the Creative Commons Attribution 4.0 License.

the Creative Commons Attribution 4.0 License.

| 03 Nov 2025

| 03 Nov 2025

Assessing effects of nature-based and other municipal adaptation measures on insured heavy rain damages

Thijs Endendijk

Jeroen C. J. H. Aerts

W. J. Wouter Botzen

Peter J. Robinson

Intense short duration rainfall events are expected to increase in severity and frequency due to climate change. Densely populated urban areas are vulnerable to these events, resulting in high losses. Implementing nature-based (e.g. green streets, rain gardens and green roofs) and other municipal adaptation measures (e.g. water storage facilities) can be a way to mitigate these damages. Little is known about the effectiveness of these measures combined in a municipality. This study assesses municipal climate adaptation measures being taken by the municipality of Amsterdam. Unique claims data of almost all Dutch insurers is used to understand the impact of these climate adaptation interventions. We study one neighborhood in Amsterdam which has been renovated using climate adaptation measures, including nature-based solutions. We implement a quasi-experimental difference-in-Differences (DiD) analysis that compares insured rainfall damages in the area to a similar neighboring area that was not renovated with climate adaptation measures. We find a negative significant relation between climate adaptation measures and insured damage when comparing the area where measures were taken to the similar area were measures were not taken, i.e. damage is reduced by climate adaptation measures by EUR 1375–5648 per rain day in the treatment area. Furthermore, precipitation per day is positively and significantly associated with insured damage. We suggest that nature-based and other adaptation measures can be installed by local governments and stimulated by insurers and banks to increase climate resilience in urban areas.

- Article

(675 KB) - Full-text XML

- BibTeX

- EndNote

Densely built cities are vulnerable to intense short duration rainfall events, i.e. cloudbursts (Rosenzweig et al., 2019), which can result in pluvial flooding and high damage to buildings and infrastructure. For example, on the 2 July 2011 in Copenhagen a single cloudburst of extreme precipitation caused over EUR 800 million of damage (The City of Copenhagen, 2012). The rainfall event in Southern Germany in June 2024 reached EUR 2 billion–3 billion of insured losses (MOODY's, 2024). Due to climate change, cloudbursts are likely to increase in frequency and severity (Seneviratne et al., 2021).

A wide range of resilience and additional flood adaptation measures are needed to cope with cloudbursts (Rosenzweig et al., 2018; Busker et al., 2022). Pluvial flood resilience in urban areas is often created by Flood Damage Mitigation (FDM) measures (e.g. water storage, drainage systems, etc.) taken by the (local) government. Furthermore, governments play a key role in enhancing resilience to flood damage, for example by investing in structural protection measures, such as dikes (Filatova, 2014). The traditional approach is engineering through building drainage systems, levees and dams. According to Sörensen et al. (2016), additional strategies are needed to enhance flood resilience such as adopting “blue-green infrastructure”, like green roofs, rain gardens and porous pavements. These blue-green infrastructure can be used to retain (storm)water and therefore reduce flood risks (Sörensen and Emilsson, 2019).

There is also a role for households and businesses in flood damage risk reduction. For instance, they can implement emergency FDM measures (e.g. placing sandbags which act as a barrier to flood water and elevating personal possessions) and take structural FDM measures (e.g. making walls water-resistant and strengthening their buildings' foundation) (Endendijk et al., 2023). Moreover, insurance may be purchased to cover damages in cases where these measures fail. However, it has been shown that individuals, communities and businesses often underinvest in protection against low-probability, high-consequence flood events (Meyer and Kunreuther, 2017). Therefore, governments can undertake interventions to stimulate flood preparedness by households and businesses through awareness campaigns (Osberghaus and Hinrichs, 2021). Such awareness campaigns may focus on educating households about flood risk and potential coping strategies.

The goal of this study is to understand the impact of nature-based and other adaptation measures measures on insured damages caused by cloudbursts. The innovation of our study is threefold. Firstly, we examine the impact of municipal climate adaptation measures on insured damages empirically. A wide body of literature has assessed flood damage using mainly flood damage modelling methods (Merz et al., 2013; Spekkers et al., 2014; Van Ootegem et al., 2015). Traditional flood damage models focus on simulating flood depths of riverine flooding and estimating damage based on exposure information, such as building classes and their vulnerability (Merz et al., 2010; Sörensen and Mobini, 2017). However, multiple studies have shown that flood depth and building class information cannot fully explain flood damage, since it requires an extensive dataset which is often not available (Wagenaar et al., 2017; Merz et al., 2010). Moreover, few studies have studied pluvial flood risk modelling (Van Ootegem et al., 2015; Porter et al., 2023), which is the hazard focus of our study. Even fewer studies have investigated the effect of FDM measures on reducing damage caused by pluvial flooding (Löwe et al., 2017)1. Modelling studies focus on situations that are modelled, and therefore not observed in real life. Empirical studies, that include real damage observations, are needed to better understand the effectiveness of FDM measures. That is, empirical studies are more suitable for drawing conclusions from actual conditions, compared to conclusions derived from modelling studies that are typically based on assumed conditions.

The second novelty of this paper is that we use actual insurance damage data to identify causal effects of FDM measures. A small but expanding body of literature has focused on assessing the effectiveness of FDM measures on a household level using surveys as empirical methods (Endendijk et al., 2023; Kreibich et al., 2015; Poussin et al., 2015; Thieken et al., 2005). For example, Endendijk et al. (2023) found that household FDM measures reduced damage due to flooding by about 30 % for buildings and 40 % for home contents using survey data. Other studies show that FDM measures on a building level have substantial effects in limiting flood damage (Kreibich et al., 2015; Poussin et al., 2015; Thieken et al., 2005). In this research, we do not only focus on adaptation measures of individuals (e.g. green roofs), but also on spatial, neighbourhood level adaptation measures of the municipality. With survey data one can typically only identify correlational effects. In this study, we aim to identify causal effects with a quasi-experiment using real damage data from insurers. The Difference-in-Differences (DiD) method allows us to identify the causal effect of FDM measures (Angrist and Pischke, 2009). Also, in surveys it is possible that damages are misreported, whereas in this study we examine observed damages registered by insurance company professionals. The use of a DiD-method is an innovative addition to the existing literature on climate adaptation (Osberghaus and Hinrichs, 2021). In this study, we illustrate how a DiD-method can work in the climate adaptation field.

The third innovation of this study is that we assess the effectiveness of a broad range of policy interventions, including nature-based solutions. In the literature, most studies examine the effect of a single FDM measure or policy intervention in isolation (Osberghaus and Hinrichs, 2021; Sörensen and Emilsson, 2019). More comprehensive approaches may be needed for substantial flood risk reduction (Busker et al., 2022; Osberghaus and Hinrichs, 2021). Osberghaus and Hinrichs (2021) is, to the best of our knowledge, the only study that adopts a quasi-experimental design to assess the effectiveness of an FDM measure. They use a DiD-design to measure the impact of a large-scale flood risk awareness campaign from 2009 to 2017 on flood damage (as well as households' adaptation behaviour and insurance penetration) in Germany. They do not find a significant effect of the awareness campaign on flood damages. Another study on a single FDM measure is done by Sörensen and Emilsson (2019), who assessed the effectiveness of a stormwater system retrofitted through climate adaptation using insurance claims data. They find that long term trends show less flood damage in the area with these adaptation measures compared to similar neighborhoods. There are studies that focus on the impact of single measures like retrofitting an old stormwater system (Sörensen and Emilsson, 2019), blue-green roofs (Busker et al., 2022) or awareness campaigns (Osberghaus and Hinrichs, 2021). This paper studies a broader range of interventions such as awareness campaigns by adding climate adaptation measures to the study as well. In reality, a wide array of measures is needed to reduce damage resulting from cloudbursts (Busker et al., 2022). We lack understanding of the impact of a broad range of FDM measures on insured damages.

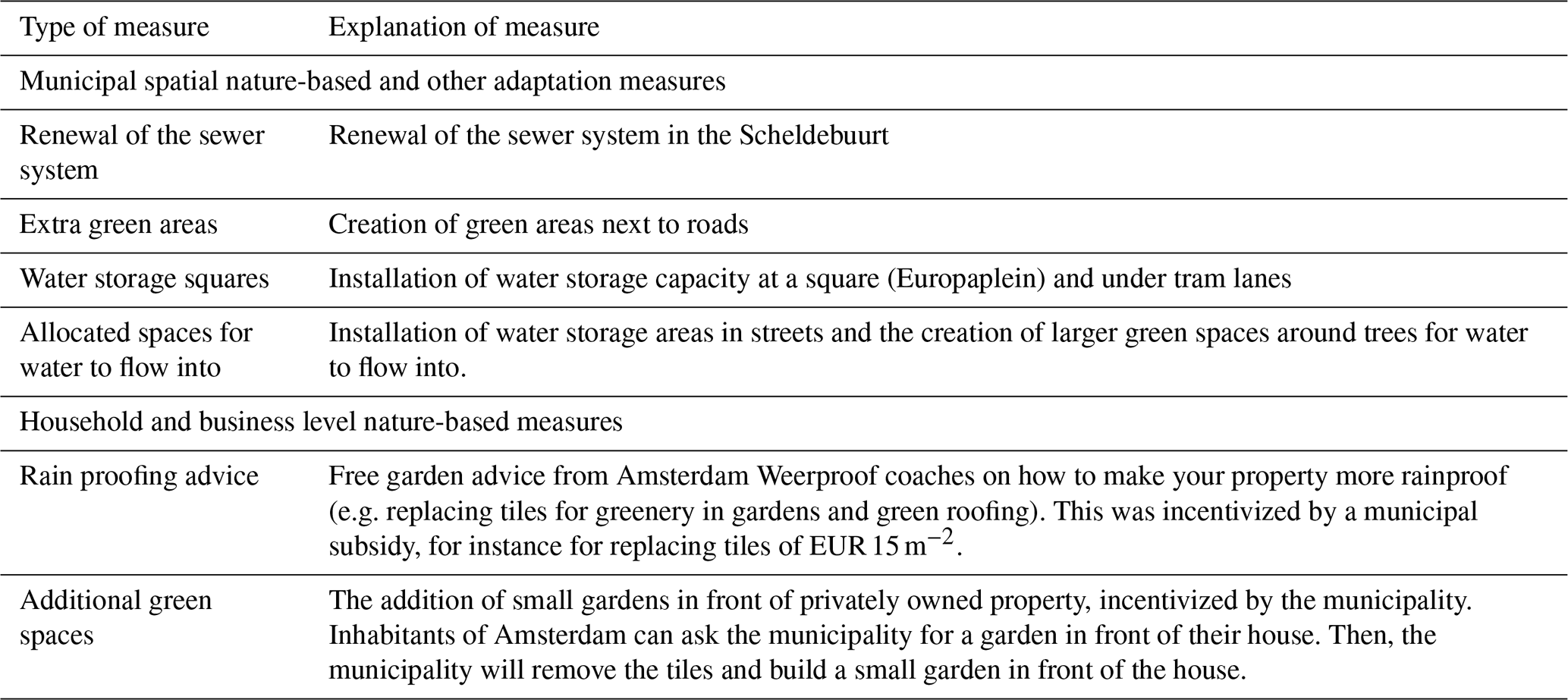

Table 1Adopted nature-based and other adaptation measures in the treatment area (Amsterdam Weerproof, 2025a).

