAMs could be carried out on a flood-type-specific basis and communicated to those potentially affected. For urban pluvial flood events in particular, it should be investigated which PLFRAM can reduce the expected damage cost-effectively since floods of this type are characterized as less severe (see Table 3). Those affected perceive response costs to be rather high (see Table 5). Often, only small changes to a building, e.g., the implementation of ground sills, might help prevent water from entering the building.

Responsibility appraisal is expected to positively influence protection motivation. This study divides responsibility appraisal into one's own perceived responsibility and the perception of the government's responsibility. The regression analyses revealed that self-responsibility positively affects protection motivation, regardless of the type of flooding, and that perceived government responsibility in the context of pluvial and flash flooding has a positive influence on protection motivation. Among those affected by floods, the sense of responsibility is generally high (see Table 5). Studies have shown that homeowners feel a greater sense of responsibility (Dillenardt et al., 2022; Grothmann and Reusswig, 2006). As over 80 % of respondents were homeowners (see Table 2), this might explain the high sense of responsibility observed. At the same time, respondents also place responsibility on public authorities. Thus, these two perceptions are not mutually exclusive. This is in the spirit of integrated flood risk management. However, over 70 % of all respondents have little or rather little confidence that the public sector will fulfill the responsibilities they ascribe to it (see topic no. 11 in Table 5). This suggests that clear communication and confidence-building actions among all stakeholders involved in integrated flood risk management should be strengthened.

4.3 Framing factors: a chance to enhance adaptive behavior?

Framing factors offer the opportunity to discuss the influences of, e.g., respondents' age, the availability of general or local information, the perceived availability of financial aid, and flood experience on adaptive behavior (i.e., the implementation of PLFRAMs). The influence of framing factors is either indirect via the influence on threat, coping, or responsibility appraisals or direct if the framing factor prevents the implementation of measures despite a high motivation of those affected, thus acting as a barrier. This study focuses on the indirect effects of the framing factors mentioned. The importance of framing factors for developing protective behavior has already been addressed by Prentice-Dunn and Rogers (1986) in protection motivation theory, in which the influence of “source information” on threat and coping appraisal is mentioned. Lindell and Perry (2012) extend this understanding by stating that those factors form a framework; i.e., they are both at the beginning of the development of a protective response (indirect influence), meaning they can directly hinder or promote the implementation of protection motivation in a protective response. Although the naming of this group of factors differs, other studies discuss framing factors. Fuchs et al. (2017) describe “situational factors”, which include “being informed”, for example, and assign them to a superclass of “social capital”, which is assumed to have a positive influence on the implementation of measures.

The regression analysis of the framing factors shows low R2 values. This is a known problem in psychological research. People are very different, but they do not participate in interviews that last longer than 30 min, making it impossible to include all personal and contextual factors (Grothmann and Reusswig, 2006). However, conclusions from the results should be drawn with caution. Our analyses show that home ownership indirectly promotes the motivation to protect oneself by strengthening coping and responsibility appraisals, which is in line with Grothmann and Reusswig (2006), who showed that ownership as a framing factor can positively influence the implementation of measures. In the context of fluvial and flash flooding, the age of affected respondents was linked negatively to their self-efficacy. Hence, older people, if they have experienced rather severe flooding, are less likely to see themselves in a position to implement PLFRAMs. However, Houston et al. (2021) found that households with older adults show less long-term flood impacts and suggested that this is caused by their social capital (e.g., social networks and knowledge). Information campaigns should build on this and pay particular attention to older people in flooded areas by enhancing or, if possible, profiting from their social capital and, at the same time, identifying who could help them during the implementation process of PLFRAMs and recommending that they not select measures that require action during an event, such as mobile devices that need to be installed. Both perceived response efficacy and perceived self-responsibility were identified as the clearest triggers of protection motivation in the regression analysis presented in Table 6. Since the perceived availability of financial aid enhances them, communicating financial aid may be crucial to support the implementation of adaptive measures. This argument is strengthened by the findings of Houston et al. (2021), who show the sensitivity of individuals' vulnerability and resilience to financial resources.