The remainder of this paper is structured as follows. Section 2 gives an overview of the methodology. Section 3 gives the results that are discussed in Sect. 4. The conclusion follows in Sect. 5.

2.1 Case study description

In this study we use insurance claims data to understand the impact of municipal adaptation interventions on pluvial flood damages in Amsterdam. We focus on parts of the city where such interventions have been implemented over time. We use data on the timing of specific interventions provided by the program Amsterdam Weerproof (Amsterdam Weatherproof), which aims to make the city more climate resilient. In this program, various structural measures have been implemented, like retrofitting municipality owned buildings into greener properties, creating more green areas, improving water storage locations, and sewer renewal. Moreover, another focus of the organization is to provide extreme weather information to raise awareness of flood risk of citizens through online and in-person information provision (Amsterdam Weerproof, 2024b).

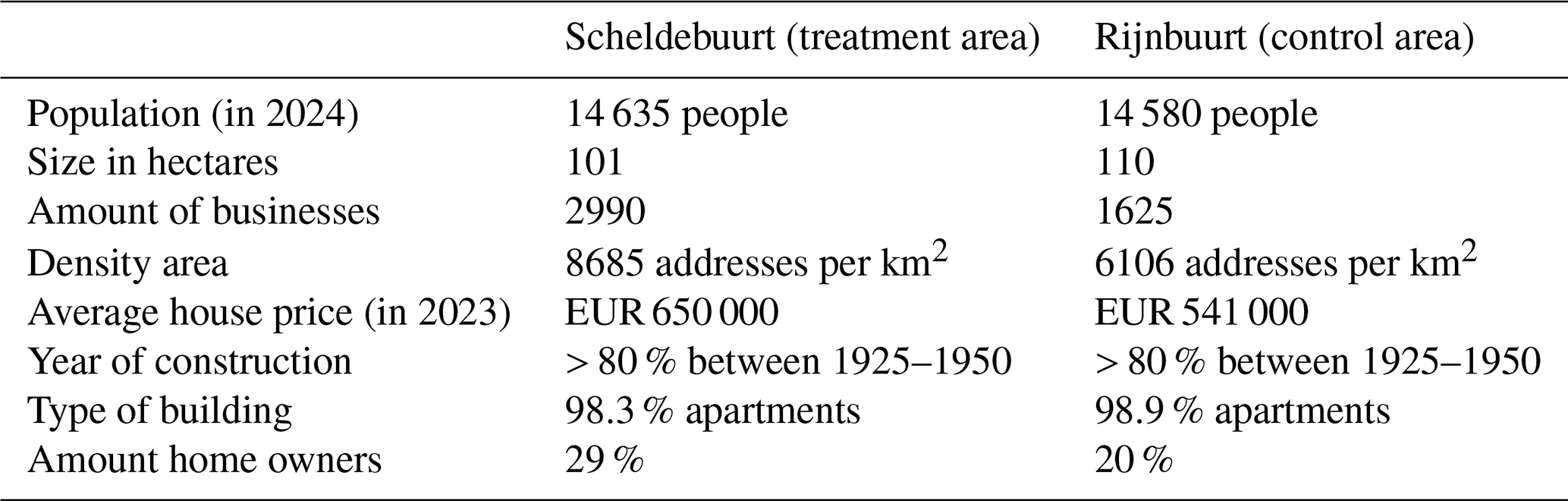

Amsterdam Weerproof executed projects in various neighbourhoods. We compare two adjacent areas of the neighbourhood Rivierenbuurt with different postal codes (PC). In PC 1078, Scheldebuurt (treatment area), municipal adaptation measures were executed from 2018 until 2022. We compare this neighborhood to PC 1079, Rijnbuurt (control area), where no measures were taken. Detailed descriptions of the Rivierenbuurt neighbourhood are found in Appendix A. Table 1 describes the climate adaptation measures that were taken in the Scheldebuurt.

2.2 Data

2.2.1 Pluvial flood insurance claims data and nature-based and other adaptation measures

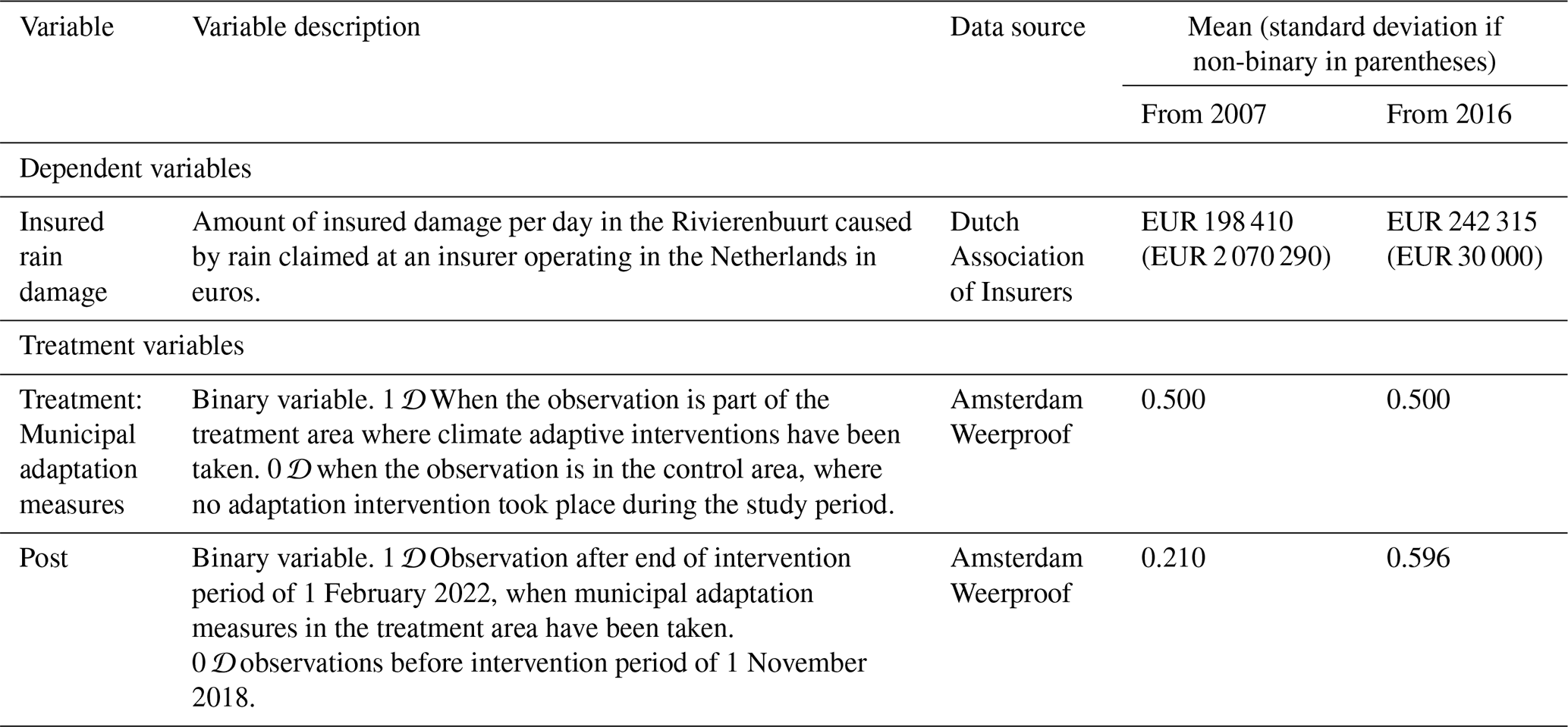

For this study we use claims data of rain damage of households from the Dutch Association of Insurers. The Dutch Association of Insurers registers claims of households filed by insurance companies that are members of the association. Since rain damage is covered by default in property and contents insurance products (Dutch Association of Insurers, 2024), we expect that the vast majority of the claims are accepted. More than 95 % of the Dutch insurers market is member of the Dutch Association of Insurers (Dutch Association of Insurers, 2025a). Furthermore, more than 95 % of households with a contents and/or property insurance in the Netherlands are insured against rain damage (Dutch Association of Insurers, 2025b). Therefore, almost all pluvial flood damages of households in the studied neighbourhoods are reflected in the insurance claims. We use aggregated data on postcode 4-level (PC 4)2 for the municipality of Amsterdam (2007–2024). In the Netherlands, PC 4 refers to a neighbourhood or a part of a district within a municipality. The damage data ranges from 1 January 2007 until 15 March 2024. The rain damage claims consist of time (day), amount (damage in euros) and location (at PC 4-level).

The treatment variable is the observed time from when nature-based and other adaptation measures were implemented. From 1 November 2018 onwards the municipality of Amsterdam implemented nature-based and other climate adaptation measures to reduce damage in the treatment area with PC 1078 (Amsterdam Weerproof, 2025a).