Our data suggest that those with little flood experience, i.e., those affected by urban pluvial or flash floods, were particularly likely to take action after the last flood. In contrast, those with more flood experience, i.e., those affected by fluvial floods, were particularly likely to have taken action before the last flood and were less likely to take further PLFRAMs. In this context, however, it should be considered that flood experience is characterized not only by the pure experience of the flood but also by the experience of the reconstruction process and possibly subsequent adapted integrated flood risk management, as was the case, for example, after the 2002 and 2013 floods in Saxony (Müller, 2013). Such management, which includes the creation of flood hazard maps and information campaigns aimed at the population, may benefit peoples' perceptions of the threat, coping options, and responsibilities. Past research has shown a positive effect of (targeted) information campaigns on flood adaptation (Erdlenbruch and Bonté, 2018). While this relationship cannot be examined based on the data, the data do reveal that those who have been affected by fluvial floods – who, according to our data, are also those who have the most flood experience – have a higher risk perception, a higher perceived response efficacy, a higher sense of personal responsibility, and a higher motivation to protect themselves. They also feel better informed by their communities (see Table 5) and are more likely to have had implemented PLFRAMs before the last flood event (see Fig. 4). Future research should focus on these relationships in order to better understand the extent to which integrated flood risk management of fluvial floods has had a positive impact on the adaptive behaviors of households. In the context of different types of flooding, it should then be considered whether similar management approaches should be adapted and applied to other types of flooding.

4.4 Protection motivation and emotional coping: an interaction still not sufficiently understood

Overall, the protection motivation of all respondents is positive or rather positive, and those affected by fluvial flooding in particular have a high motivation to protect themselves from future events. At the same time, most interviewees agree with statements indicating they will face future events with denial and fatalism. Denial and fatalism are markers of a non-protective response, as defined by Grothmann and Reusswig (2006), and are also referred to as emotional coping or maladaptive thinking in other studies. Grothmann and Reusswig (2006) conclude from their own and other studies that a non-protective response has a negative/hindering effect on protection motivation.

For respondents who were affected by fluvial flooding, our results show that high ratings for denial and fatalism and a high protection motivation are not mutually exclusive but can instead coexist, which might be caused by repeated flooding and decreasing resilience, as indicated by other studies (Houston et al., 2021; Köhler et al., 2023). This may indicate that protective motivation is promoted regardless of maladaptive thinking if the assessments of threat, coping, and (personal) responsibility are high. However, it has been found that those affected by fluvial flooding implemented fewer measures after the event than the other respondents. This might suggest that a protective response results from the interaction between maladaptive thinking and protection motivation. Our data show that, at least in the context of fluvial flooding, the high sense of self-responsibility is not enough to stop those affected from developing a non-protective response. However, self-responsibility was found to hinder maladaptive thinking in the context of urban pluvial flooding (Dillenardt et al., 2022). Hence, interconnections among the factors of PMT and PADM are not yet fully understood, particularly in the context of different flood types, and the exact role of maladaptive thinking cannot be conclusively clarified. Further research is needed on this topic. For instance, future research could use qualitative interviews to identify or confirm items to capture maladaptive thinking within future survey campaigns.

4.5 Limitations

In this study, people affected by different types of flooding have been compared. Therefore, several surveys have been conducted. Between 2013 and today, our survey methodology has evolved from computer-aided telephone interviews (CATIs) to computer-assisted web interviews (CAWIs); see Fig. 2. The reason for this is that the use of mobile phones has increased rapidly in the last decade, and it can no longer be assumed that a balanced sample can be reached via landline. As a result, the fluvial group is homogeneous in terms of methodology (CATI), while the urban pluvial and flash flooding groups are mixed in terms of sampling methods used. One limitation in this context is that it is almost impossible to derive response rates for a CAWI advertised via social media, as it is impossible to conclusively determine how many people were reached through the original advertisement or through sharing of the survey link by those initially reached by the advertisement. In addition, a study conducted in Australia by Gilligan et al. (2014) indicates that participants recruited through Facebook may be more socially engaged, be better educated, and have higher earnings than the general population. In our study, however, the CAWIs within a flood type group were not advertised exclusively via social media but also via direct mail. It can be assumed that the mixed use of methods minimizes those effects.

In addition to these limitations, which can be attributed to the combination of sampling methods, it is possible that our surveys were unable to reach those affected who had moved to a new place of residence after experiencing flooding. This is supported by the fact that around of the letters sent out by the municipality as part of the survey conducted in the wake of the 2021 flood have been undeliverable. This group could, therefore, be underrepresented in sample D (see Fig. 2). However, the applied combination of sampling methods will likely reduce that effect within the overall group affected by flash flooding. Shaver et al. (2019) point out that Facebook uses a non-random targeting algorithm.