Both models we use showcase the analysis without the intervention period, to make for a cleaner analysis of the comparison before and after the implementation of the measures3. This choice has been made to avoid potential bias from including the rollout period, when the policy's effect was only partial.

2.2.2 Rain data and socio-demographic characteristics

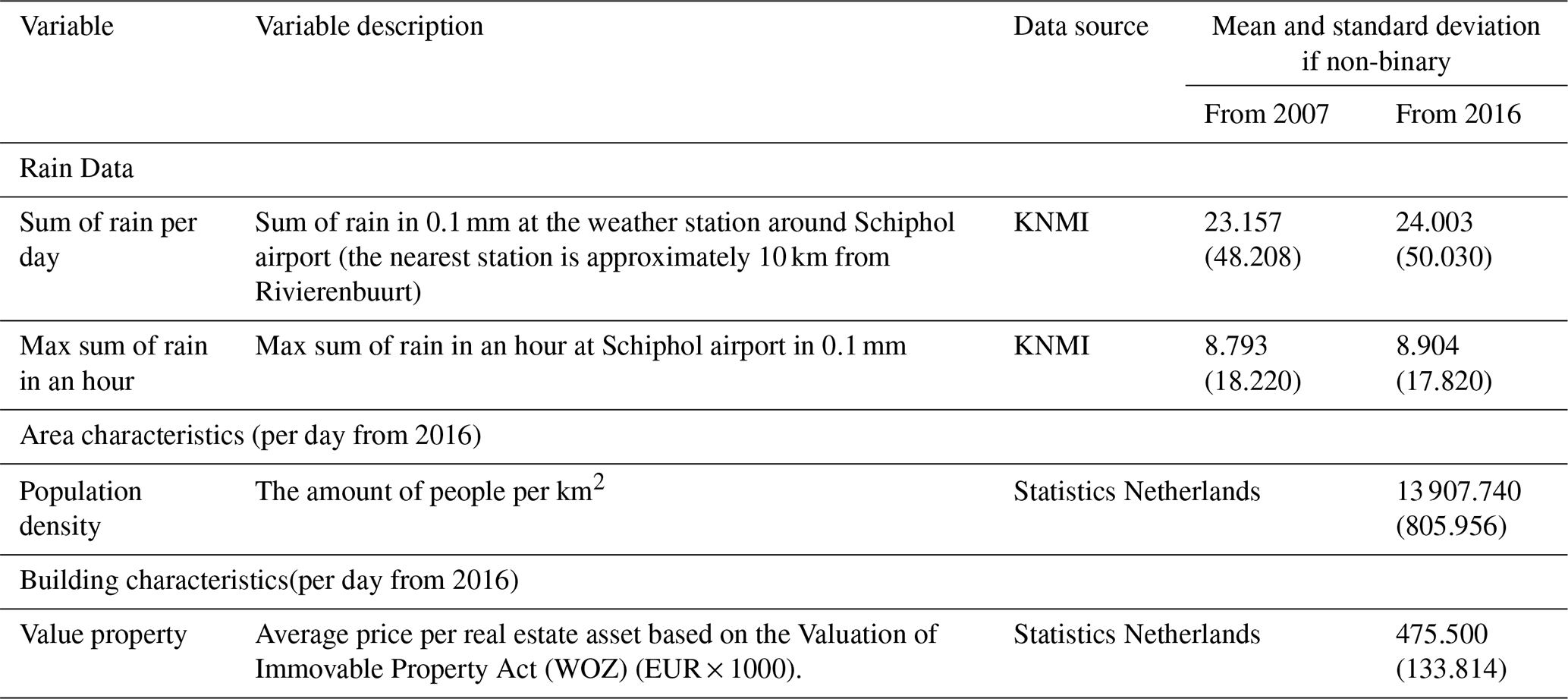

Control variables are added to check for neighborhood specific effects when establishing the relationship between the adaptation measures and the amount of damage. Two categories of variables are controlled for. Precipitation data is added on PC4 level over the period damage data is available from 1 January 2007 until the 15 March 2024. The nearest weather station of the Royal Netherlands Meteorological Institute (KNMI) is located at Schiphol airport, which is approximately 10 km from the Rivierenbuurt. Two types of data are derived from the weather station: data on amount of precipitation per day and data on maximum precipitation per hour. Both are included, because moderate rain over a long period within a day can cause damage as well as torrential rain in a short moment. The observations of the damage data are on the day on which the claim is filed. The claim can be filed on the same day as the event that caused the damage. However, people can also file claims one or two days later. Therefore, for both rain control variables we use 1 and 2 d lags.

Additionally, data on socio-demographic characteristics of the Rivierenbuurt (e.g. average house price and average size of households) is used to control for neighborhood specific effects. This data is derived from public data of Statistics Netherlands (CBS), which is only available on a yearly basis from 1 January 2016 until 31 December 2023. Therefore, we interpolate between the years to create daily neighborhood characteristic data and extrapolate in the period 1 January 2024 until 15 March 2024 by assuming linear trends. In Appendix E we show tables on the distribution of insured rain damage, a detailed description of insured rain damage data and the distribution of rain data.

2.3 Difference-in-difference method

In this study, we use a DiD two-way fixed effects model to estimate the impact of municipal adaptation measures on rainfall damage in Amsterdam. This method compares a situation before and after an intervention period. We compare two adjacent areas within the Rivierenbuurt neighborhood: one where FDM measures have been implemented (Scheldebuurt) and another where no adaptation interventions have been implemented (Rijnbuurt). The DiD-approach allows us to compare changes in outcomes over time between these areas, while controlling for unobserved factors and broader trends (Card and Krueger, 2000; Wooldridge, 2014). By leveraging insurance claims data, we can isolate the causal impact of these measures under the assumption that both areas would have followed similar trends in the absence of interventions. We test this assumption in the next section.

We expand upon a traditional DiD by employing a two-way fixed effects (TWFE-) model (Callaway and Sant'Anna, 2021). Using fixed effects in a DiD gives a more robust causal estimate. This approach controls for time-invariant unobserved differences between neighborhoods, such as historical infrastructure and socioeconomic factors, as well as time-specific shocks, like extreme weather events. By accounting for both unit (neighborhood) and time (month) fixed effects, the TWFE-model ensures that our estimated treatment effect reflects the impact of adaptation measures rather than underlying trends or external influences. This strengthens the causal interpretation of the DiD-analysis. We estimate the following TWFE-model:

The outcome variable Yit represents daily insured damage claims in euros. Moreover, we expect that no rain damage occurs with slight rain (< 2 mm h−1). Therefore, we look at cases of moderate, or higher rain (> 2 mm h−1) in classification (Met Office, 2012). Excess rainfall can accumulate on the surface and may cause damage to buildings. Therefore, we only include damage observations linked to days when this threshold is exceeded, along with a two-day lag period to account for potential delays in damage claims reporting. The average treatment effect is given by β1, which captures the average impact of the policy interventions in the treated area in the TWFE specification (Callaway and Sant'Anna, 2021). We control for time-invariant neighborhood differences using unit (postcode 4-level) fixed effects (δi). Time-specific neighborhood-level shocks are controlled for through fixed effects for each month (θt). The coefficient vector of other control variables is represented by β2, and the error term is given by εit.

2.4 Common trend assumption

The central assumption for a DiD-analysis is the common trend assumption, which states that, in the absence of the treatment, the treatment and control groups would have followed a similar trend (in our case of insured damages) over time (Angrist and Pischke, 2009). This assumption allows for isolating the treatment effect from any other factors that may influence damage from rainfall. If both neighbourhoods were on different damage trajectories before the policy interventions, differences in their post-interventions outcomes could be attributed to these pre-treatment differences. Additionally, it is assumed that no significant changes in group composition occur over time. Data from Statistics Netherlands indicates that there were no shocks to the demographic composition of the neighbourhoods during the study period, supporting this assumption. Moreover, key demographics are controlled for in our regression model.