Furthermore, our survey exclusively targeted affected households. Our sampling based on advertisements via Meta is, therefore, non-random, and our results only reflect the perceptions of those affected and not those of unaffected households. In addition, our surveys were conducted exclusively in Germany. The transfer to other regions must, therefore, be scrutinized in advance. For example, it can be assumed that the sense of responsibility of those affected by floods differs between countries (Andrasko, 2021).

Regarding implementing PLFRAMs, this study and the available data cannot clarify the extent to which households adapted appropriately before or after the flood. This is because which PLFRAMs or combinations of PLFRAMs are appropriate to the individual flood risk depends on many individual and local factors for which no data were collected. Furthermore, it is not possible to conclusively clarify how much financial resources, time, and/or construction effort was required by those affected to implement PLFRAMs. This is because the classes used differentiate between PLFRAMs in terms of their mode of action and not in terms of implementation costs or effort.

This paper examined and compared the adaptive behavior of households that experienced urban pluvial flooding between 2014 and 2019, flash flooding in 2016 or 2021, and fluvial flooding in 2013 in Germany. The findings are based on several post-event surveys that were analyzed descriptively via Kruskal–Wallis tests, single-factor ANOVA, and linear regressions. The theoretical frameworks of PMT and PADM are used to structure our analyses and discuss our results in a way that allows us to draw practical conclusions for future risk communication strategies.

The communication of the threat should include the probability of future events, particularly those at risk of urban pluvial flooding, and communicate high flow velocities and water inundations if those are expected. The local context must be established so that those affected can become aware of their individual risk. Our results suggest that information campaigns should focus on informing affected individuals about PLFRAMs and responsibilities. Flood-type-specific recommendations and cost–benefit analyses should be carried out. The results of such analyses should be communicated to specific target groups so that the measures can be adapted to the expected severity and hydraulic forces. Care should be taken to ensure that the communicated PLFRAMs can be implemented by the target group, e.g., evasion measures by those involved in house construction. It may be advisable to incorporate the implementation of PLFRAMs into the planning and permitting process. As respondents show very little trust in the public sector's ability to deal with floods, especially after events that are perceived as very severe, communication strategies should include confidence-building strategies and communicate responsibilities. Those affected are open to information campaigns, particularly after a flood event, but these campaigns should be flood-type-specific.

Our results suggest that investigating framing factors enhances the discussion about households' adaptive behavior. In this context, whether and how the perceived availability of information and financial aid, flood experience, and home ownership promote aspects of PMT and PADM have been discussed. It has been found that the perceived availability of financial aid and information positively impacts coping appraisal and that community-led information campaigns are more likely to increase peoples' sense of personal responsibility. However, the interaction of these factors and the effect of maladaptive thinking within the development of adaptive behavior are not yet sufficiently understood, neither in our study nor in the wider literature. Further research is needed, as a better understanding can strengthen future risk communication strategies.

Table A1Summary of the measures, their definitions, and the survey items assigned to them, based on and updated from Dillenardt et al. (2024). For more information about the surveys, see Table 1.

Table A2Items asked in the surveys, their respective scale, and the respondents' answers in percent.

The analyses were performed using a commercial software (IBM-SPSS) and, thus, the code is not publicly available.

Some of the data sets (S1, S2) are available in HOWAS21 (https://howas21.gfz.de/, GFZ, 2025); others (S3, S6) will be included soon. However, not all variables used in this paper can be found in HOWAS21. The whole data set can be provided by the authors upon reasonable request.

LD carried out the conceptualization, curated and analyzed the data, and prepared the paper. AHT contributed to the writing through review and editing and providing resources and supervision.

The contact author has declared that neither of the authors has any competing interests.

Publisher's note: Copernicus Publications remains neutral with regard to jurisdictional claims made in the text, published maps, institutional affiliations, or any other geographical representation in this paper. While Copernicus Publications makes every effort to include appropriate place names, the final responsibility lies with the authors.

This article is part of the special issue “Strengthening climate-resilient development through adaptation, disaster risk reduction, and reconstruction after extreme events”. It is not associated with a conference.

This research has been supported by the Bundesministerium für Bildung und Forschung (grant no. 01LR2102I).

This paper was edited by Marvin Ravan and reviewed by two anonymous referees.

Adams, R., Binder, W., Breit, W., Disse, M., Fröhlich, K.-D., Jüpner, R., Kathmann, M., Kron, W., Lesny, K., Müller, U., Patt, H., Piroth, K., Pohl, R., and Weiß, G.: Hochwasser-Handbuch, 3, Springer Vieweg, 729 pp., https://doi.org/10.1007/978-3-658-26743-8, 2020.

Andrasko, I.: Why People (Do Not) Adopt the Private Precautionary and Mitigation Measures: A Review of the Issue from the Perspective of Recent Flood Risk Research, Water, 13, 140, https://doi.org/10.3390/w13020140, 2021.

Arrow, K., Solow, R., Portney, P. R., Leamer, E. E., Radner, R., and Schuman, H.: Report of the NOAA panel on contingent valuation, United States, National Oceanic and Atmospheric Administration, 1995.

Attems, M.-S., Thaler, T., Genovese, E., and Fuchs, S.: Implementation of property-level flood risk adaptation (PLFRA) measures: Choices and decisions, WIREs Water, 7, e1404, https://doi.org/10.1002/wat2.1404, 2020.

Berghäuser, L., Schoppa, L., Ulrich, J., Dillenardt, L., Jurado, O. E., Passow, C., Samprogna Mohor, G., Seleem, O., Petrow, T., and Thieken, A. H.: Starkregen in Berlin, Universitätsverlag Potsdam, https://doi.org/10.25932/PUBLISHUP-50056, 2021.

Bird, D., King, D., Haynes, K., Box, P., Okada, T., and Nairn, K.: Impact of the 2010–11 floods and the factors that inhibit and enable household adaptation strategies, NCCARF Publication 07/13, ISBN 978-1-921609-77-0, https://nccarf.edu.au/wp-content/uploads/2019/03/Bird_2013_Floods_household_adaptation_strategies.pdf (last access: 22 August 2025), 2013

Bruijn, K. D., Klijn, F., Ölfert, A., Penning-Rowsell, E., Simm, J., and Wallis, M.: Flood risk assessment and flood risk management, FloodSite Report T29-09-01, FLOODsite, ISBN 978 90 814067 1 0, 2009.

Bubeck, P., Botzen, W. J. W., and Aerts, J. C. J. H.: A review of risk perceptions and other factors that influence flood mitigation behavior, Risk Anal., 32, 1481–1495, https://doi.org/10.1111/j.1539-6924.2011.01783.x, 2012.

Bubeck, P., Botzen, W. J. W., Kreibich, H., and Aerts, J. C. J. H.: Detailed insights into the influence of flood-coping appraisals on mitigation behaviour, Global Environ. Chang., 23, 1327–1338, https://doi.org/10.1016/j.gloenvcha.2013.05.009, 2013.

Bubeck, P., Wouter Botzen, W. J., Laudan, J., Aerts, J. C. J. H., and Thieken, A. H.: Insights into Flood-Coping Appraisals of Protection Motivation Theory: Empirical Evidence from Germany and France, Risk Anal., 38, 1239–1257, https://doi.org/10.1111/risa.12938, 2018.

Bubeck, P., Berghäuser, L., Hudson, P., and Thieken, A. H.: Using Panel Data to Understand the Dynamics of Human Behavior in Response to Flooding, Risk Anal., 40, 2340–2359, https://doi.org/10.1111/risa.13548, 2020.

Caldas-Alvarez, A., Augenstein, M., Ayzel, G., Barfus, K., Cherian, R., Dillenardt, L., Fauer, F., Feldmann, H., Heistermann, M., Karwat, A., Kaspar, F., Kreibich, H., Lucio-Eceiza, E. E., Meredith, E. P., Mohr, S., Niermann, D., Pfahl, S., Ruff, F., Rust, H. W., Schoppa, L., Schwitalla, T., Steidl, S., Thieken, A. H., Tradowsky, J. S., Wulfmeyer, V., and Quaas, J.: Meteorological, impact and climate perspectives of the 29 June 2017 heavy precipitation event in the Berlin metropolitan area, Nat. Hazards Earth Syst. Sci., 22, 3701–3724, https://doi.org/10.5194/nhess-22-3701-2022, 2022.

DEFRA: Developing the evidence base for flood resistance and resilience: Summary Report, Environment Agency and DEFRA, London, UK, 2008.

DeStatis: Ergebnisse des Zensus am 9. Mai 2011, Statistische Ämter des Bundes und der Länder, 2014.