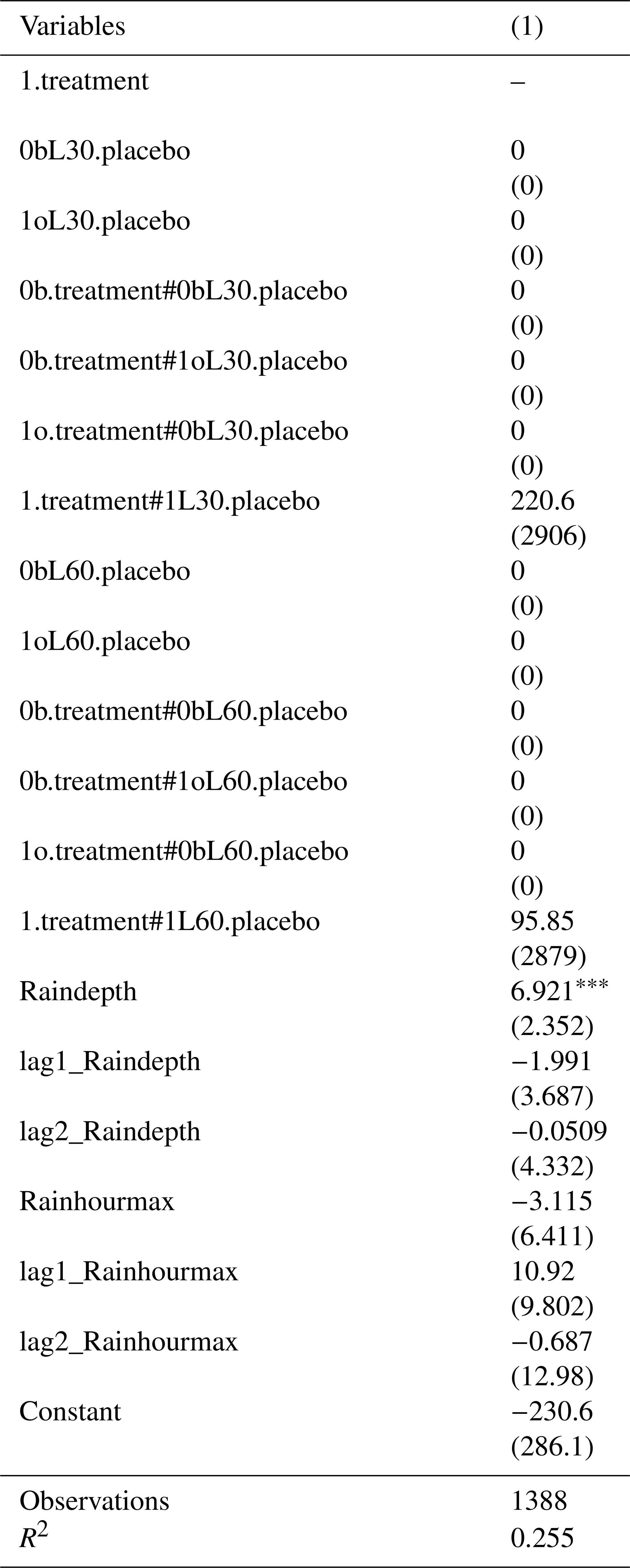

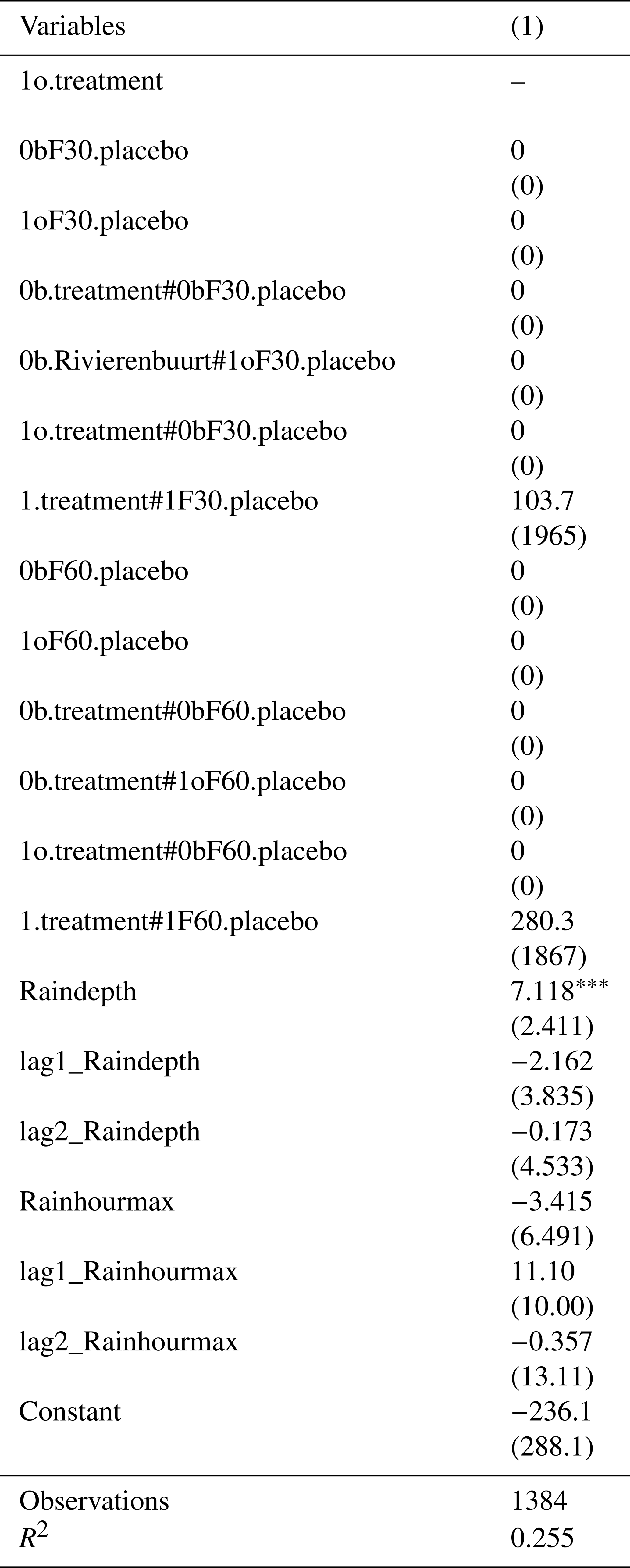

The placebo test can be performed to check for the common trend assumption (Eggers et al., 2024). The placebo test checks the common trend assumption by creating “fake” treatment groups before and after the interventions. We select a different treatment timeframe and observe whether the effects are significant as well. If no effect is found in any of the placebo groups, it supports that the found treatment effect can be attributed to the treatment rather than pre-existing trends. Angrist and Pischke (2009) used lag and lead values of treatment status to show that no significant effects occurred in the placebo periods. In Appendix B, we apply placebo tests by using 1 and 2 month leads and lags for the treatment variable. These placebo treatment variables resulted in non-significant outcomes, reinforcing the validity of the common trend assumption for causal inference.