DeStatis: Bau- und Immobilienpreise – Tabellen, DeStatis, 2023a.

DeStatis: Verbraucherpreisindex für Deutschland – Lange Reihen ab 1948 – Dezember 2022, DeStatis, 2023b.

Dillenardt, L., Hudson, P., and Thieken, A. H.: Urban pluvial flood adaptation: Results of a household survey across four German municipalities, J. Flood Risk Manag., 15, e12748, https://doi.org/10.1111/jfr3.12748, 2022.

Dillenardt, L., Bubeck, P., Hudson, P., Wutzler, B., and Thieken, A. H.: Property-level adaptation to pluvial flooding: An analysis of individual behaviour and risk communication material, Mitig. Adapt. Strat. Gl., 29, 53, https://doi.org/10.1007/s11027-024-10148-y, 2024.

DWD: Die Entwicklung von Starkniederschlägen in Deutschland – Plädoyer für eine differenzierte Betrachtung, DWD, 7 pp., 2016.

EC (European Commission): Directive 2007/60/EC of the European Parliament and of the Council of 23 October 2007 on the assessment and management of flood risks, Official Journal of the European Union, L 288/27, https://eur-lex.europa.eu/eli/dir/2007/60/oj/eng (last access: 8 September 2025), 2007.

EEA: Economic losses from weather- and climate-related extremes in Europe, European Environment Agency, https://www.eea.europa.eu/en/analysis/indicators/economic-losses-from-climate-related (last access: 22 August 2025), 2024.

Erdlenbruch, K. and Bonté, B.: Simulating the dynamics of individual adaptation to floods, Environ. Sci. Policy, 84, 134–148, 2018.

Fuchs, S., Karagiorgos, K., Kitikidou, K., Maris, F., Paparrizos, S., and Thaler, T.: Flood risk perception and adaptation capacity: a contribution to the socio-hydrology debate, Hydrol. Earth Syst. Sci., 21, 3183–3198, https://doi.org/10.5194/hess-21-3183-2017, 2017.

GDV: Naturgefahrenreport 2022 – Die Schaden-Chronik der deutschen Versicherer, Gesamtverband der Deutschen Versicherungswirtschaft e.V., 2022.

GDV: Naturgefahrenreport 2023 – Die Schaden-Chronik der deutschen Versicherer, Gesamtverband deutscher Versicherer e.V., 2023.

GFZ: Hochwasserschadensdatenbank HOWAS21, Helmholtz-Zentrum Potsdam – Deutsches GeoForschungsZentrum GFZ, https://howas21.gfz.de/, 9 September 2025.

Gilligan, C., Kypri, K., and Bourke, J.: Social Networking Versus Facebook Advertising to Recruit Survey Respondents: A Quasi-Experimental Study, JMIR Res. Protoc., 3, e48, https://doi.org/10.2196/resprot.3317, 2014.

Grothmann, T. and Reusswig, F.: People at Risk of Flooding: Why Some Residents Take Precautionary Action While Others Do Not, Nat. Hazards, 38, 101–120, https://doi.org/10.1007/s11069-005-8604-6, 2006.

Grounds, M., Leclerc, J., and Joslyn, S.: Expressing Flood Likelihood: Return Period versus Probability, Weather Clim. Soc., 10, 5–17, 2018.

Houston, D., Werritty, A., Ball, T., and Black, A.: Environmental vulnerability and resilience: Social differentiation in short- and long-term flood impacts, T. I. Brit. Geog. 46, 102–119, https://doi.org/10.1111/tran.12408, 2021.

Hudson, P., Botzen, W. J. W., Kreibich, H., Bubeck, P., and Aerts, J. C. J. H.: Evaluating the effectiveness of flood damage mitigation measures by the application of propensity score matching, Nat. Hazards Earth Syst. Sci., 14, 1731–1747, https://doi.org/10.5194/nhess-14-1731-2014, 2014.

Hunt, J.: Inland and coastal flooding: developments in prediction and prevention, Phil. Trans. R. Soc. A, 363, 1475–1491, https://doi.org/10.1098/rsta.2005.1580, 2005.

Kaiser, M. H. E.: Data-driven modeling of areas prone to heavy rain-induced floods, PhD thesis, TU München, https://mediatum.ub.tum.de/doc/1600892/1600892.pdf (last access: 14 August 2025), 2021.