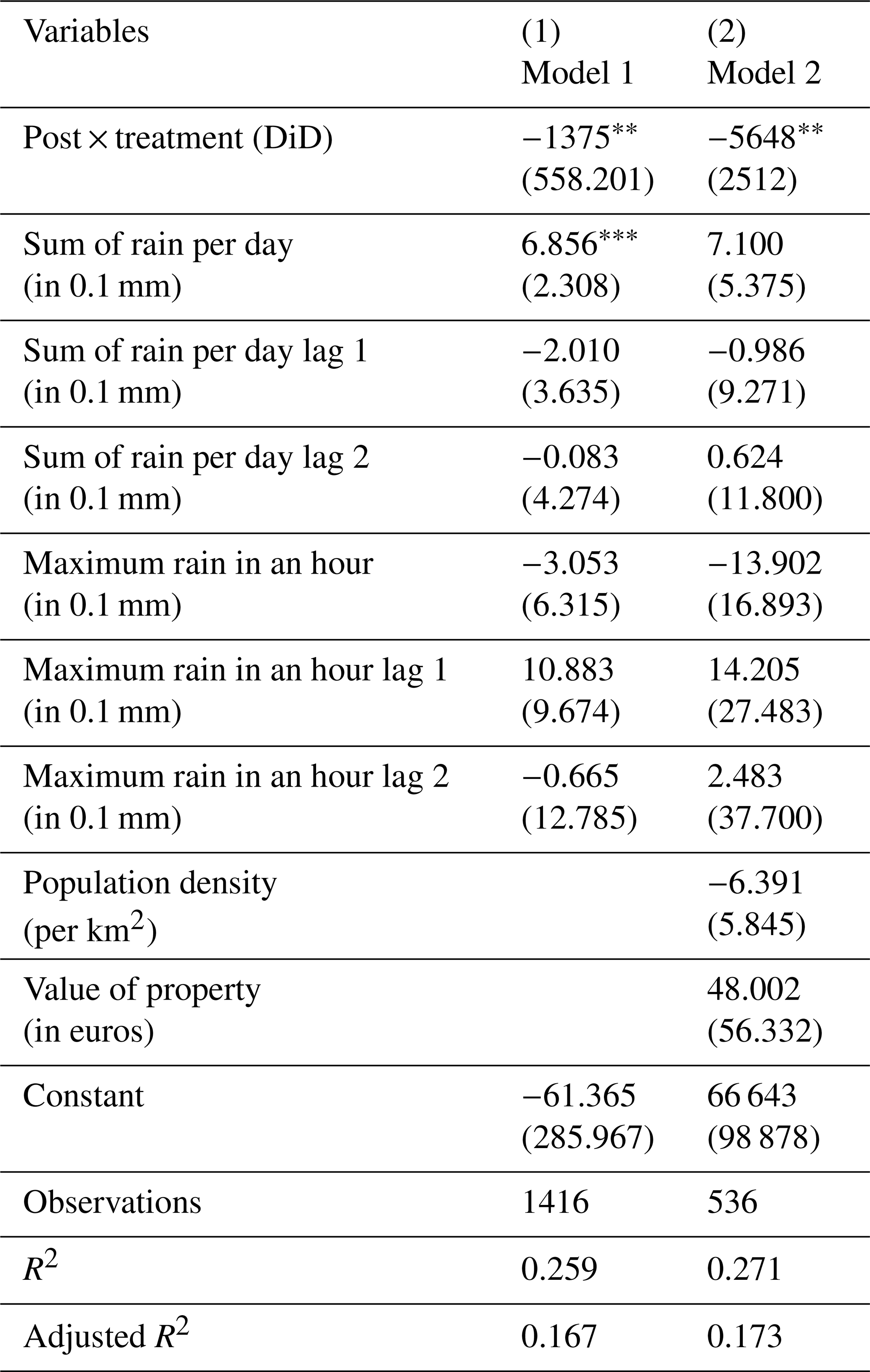

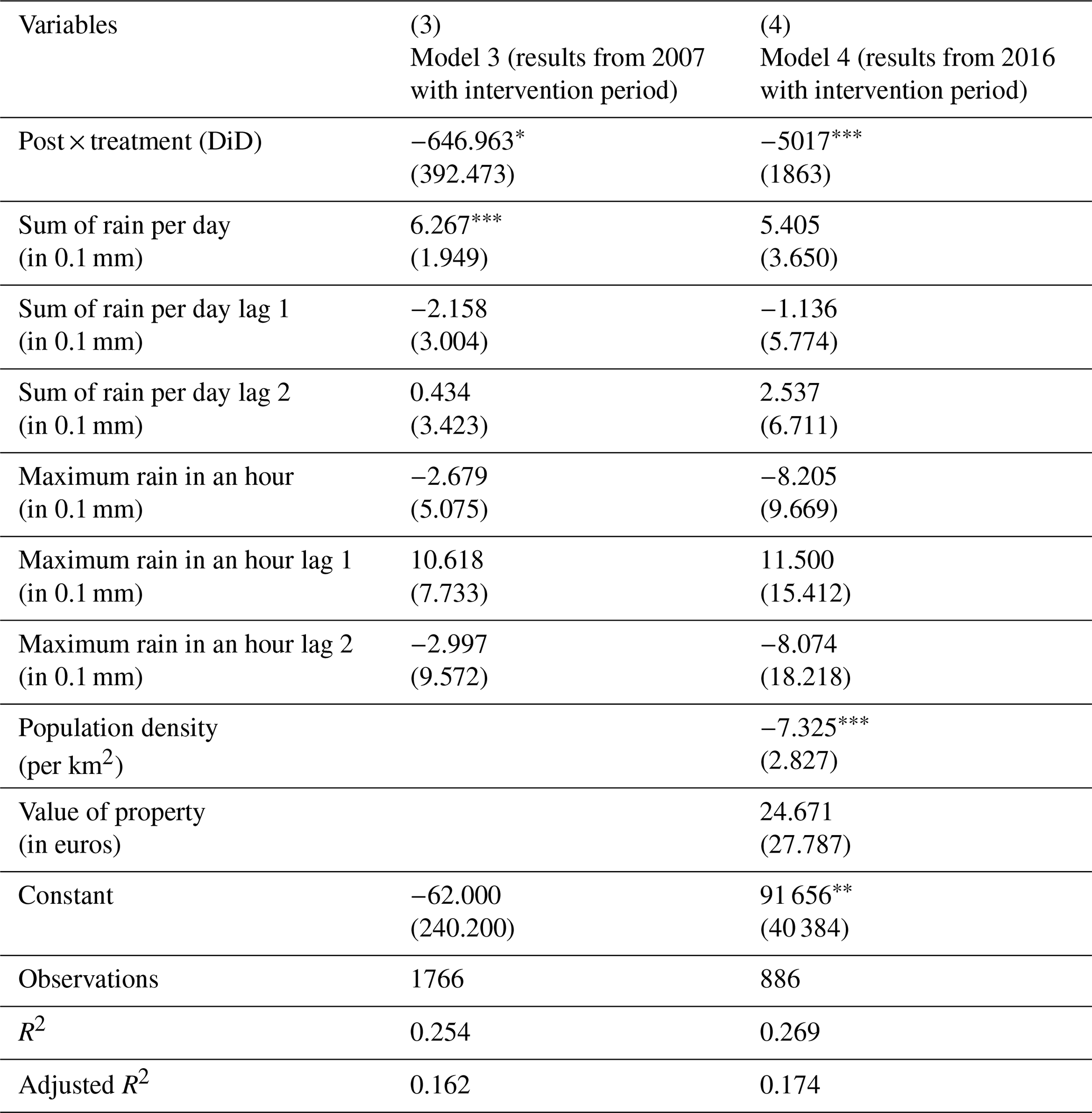

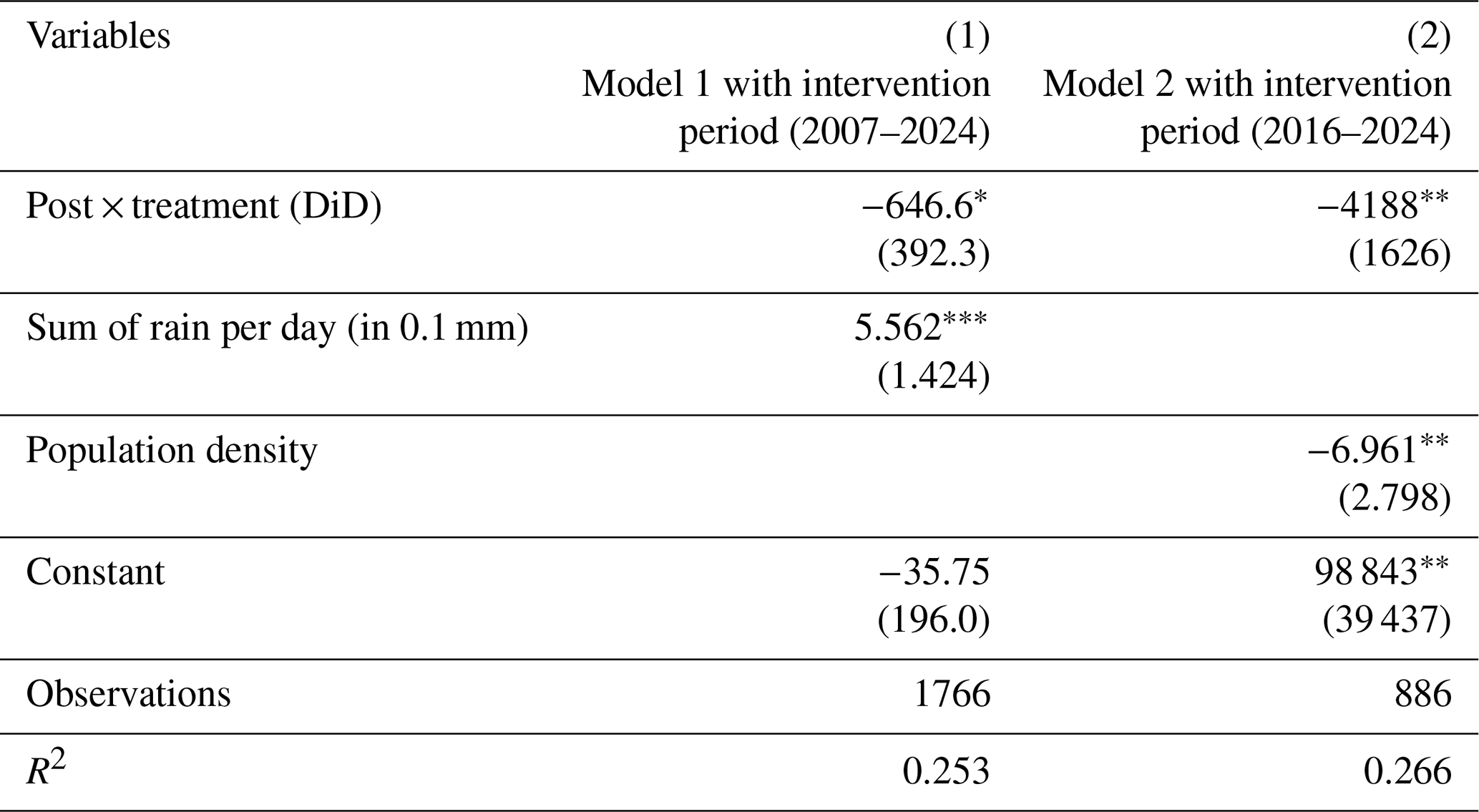

The results are shown in Table 4 for two models. The first model showcases the results of the dataset starting from 2007 until 2024 without control variables for area characteristics, which are unavailable for this entire time period. In this model we see that the DiD-indicator shows a significant (p < 0.05) reduction of insured damage in the treatment compared to the control group. This means that in the area where nature-based and other adaptation measures were adopted, insured damage in the treatment group is on average EUR 1375 d−1 lower for rain events exceeding 2 mm h−1 as compared to the control group, after controlling for time- and unit fixed effects. The second model presents results using damage data starting from 2016, when area characteristics are available as control variables. The coefficient on the interaction term shows a significant (p < 0.05) reduction of damage in the treatment group, compared to the control group. The rain damage is, on average, lower by EUR 5648 per rain day compared to the control group. For illustration, we can see a damage reduction of 21,7 % for rainy days with more than EUR 2500 of insured damage per year on average based on model 1 (from 2007).4

Furthermore, the variable for precipitation per day is positive and significant (p < 0.01) in model 1, indicating that an increase of 0.1 mm precipitation per day results in an increase of EUR 13.75 of rain damage on average per rain day based on model 1. Regarding the area- and building characteristics control variables, we see that none of the variables are significantly associated with insured damage. According to the adjusted R2, model 1 explains 16.7 % of the variation in insured damage and model 2 explains 17.3 % of the variation.

Table 2Dependent variable, treatment variables and their descriptive statistics over the final sample period (excluding the intervention period).

Table 3Control variables and their descriptive statistics over the final sample period (excluding the intervention period).

Table 4Two-way fixed effects DiD regression on insured damage per day in case of maximum rain per hour exceeds 2 mm h−1 from 2007 and 2016 without observations in the intervention period.

Standard errors in parentheses. p < 0.01, p < 0.05, ∗ p < 0.1

4.1 Discussion of findings in relation to the existing literature

Impact nature-based and other adaptation measures measures on rain damage (post × treatment): In both models we find a significant reduction of insured damages in the treatment group compared to the control group. The interaction result of model 1 is impacted by high damage observations in August 2010 in the control group compared to the treatment group.5 This also explains why the standard deviation is very high compared to the average of damage data (Table 2) and rain data (Table 3).The results of the impact of nature-based and other adaptation measures on damage are in line with some previous studies on physical adaptation measures. Sörensen and Emilsson (2019) present trends showing less damage in areas with adaptation measures compared to similar neighbourhoods. Also, the findings are in line with studies on the stated effectiveness of FDM measures: Endendijk et al. (2023), Kreibich et al. (2015), Poussin et al. (2015), and Thieken et al. (2005) all confirm the damage reductive capacity of flood risk reduction measures. The addition of this study is the DiD-design, which allows us to identify the causal effect of FDM measures. To our knowledge, the method is hardly seen in the climate adaptation field. We illustrate with this that this method can work. Future studies could adopt this method as well in different areas.

Rain control variables: Model 1 shows a significant result regarding precipitation per day. Contrastingly, the precipitation per day variable in model 2 is insignificant. Model 1 has 1416 observations and model 2 has 536 observations. The fact that model 2 has less than half the number of observations could be an explanation why no significant coefficient is found for the rain control variables in model 2. The literature findings on the relation between rain and damage vary. Previous literature on pluvial floods and damage show that flood depth (among other factors) cannot fully explain damage (Wagenaar et al., 2017; Merz et al., 2010). However, Sörensen and Mobini (2017) do find that rainfall intensity is one of the main determinants of flood damage. We further do not find a significant relation between damage and maximum rain per hour.