Kapp, J. M., Peters, C., and Oliver, D. P.: Research Recruitment Using Facebook Advertising: Big Potential, Big Challenges, J. Cancer Educ., 28, 134–137, https://doi.org/10.1007/s13187-012-0443-z, 2013.

Knocke, E. T. and Kolivras, K. N.: Flash Flood Awareness in Southwest Virginia, Risk Anal., 27, 155–169, https://doi.org/10.1111/j.1539-6924.2006.00866.x, 2007.

Köhler, L., Masson, T., Köhler, S., and Kuhlicke, C.: Better prepared but less resilient: the paradoxical impact of frequent flood experience on adaptive behavior and resilience, Nat. Hazards Earth Syst. Sci., 23, 2787–2806, https://doi.org/10.5194/nhess-23-2787-2023, 2023.

Kreibich, H., Thieken, A. H., Petrow, Th., Müller, M., and Merz, B.: Flood loss reduction of private households due to building precautionary measures – lessons learned from the Elbe flood in August 2002, Nat. Hazards Earth Syst. Sci., 5, 117–126, https://doi.org/10.5194/nhess-5-117-2005, 2005.

Kreibich, H., Christenberger, S., and Schwarze, R.: Economic motivation of households to undertake private precautionary measures against floods, Nat. Hazards Earth Syst. Sci., 11, 309–321, https://doi.org/10.5194/nhess-11-309-2011, 2011.

Kreienkamp, F., Philip, S. Y., Tradowsky, J. S., Kew, S. F., Lorenz, P., Arrighi, J., Belleflamme, A., Bettmann, T., Caluwaerts, S., Chan, S. C., Ciavarella, A., Cruz, L. D., Vries, H. D., Demuth, N., Ferrone, A., Fischer, E. M., Fowler, H. J., Goergen, K., Heinrich, D., Henrichs, Y., Lenderink, G., Kaspar, F., Nilson, E., Otto, F. E. L., Ragone, F., Seneviratne, S. I., Singh, R. K., Skålevåg, A., Termonia, P., Thalheimer, L., Aalst, M. V., Bergh, J. V. D., Vyver, H. V. D., Vannitsem, S., Oldenborgh, G. T. J. V., Schaeybroeck, B. V., Vautard, R., Vonk, D., and Wanders, N.: Rapid attribution of heavy rainfall events leading to the severe flooding in Western Europe during July 2021, World Weather Attribution, http://hdl.handle.net/2128/30381 (last access: 8 September 2025), 2021.

Lamond, J., Rose, C., Bhattacharya-Mis, N., and Joseph, R.: Evidence review for property flood resilience phase 2 report, Flood Re and UWE Bristol, https://uwe-repository.worktribe.com/output/874824 (last access: 22 August 2025), 2018.

Laudan, J., Rözer, V., Sieg, T., Vogel, K., and Thieken, A. H.: Damage assessment in Braunsbach 2016: data collection and analysis for an improved understanding of damaging processes during flash floods, Nat. Hazards Earth Syst. Sci., 17, 2163–2179, https://doi.org/10.5194/nhess-17-2163-2017, 2017.

Laudan, J., Zöller, G., and Thieken, A. H.: Flash floods versus river floods – a comparison of psychological impacts and implications for precautionary behaviour, Nat. Hazards Earth Syst. Sci., 20, 999–1023, https://doi.org/10.5194/nhess-20-999-2020, 2020.

Lindell, M. K. and Perry, R. W.: The Protective Action Decision Model: Theoretical Modifications and Additional Evidence, Risk Anal., 32, 616–632, https://doi.org/10.1111/j.1539-6924.2011.01647.x, 2012.

Maidl, E. and Buchecker, M.: Raising risk preparedness by flood risk communication, Nat. Hazards Earth Syst. Sci., 15, 1577–1595, https://doi.org/10.5194/nhess-15-1577-2015, 2015.

Müller, U.: 10 Jahre Hochwasserrisikomanagement in Sachsen. Dresdner Wasserbauliche Mitteilungen 48, Technische Universität Dresden, Institut für Wasserbau und technische Hydromechanik, https://hdl.handle.net/20.500.11970/103482 (last access: 22 August 2025), 2013.

Netzel, L. M., Heldt, S., Engler, S., and Denecke, M.: The importance of public risk perception for the effective management of pluvial floods in urban areas: A case study from Germany, J. Flood Risk Manag., 14, e12688, https://doi.org/10.1111/jfr3.12688, 2021.

Piper, D., Kunz, M., Ehmele, F., Mohr, S., Mühr, B., Kron, A., and Daniell, J.: Exceptional sequence of severe thunderstorms and related flash floods in May and June 2016 in Germany – Part 1: Meteorological background, Nat. Hazards Earth Syst. Sci., 16, 2835–2850, https://doi.org/10.5194/nhess-16-2835-2016, 2016.

Poussin, J. K., Botzen, W. J. W., and Aerts, J. C. J. H.: Factors of Influence on flood damage mitigation behavior by households, Environ. Sci. Policy, 40, 69–77, https://doi.org/10.1016/j.envsci.2014.01.013, 2014.

Poussin, J. K., Botzen, W. J. W., and Aerts, J. C. J. H.: Effectiveness of flood damage mitigation measures: Empirical evidence from French flood disasters, Global Environ. Chang., 31, 74–84, https://doi.org/10.1016/j.gloenvcha.2014.12.007, 2015.

Prentice-Dunn, S. and ROGERS, R. W.: Protection Motivation Theory and preventive health: Beyond the Health Belief Model, Health Educ. Res., 1, 153–161, https://doi.org/10.1093/her/1.3.153, 1986.

Rogers, R. W.: A Protection Motivation Theory of Fear Appeals and Attitude Change, J. Psychol., 91, 93–114, https://doi.org/10.1080/00223980.1975.9915803, 1975.

Rogers, R. W.: Cognitive and Physiological Processes in Fear Appeals and Attitude Change: A Revised Theory of Protection Motivation, in: Social Psychophysiology: A Sourcebook, edited by: Cacioppo, J. T. and Petty, R. E., Guilford Press, New York, 153–176, 1983.

Shaver, L. G., Khawer, A., Yi, Y., Aubrey-Bassler, K., Etchegary, H., Roebothan, B., Asghari, S., and Wang, P. P.: Using Facebook Advertising to Recruit Representative Samples: Feasibility Assessment of a Cross-Sectional Survey, J. Med. Internet Res., 21, e14021, https://doi.org/10.2196/14021, 2019.

Spekkers, M., Rözer, V., Thieken, A., ten Veldhuis, M.-C., and Kreibich, H.: A comparative survey of the impacts of extreme rainfall in two international case studies, Nat. Hazards Earth Syst. Sci., 17, 1337–1355, https://doi.org/10.5194/nhess-17-1337-2017, 2017.

Sweeney, T. L.: Modernized Areal Flash Flood Guidance, NOAA Technical Memorandum NWS HYDRO 44, Office of Hydology Silver Spring, Mf, 1992.

Terpstra, T.: Emotions, trust, and perceived risk: affective and cognitive routes to flood preparedness behaviour, Risk Anal., 31, 1658–1675, https://doi.org/10.1111/j.1539-6924.2011.01616.x, 2011.

Thieken, A. H., Petrow, T., Kreibich, H., and Merz, B.: Insurability and Mitigation of Flood Losses in Private Households in Germany, Risk Anal., 26, 383–395, 2006.

Thieken, A. H., Kreibich, H., Müller, M., and Lamond, J. E.: Data collection for a better understanding of what causes flood damage–experiences with telephone surveys, in: Flood damage survey and assessment: new insights from research and practice, edited by: Molinari, D., Menoni, S., and Ballio, F., Wiley, 95–106, ISBN 978-1-119-21792-3, 2017.

Thieken, A. H., Samprogna Mohor, G., Kreibich, H., and Müller, M.: Compound inland flood events: different pathways, different impacts and different coping options, Nat. Hazards Earth Syst. Sci., 22, 165–185, https://doi.org/10.5194/nhess-22-165-2022, 2022.

Thieken, A. H., Bubeck, P., Heidenreich, A., von Keyserlingk, J., Dillenardt, L., and Otto, A.: Performance of the flood warning system in Germany in July 2021 – insights from affected residents, Nat. Hazards Earth Syst. Sci., 23, 973–990, https://doi.org/10.5194/nhess-23-973-2023, 2023.

WHG: Wasserhaushaltsgesetz vom 31. Juli 2009, BGBl. I S. 2585, 2009.

Wind, H. G., Nierop, T. M., Blois, C. J. D., and Kok, J. L. D.: Analysis of flood damages from the 1993 and 1995 Meuse floods, Water Resour. Res., 35, 3459–3465, https://doi.org/10.1029/1999WR900192, 1999.