4.2 Policy implications

We find that nature-based and other adaptation measures reduce rain damage. Local governments can use nature based and other adaptation measures (e.g. through green lanes, water storage facilities, green roofs, and greener gardens) as means to decrease rain damage in urban areas and increase livability and biodiversity in these areas (Skrydstrup et al., 2022). These nature-based measures often come with co-benefits like mental and physical benefits (Tzoulas et al., 2007), which can have a long-term impact on health by incentivizing people to exercise, for instance. Rain damage is the focus of this study. The measures the municipality applied could also limit impacts of other natural hazards, like drought (Ljubojević et al., 2025) and heat (Augusto et al., 2020). In this way, nature-based measures can limit long-term impacts of climate change in the area (Augusto et al., 2020). The benefits (in addition to the damage reducing potential of these measures) make these nature-based solutions attractive for designing climate resilient cities globally. The measures the city of Amsterdam implemented (e.g. water storage on city squares, green roofs) can be implemented in cities worldwide. The findings of this study can motivate national governments, building corporations, and project developers to construct buildings and infrastructure in a climate adaptive way. The quantification of avoided damage can also be useful for cost-benefit analyses. Measures like green roofs and rain gardens can be stimulated by governments using policy measures like subsidies. Lastly, the results of this study can motivate insurers to stimulate the uptake of climate adaptive measures of their customers. Insurers could stimulate these measures by providing flood risk information or giving premium discounts when customers take climate adaptive measures and may benefit from lower claims (Poussin et al., 2015; Mol et al., 2020).

4.3 Limitations and research implications

In this study we use insurance damage data. Most studies using insurance data use data of a single insurer (Cheng et al., 2012) or only a few insurers (Sörensen and Mobini, 2017). A strength of this study is the use of high-resolution insurance data covering more than 95 % of the Dutch insurance market (Dutch Association of Insurers, 2024). However, the data contains only household claims, and we here neglect insurance claims of businesses and uninsured damages. It would be of value to analyze uninsured damages (e.g., public infrastructure) and claims of businesses as well. Insured damage of households is only a part of total damage of extreme rain, but can still give valuable insights into the effectiveness of FDM measures. The fact that only two full years (2022–2024) had passed since the end intervention period could be a limitation. However, we do find significant effects already. Moreover, torrential rain can be a local event, whereas we used rain data measured at the nearest weather station of which data may deviate from the real rainfall at the case study locations. This difference in data granularity between local insured damages and rainfall may weaken statistical significance between these two variables and means that the rainfall data may lack precision. Additionally, it would be insightful if future research could be conducted on social vulnerability (e.g. financial situation), since that could influence insurance uptake. Furthermore, this study shows the impact of all adaptation measures combined. Because of privacy regulations, it was not possible to localize claims on a more detailed level than PC 4-level. This makes it difficult to attach effects of a single measure to single damage claims. It would be valuable to understand how much separate measures contribute to damage reduction. This would give information on which measures policymakers could prioritize. In a future study, it might be of value to understand the impact of these measures separately.

In this study, we show the impact of various nature-based and other adaptation measures on insured rain damage. We add novel insights to the literature by using actual insurance damage data to identify causal effects of a broad range of adaptation measures. Our results show a robust significant reduction in damage caused by the adoption of climate adaptation measures in the city of Amsterdam. The effect of nature-based and other climate adaptation measures on rain damage suggests that governments, private investors, banks and insurers can stimulate and implement these measures to cope with increasing rain damage. Local governments can incentivize the uptake of these measures among their citizens through information provision and subsidization. Private investors can invest in climate adaptive real estate to finance durable, resilient real estate and infrastructure that can withstand heavy rain damage. Banks can stimulate climate adaptation by including adaptation measures for resilient houses in loans (e.g. climate adaptive mortgage products). Insurers can stimulate climate adaptation measures through information provision, premium discounts and climate adaptive retrofitting (building back better) after damage. Improving the understanding of the impact of climate adaptation measures is important to increase societal climate resilience. Cloudbursts can increase in severity and frequency, potentially causing more floods in urban areas. The implementation of nature-based and other adaptation measures is important to prevent urban floods and reduce damage in urban areas globally.

In Rivierenbuurt we compare two parts of the same neighbourhood. One where measures have been executed, Scheldebuurt, and one where no measures have been taken, Rijnbuurt.

Table A1Description Rivierenbuurt.

Source: Statistics Netherlands (2025).

The goal of this placebo test is to identify whether groups were experiencing similar trends before the treatment. This can be done by creating “fake” treatments that indicate treatment before it actually occurred (Angrist and Pischke, 2009). These placebo treatments should have no effect if the common trend assumption holds. If they do show significant effects, this suggests a violation of the assumption, as it indicates that treated and control groups were already on diverging paths prior to the interventions.

We apply placebo tests by using 1 and 2 month leads and lags for the treatment variable. The lead and lagged placebo treatments do not show any significant outcomes, which provides evidence in favour of the common trend assumption.

Table B1Placebo test 2007 with lags of one month and two months.

Table B2Placebo test 2007 with leads of one month and two months.

Standard errors in parentheses. p < 0.01, p < 0.05, ∗ p < 0.1

Table B3Placebo test 2016 with lags of one month and two months.

Standard errors in parentheses. p < 0.01, p < 0.05, ∗ p < 0.1

Table B4Placebo test 2016 with leads of one month and two months.

Standard errors in parentheses. p < 0.01, p < 0.05, ∗ p < 0.1

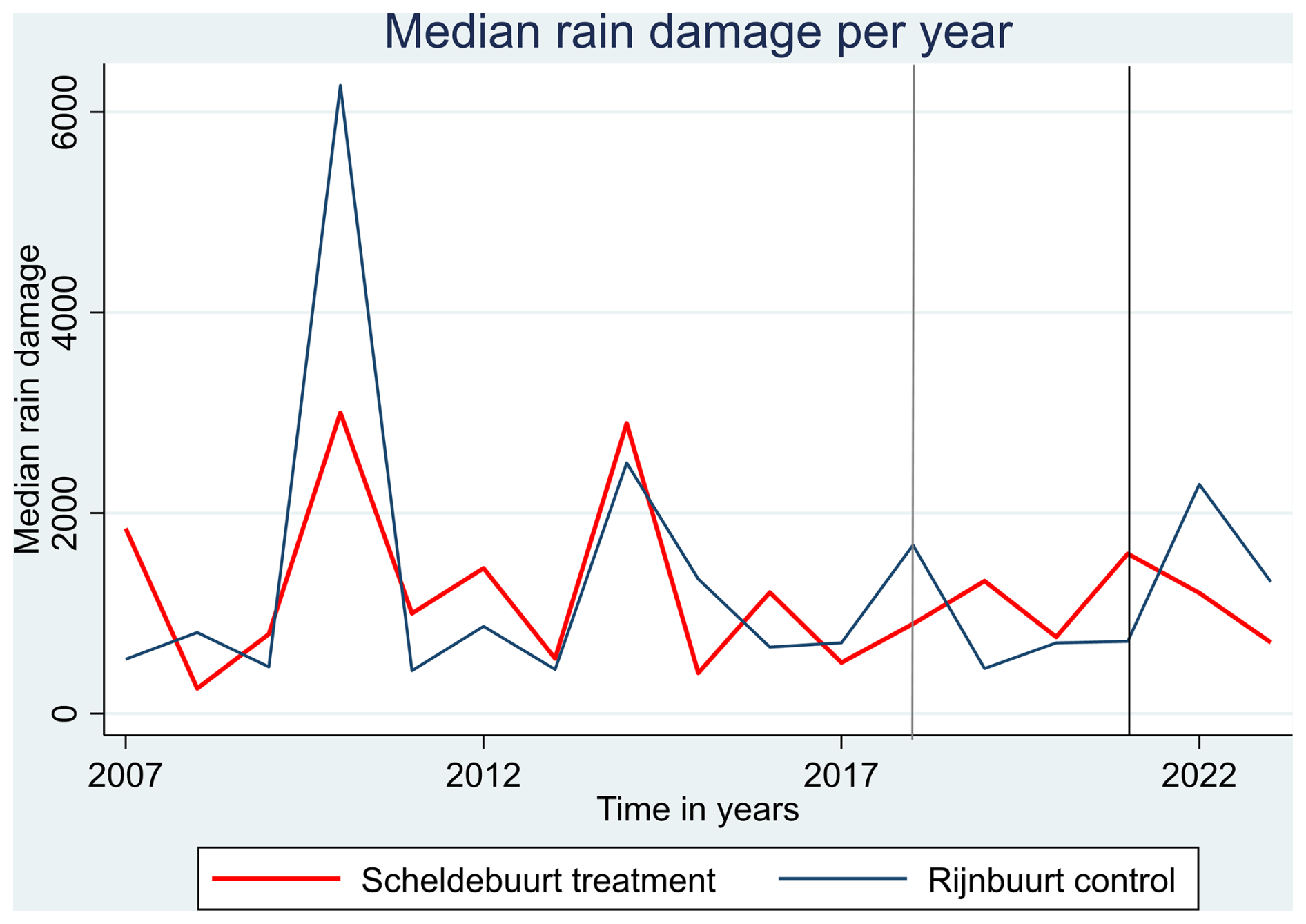

We use the median of observations when rain damage occurred to display the common trend assumption in the figure below, because the average is sensitive to outliers, and we compare only two small neighbourhoods. The intervention period is displayed in the figure as well. The time trends of median damages in both the control group and treatment group are similar before the interventions takes place and start to differ after the start of the intervention period. Therefore, the interventions seem to impact the trend of the median rain damage. After the interventions, the median rain damage rises in the control group, but decreases in the treatment group. Initially, the rain damage of the treatment group is higher than the damage of the control group. Over time, more measures have been implemented. After most of the interventions have finished, the damage of the treatment group decreases and becomes less compared to the control group.

Figure C1Median insured rain damage per year in treatment area and control area. Note: The interventions began in November 2018 and was finished 31 January 2022. To be closest to this, we drew the lines of the start of the intervention in 2018 (in grey). The end of the intervention is drawn in 2021 (in black), since 11 out of 12 months of 2022 have taken place after the intervention period. Also, in the figure above there is no datapoint for 2024, because there are no observations of damages and rainfall exceeding 2 mm h−1 in 2024 (until 15 March).

Table D1Two-way fixed effects DiD regression on insured damage per day in case of maximum rain per hour exceeds 2 mm h−1 with observations in the intervention period.

Standard errors in parentheses. p < 0.01, p < 0.05, ∗ p < 0.1

Table E1Distribution insured rain damage data full dataset (from 2007). Values in euro.

Table E2Detailed description insured rain damage data full dataset (from 2007). Values in euro.

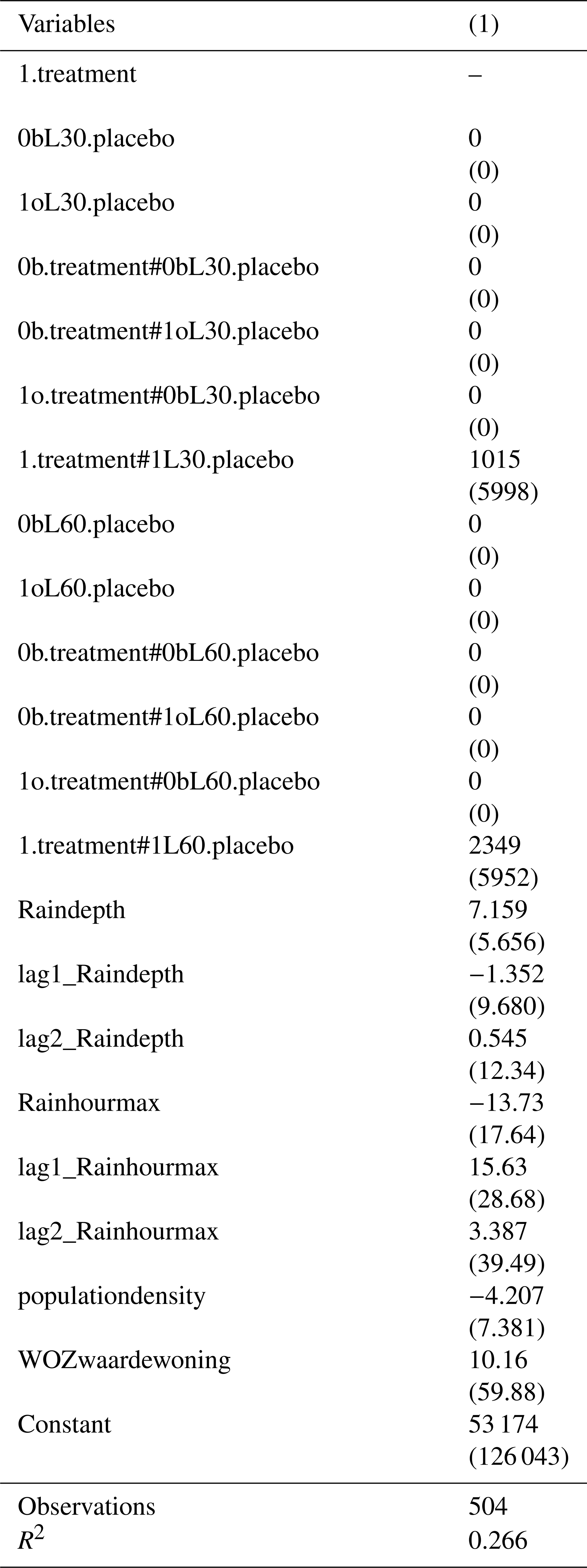

Table F1Two-way fixed effects DiD regression on insured damage per day in case of maximum rain per hour exceeds 2 mm h−1 from 2016 with only significant variables.

Standard errors in parentheses. p < 0.01, p < 0.05, ∗ p < 0.1

The insurance claims data of the Dutch Association of Insurers is not available publicly due to privacy or ethical restrictions.

VO: formal analysis, data curation, writing (original draft preparation and review and editing), and methodology. TE: methodology and writing (specifically on the methodology section). JCJHA: supervision and writing (review and editing). WJWB: conceptualization, supervision and writing (review and editing). PJR: conceptualization, supervision and writing (review and editing).

The contact author has declared that none of the authors has any competing interests.

Publisher's note: Copernicus Publications remains neutral with regard to jurisdictional claims made in the text, published maps, institutional affiliations, or any other geographical representation in this paper. While Copernicus Publications makes every effort to include appropriate place names, the final responsibility lies with the authors. Views expressed in the text are those of the authors and do not necessarily reflect the views of the publisher.

The authors would like to thank the Dutch Association of Insurers for making the data available.

V. Ooms received funding from the Dutch Association of Insurers. W. J. W. Botzen received funding from the project NATURANCE (grant no. 101060464) of the Horizon 2020 Framework Programme of the European Union. J. C. J. H. Aerts received funding from the ERC COASTMOVE project nr884442. P. J. Robinson received funding from EU PIISA (grant no. 101112841).

This paper was edited by Olga Petrucci and reviewed by three anonymous referees.

Amsterdam Weerproof: Rivierenbuurt buurtpagina, https://weerproof.nl/rivierenbuurt/, last access: 7 February 2025a.

Amsterdam Weerproof: https://klimaatadaptatienederland.nl/@295763/amsterdam-rainproof/, last access: 14 March 2025b.

Angrist, J. and Pischke, J.-S.: Mostly Harmless Econometrics: An Empiricist's Companion, Princeton University Press, Princeton, NJ, 392 pp., ISBN 9780691120355, 2009.

Augusto, B., Roebeling, P., Rafael, S., Ferreira, J., Ascenso, A., and Bodilis, C.: Short and medium- to long-term impacts of nature-based solutions on urban heat, Sustainable Cities and Society, 57, 102122, https://doi.org/10.1016/j.scs.2020.102122, 2020.

Busker, T., de Moel, H., Haer, T., Schmeits, M., van den Hurk, B., Myers, K., Cirkel, D. G., and Aerts, J.: Blue-green roofs with forecast-based operation to reduce the impact of weather extremes, Journal of Environmental Management, 301, 1–12, https://doi.org/10.1016/j.jenvman.2021.113750, 2022.

Callaway, B. and Sant'Anna, P. H. C.: Difference-in-Differences with multiple time periods, Journal of Econometrics, 225, 200–230, https://doi.org/10.1016/j.jeconom.2020.12.001, 2021.

Card, D. and Krueger, A. B.: Minimum Wages and Employment: A Case Study of the Fast-Food Industry in New Jersey and Pennsylvania: Reply, American Economic Review, 90, 1397–1420, 2000.

Cheng, C. S., Li, Q., Li, G., and Auld, H.: Climate Change and Heavy Rainfall-Related Water Damage Insurance Claims and Losses in Ontario, Canada, JWARP, 04, 49–62, https://doi.org/10.4236/jwarp.2012.42007, 2012.

Dutch Association of Insurers: Overstroming en droogte: schade en verzekeringen, https://www.verzekeraars.nl/verzekeringsthemas/klimaatbestendig-verzekeren/overstroming-en-droogte, last access: 1 August 2024.

Dutch Association of Insurers: Ledenlijst/Lid worden, https://www.verzekeraars.nl/over-het-verbond/lid-worden, last access: 18 March 2025a.

Dutch Association of Insurers: Dutch Insurance Industry in Figures 2016, https://www.verzekeraars.nl/media/1751/verzekerd-van-cijfers-2016-eng.pdf, last access: 18 March 2025b.

Eggers, A. C., Tuñón, G., and Dafoe, A.: Placebo Tests for Causal Inference, American Journal of Political Science, 68, 1106–1121, https://doi.org/10.1111/ajps.12818, 2024.

Endendijk, T., Botzen, W. J. W., de Moel, H., Aerts, J. C. J. H., Slager, K., and Kok, M.: Flood Vulnerability Models and Household Flood Damage Mitigation Measures: An Econometric Analysis of Survey Data, Water Resources Research, 59, e2022WR034192, https://doi.org/10.1029/2022WR034192, 2023.

Filatova, T.: Market-based instruments for flood risk management: A review of theory, practice and perspectives for climate adaptation policy, Environmental Science & Policy, 37, 227–242, https://doi.org/10.1016/j.envsci.2013.09.005, 2014.

KNMI: Daily, validated and automated in-situ ground-based meteorological observations in the Netherlands (Version 1.0), KNMI Dataplatform [data set], https://doi.org/urn:xkdc:ds:nl.knmi::daily-in-situ-meteorological-observations-validated/1.0 (last access: 29 August 2025), 2025.

Kreibich, H., Bubeck, P., Van Vliet, M., and De Moel, H.: A review of damage-reducing measures to manage fluvial flood risks in a changing climate, Mitigation and Adaptation Strategies for Global Change, 20, 967–989, https://doi.org/10.1007/s11027-014-9629-5, 2015.

Ljubojević, M., Greksa, A., Despotović, J., Rodić, V., Narandžić, T., and Šarac, V.: Chapter 12 – Integrating nature-based solutions for drought resilience in urban and rural planning, in: Handbook of Nature-Based Drought Solutions, edited by: Eslamian, S. and Eslamian, F., Elsevier, https://doi.org/10.1016/B978-0-443-29993-3.00012-6, 253–278, 2025.

Löwe, R., Urich, C., Sto. Domingo, N., Mark, O., Deletic, A., and Arnbjerg-Nielsen, K.: Assessment of urban pluvial flood risk and efficiency of adaptation options through simulations – A new generation of urban planning tools, Journal of Hydrology, 550, 355–367, https://doi.org/10.1016/j.jhydrol.2017.05.009, 2017.

Merz, B., Kreibich, H., and Lall, U.: Multi-variate flood damage assessment: a tree-based data-mining approach, Natural Hazards and Earth System Sciences, 13, 53–64, https://doi.org/10.5194/nhess-13-53-2013, 2013.

Merz, B., Kreibich, H., Schwarze, R., and Thieken, A.: Review article ”Assessment of economic flood damage”, Nat. Hazards Earth Syst. Sci., 10, 1697–1724, https://doi.org/10.5194/nhess-10-1697-2010, 2010.

Met Office: Fact Sheet No. 3 – Water in the Atmosphere, Met Office, Exeter, UK, 9 pp., https://ugc.futurelearn.com/uploads/files/74/7f/747f9bee-dd16-4fc3-8347-fc33b9c4e1a9/fact_sheet_no._3_Water_in_the_atmosphere.pdf (last access: 23 September 2025), 2012.

Meyer, R. and Kunreuther, H. .: The Ostrich Paradox: Why We Underprepare for Disasters, Wharton School Press. https://doi.org/10.2307/j.ctv2hdrfz6, 2017.

Mol, J. M., Botzen, W. J. W., and Blasch, J. E.: Risk reduction in compulsory disaster insurance: Experimental evidence on moral hazard and financial incentives, Journal of Behavioral and Experimental Economics, 84, https://doi.org/10.1016/j.socec.2019.101500, 2020.

Moody's Corporation: Moody's RMS event response estimates insured losses in Germany from the Central Europe floods will likely range between € 2.0 to € 3.0 billion (US$2.1 to US$3.2 billion), https://www.moodys.com/web/en/us/insights/announcements/ moodys-rms-event-response-estimates-insured-losses-in-germany-from-the-central-europe-floods-will-likely-range-between-eu20-to-eu30-billion-us21-to-us32-billion.html, (last access: 14 March 2025), 2024.

Ootegem, L., Verhofstadt, E., Van Herck, K., and Creten, T.: Multivariate pluvial flood damage models, Environmental Impact Assessment Review, 54, https://doi.org/10.1016/j.eiar.2015.05.005, 2015.

Osberghaus, D. and Hinrichs, H.: The Effectiveness of a Large-Scale Flood Risk Awareness Campaign: Evidence from Two Panel Data Sets, Risk Analysis, 41, 944–957, https://doi.org/10.1111/risa.13601, 2021.

Porter, J., Marston, M., Shu, E., Bauer, M., Lai, K., Wilson, B., and Pope, M.: Estimating Pluvial Depth–Damage Functions for Areas within the United States Using Historical Claims Data, Natural Hazards Review, 24, https://doi.org/10.1061/NHREFO.NHENG-1543, 2023.

Poussin, J. K., Wouter Botzen, W. J., and Aerts, J. C. J. H.: Effectiveness of flood damage mitigation measures: Empirical evidence from French flood disasters, Global Environmental Change, 31, 74–84, https://doi.org/10.1016/j.gloenvcha.2014.12.007, 2015.

Rosenzweig, B. R., McPhillips, L., Chang, H., Cheng, C., Welty, C., Matsler, M., Iwaniec, D., and Davidson, C. I.: Pluvial flood risk and opportunities for resilience, WIREs Water, 5, e1302, https://doi.org/10.1002/wat2.1302, 2018.

Rosenzweig, B., Ruddell, B. L., McPhillips, L., Hobbins, R., McPhearson, T., Cheng, Z., Chang, H., and Kim, Y.: Developing knowledge systems for urban resilience to cloudburst rain events, Environmental Science & Policy, 99, 150–159, https://doi.org/10.1016/j.envsci.2019.05.020, 2019.

Seneviratne, S. I., Zhang, X., Adnan, M., Badi, W., Dereczynski, C., Di Luca, A., Ghosh, S., Iskandar, I., Kossin, J., Lewis, S., Otto, F., Pinto, I., Satoh, M., Vicente-Serrano, S. M., Wehner, M., and Zhou, B.: Weather and climate extreme events in a changing climate, in: Climate Change 2021: The Physical Science Basis. Contribution of Working Group I to the Sixth Assessment Report of the Intergovernmental Panel on Climate Change, edited by: Masson-Delmotte, V., Zhai, P., Pirani, A., Connors, S. L., Péan, C., Berger, S., Caud, N., Chen, Y., Goldfarb, L., Gomis, M. I., Huang, M., Leitzell, K., Lonnoy, E., Matthews, J. B. R., Maycock, T. K., Waterfield, T., Yelekçi, O., Yu, R., and Zhou, B., Cambridge University Press, Cambridge, United Kingdom and New York, NY, USA, 1513–1766, https://doi.org/10.1017/9781009157896.013, 2021.

Skrydstrup, J., Löwe, R., Gregersen, I. B., Koetse, M., Aerts, J. C. J. H., de Ruiter, M., and Arnbjerg-Nielsen, K.: Assessing the recreational value of small-scale nature-based solutions when planning urban flood adaptation, Journal of Environmental Management, 320, 115724, https://doi.org/10.1016/j.jenvman.2022.115724, 2022.

Sörensen, J. and Emilsson, T.: Evaluating Flood Risk Reduction by Urban Blue-Green Infrastructure Using Insurance Data, Journal of Water Resources Planning and Management, 145, https://doi.org/10.1061/(ASCE)WR.1943-5452.0001037, 2019.

Sörensen, J. and Mobini, S.: Pluvial, urban flood mechanisms and characteristics – Assessment based on insurance claims, Journal of Hydrology, 555, 51–67, https://doi.org/10.1016/j.jhydrol.2017.09.039, 2017.

Sörensen, J., Persson, A., Sternudd, C., Aspegren, H., Nilsson, J., Nordström, J., Jönsson, K., Mottaghi, M., Becker, P., Pilesjö, P., Larsson, R., Berndtsson, R., and Mobini, S.: Re-Thinking Urban Flood Management—Time for a Regime Shift, Water, 8, 332, https://doi.org/10.3390/w8080332, 2016.

Spekkers, M. H., Kok, M., Clemens, F. H. L. R., and ten Veldhuis, J. A. E.: Decision-tree analysis of factors influencing rainfall-related building structure and content damage, Nat. Hazards Earth Syst. Sci., 14, 2531–2547, https://doi.org/10.5194/nhess-14-2531-2014, 2014.

Statistics Netherlands: Kerncijfers per postcode, https://www.cbs.nl/nl-nl/dossier/nederland-regionaal/geografische-data/gegevens-per-postcode, last access: 14 March 2025.

The City of Copenhagen: Management Plan 2012, https://international.kk.dk/sites/default/files/2021-09/Cloudburst Management plan 2010.pdf, last access: 18 March 2025.

Thieken, A. H., Müller, M., Kreibich, H., and Merz, B.: Flood damage and influencing factors: New insights from the August 2002 flood in Germany, Water Resources Research, 41, https://doi.org/10.1029/2005WR004177, 2005.

Tzoulas, K., Korpela, K., Venn, S., Yli-Pelkonen, V., Kaźmierczak, A., Niemela, J., and James, P.: Promoting ecosystem and human health in urban areas using Green Infrastructure: A literature review, Landscape and Urban Planning, 81, 167–178, https://doi.org/10.1016/j.landurbplan.2007.02.001, 2007.

Wagenaar, D., de Jong, J., and Bouwer, L. M.: Multi-variable flood damage modelling with limited data using supervised learning approaches, Nat. Hazards Earth Syst. Sci., 17, 1683–1696, https://doi.org/10.5194/nhess-17-1683-2017, 2017.

Wooldridge, J. M.: Introduction to Econometrics (Europe, Middle East & Africa Edition), Cengage Learning EMEA, Andover, United Kingdom, 912 pp., ISBN 9781408093757, 2014.

One exception is Löwe et al. (2017), which examined the effect of 9 scenarios of urban development and 32 combinations of FDM measures on flood damages. They find that the effectiveness of the measures depends on climate and urban development. That is, these measures are interlinked, and the effectiveness can change through variations in climate, suggesting that a strategy with different measures through time is preferable to one-off investments.

Due to privacy restrictions on the claims data it is not possible to look at the damages on address level.

The results with the intervention period included are used as a robustness test and can be observed in Appendix D. An analysis with only the significant variables with the intervention period is included in Appendix F.

The damage reduction could be illustrated using an example by the following steps. Firstly, there are 35 rainy days on which severe damage (more than EUR 2500 of insured damage) occurred. Second, when we divide these rainy days by the 17.21 years in the dataset (1 January 2007–15 March 2024), we obtain 2.03 rainy days with more than EUR 2500 of insured damage per year on average. Third, the total damage in the treatment area on 35 rainy days with more that EUR 2500 of damage is EUR 221 771.20. Fourth, if we divide this amount by the 17.21 years in the dataset, we obtain EUR 12 886.18 of damage per year on rainy days with more than EUR 2500 of insured damage, on average. Next, according to model 1 (from 2007), insured damage in the treatment group is on average EUR 1375 per rainy day lower compared to the control group. There are 2.03 rainy days with more than EUR 2500 of insured damage per year. If we multiply the coefficient (EUR 1375) times 2.03 rainy days, we obtain EUR 2791,25 of damage reduction on these days. Lastly, when we divide EUR 2791.25 by the total EUR 12 886.18 of damage per year on rainy days with more than EUR 2500 of insured damage, obtain 0217. Here, we can observe a damage reduction of 21.7 % for rainy days with more than EUR 2500 of insured damage per year on average based on model 1 (from 2007).

In an additional analysis, we omitted the month August 2010, with the large damages in the treatment group and the control group. This month is an outlier and seemed to impact the interaction result and the coefficient. We see some changes in the results: the interaction coefficient is −1432, compared to the −1375 in the model with August 2010 included, and the relation is significant on a higher level (p < 0.01).

- Abstract

- Introduction

- Methodology

- Results

- Discussion and recommendations

- Conclusion

- Appendix A: Description Rivierenbuurt

- Appendix B: Placebo tests

- Appendix C: Median of rain damage per year figure

- Appendix D: DiD regression with intervention period

- Appendix E: Distributions and descriptions of data

- Appendix F: DiD regression with only significant variables

- Data availability

- Author contributions

- Competing interests

- Disclaimer

- Acknowledgements

- Financial support

- Review statement

- References

- Abstract

- Introduction

- Methodology

- Results

- Discussion and recommendations

- Conclusion

- Appendix A: Description Rivierenbuurt

- Appendix B: Placebo tests

- Appendix C: Median of rain damage per year figure

- Appendix D: DiD regression with intervention period

- Appendix E: Distributions and descriptions of data

- Appendix F: DiD regression with only significant variables

- Data availability

- Author contributions

- Competing interests

- Disclaimer

- Acknowledgements

- Financial support

- Review statement

- References